您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

The aluminium industry's supply chain story increasingly begins long before metal reaches a smelter. Across several regions, governments and companies are moving to secure access to bauxite, the industry's most important raw material.

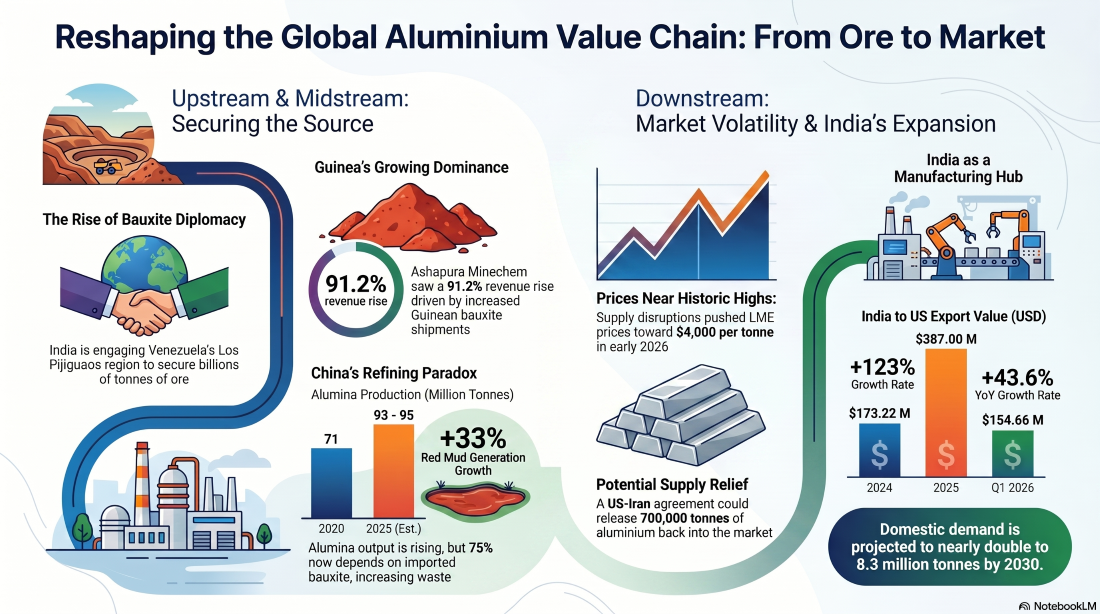

{alcircleadd}India's engagement with Venezuela reflects a broader effort to secure long-term access to raw materials essential for industrial growth. During recent discussions between the two countries, Venezuela's vast bauxite reserves emerged as a key area of interest, particularly the Los Pijiguaos region, which is estimated to hold billions of tonnes of the ore. The development highlights how resource security is becoming increasingly important as countries seek reliable supplies of materials that support aluminium production and manufacturing growth.

At the producer level, Guinea continues to reinforce its position as one of the world's most important bauxite suppliers. Ashapura Minechem's FY2026 performance highlighted the country's growing significance, with higher bauxite and iron ore shipments from Guinea helping drive a 91.2 per cent rise in revenue to INR 52.37 billion and a 44 per cent increase in profit.

Elsewhere, operational momentum is returning after weather and logistics disruptions. Metro Mining's Bauxite Hills operation in Queensland shipped 604,000 wet metric tonnes in May, up 45 per cent from April, following the return of its offshore floating terminal Ikamba from statutory dry-docking. Click here for the full story.

Meanwhile, Cameroon moved closer to joining the ranks of major exporting nations, with Canyon Resources targeting the first shipment from the Minim Martap project by late September 2026 once rail and port connections are completed.

While some regions focus on expanding supply, others are dealing with governance challenges. In the Solomon Islands, political scrutiny intensified around 33 bauxite shipments from West Rennell, bringing renewed attention to regulatory oversight and transparency in the sector. Click here.

As alumina production rises, environmental and geopolitical pressures build

The conversation then shifts downstream to alumina, where growth, sustainability and geopolitics are becoming increasingly intertwined.

China's alumina industry has expanded steadily over the past six years, with production rising from 71 million tonnes in 2020 to nearly 93-95 million tonnes in 2025. Yet this growth has also magnified another challenge: red mud generation. The increase in alumina output has been accompanied by a roughly 33 per cent rise in red mud volumes, drawing greater attention to ore beneficiation, refinery efficiency and waste utilisation. Red the full red mud story here.

Explore- Most comprehensive and forward-looking industry-focused report — Global Bauxite & Alumina Market Forecast to 2036: Supply–Demand, Trade Flows & Price Outlook

The issue is becoming more pronounced as China's dependence on imported bauxite continues to grow. According to the Bauxite Index, only 25 per cent of the country's alumina production in 2025 was derived from domestic bauxite, compared with more than 70 per cent before 2019. The quality of imported ore and the efficiency of refining processes are therefore becoming increasingly important factors in determining both production economics and waste generation.

