您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