At the same time, Europe is confronting its own alumina-related challenges. Estonia has renewed calls for a complete ban on alumina exports to Russia, arguing that the material continues to support sectors critical to the country's industrial and military capabilities.

The debate highlights how alumina has become part of broader geopolitical discussions surrounding sanctions and strategic supply chains. Against this backdrop, investment in advanced alumina applications continues. Sasol announced a EUR 60 million investment in its Brunsbüttel facility in Germany to expand production capacity for advanced materials and specialty chemicals, including spherical alumina supports used in catalyst systems.

Greenland Mines also strengthened its critical minerals strategy through an initial 9.9 per cent stake in AnorTech, with the option to increase ownership to 19.9 per cent over the next six months as it works to build a broader critical materials ecosystem. Read here.

Aluminium enters a period of tighter supply and policy intervention

The pressures building upstream are increasingly being felt in the aluminium market itself.

Supply disruptions linked to the Middle East conflict have tightened availability across the value chain. Concerns over smelter operations, shipping routes and regional energy supplies pushed London Metal Exchange aluminium prices to four-year highs and brought the market closer to the USD 4,000 per tonne mark. The rally has been amplified by China's 45 million tonne production cap, which limits the country's ability to rapidly increase output and compensate for any loss of supply from Gulf producers.

The impact of these supply concerns is now visible across regional markets. Japanese buyers have been offered a premium of USD 480 per tonne for July-September deliveries, around 36-37 per cent higher than levels agreed in the previous quarter, reinforcing the tightness seen in physical markets.

Governments are also paying closer attention to supply chain vulnerabilities. In the United States, Congresswoman Haley Stevens introduced the Secure Aluminium Supply Chains Act, which would require the US International Trade Commission to investigate aluminium scrap exports and assess their impact on domestic manufacturing. The proposal reflects growing concerns over the strategic importance of secondary aluminium and scrap availability.

For investors, the changing market environment has renewed interest in major producers. UBS recently highlighted supply risks associated with the Middle East conflict and stronger long-term demand from electrification and industrial sectors, bringing Alcoa's valuation back into focus. Read here.

India emerges at the centre of the next growth phase

While global markets grapple with supply constraints, India is increasingly positioning itself at the centre of aluminium's next phase of growth.

The country remains the world's second-largest primary aluminium producer and the third-largest consumer, supported by integrated producers including NALCO, Hindalco, Vedanta and BALCO. Combined primary smelting capacity stands at approximately 4.3 million tonnes, while annual consumption has reached 4.5-5 million tonnes. Read here.

Yet India's story is no longer solely about production. Despite concerns that US tariff measures would hurt exports, shipments of primary aluminium to the United States have continued to rise. Export value climbed 43.64 per cent year-on-year to USD 154.66 million during the first quarter of 2026, while cumulative exports reached USD 387 million in 2025 compared with USD 173.22 million a year earlier.

At the same time, domestic demand is accelerating rapidly. Consumption is projected to increase from 4.5 million tonnes to 8.3 million tonnes by 2030, prompting producers to commit more than INR 640 billion towards new mines, refineries and smelter expansions. The challenge is that demand may still outpace capacity additions, particularly as imports already approach 3 million tonnes annually and could account for nearly 55 per cent of requirements in FY2025-26.

The industry's future therefore hinges on whether planned investments can arrive quickly enough to support the country's ambitions of becoming both a major manufacturing hub and a leading aluminium consumer.

Participate in our upcoming e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

A changing outlook for the second half of 2026

As the first half of 2026 draws to a close, the aluminium value chain finds itself at a turning point.

Bauxite supply is expanding in some regions while becoming increasingly strategic in others. Alumina producers are balancing growth with environmental and geopolitical pressures. Aluminium markets remain tight due to supply disruptions and production constraints, while governments are taking a more active role in protecting supply chains.

However, one of the biggest variables may be the Strait of Hormuz. Aluminium prices climbed nearly 29.1 per cent in the first half of the year, reaching USD 3,855 per tonne on June 2 as inventories tightened and supply concerns intensified. Now, following a preliminary agreement between the United States and Iran, the prospect of the waterway reopening could allow delayed raw material and metal cargoes to move more freely. Read here the full analysis.

If that happens, as much as 700,000 tonnes of aluminium could gradually return to the market, potentially easing some of the supply pressures that have dominated the industry for much of 2026. Whether that marks the beginning of a more balanced market or merely a pause in a longer period of tightness will shape the industry's next chapter.

Responses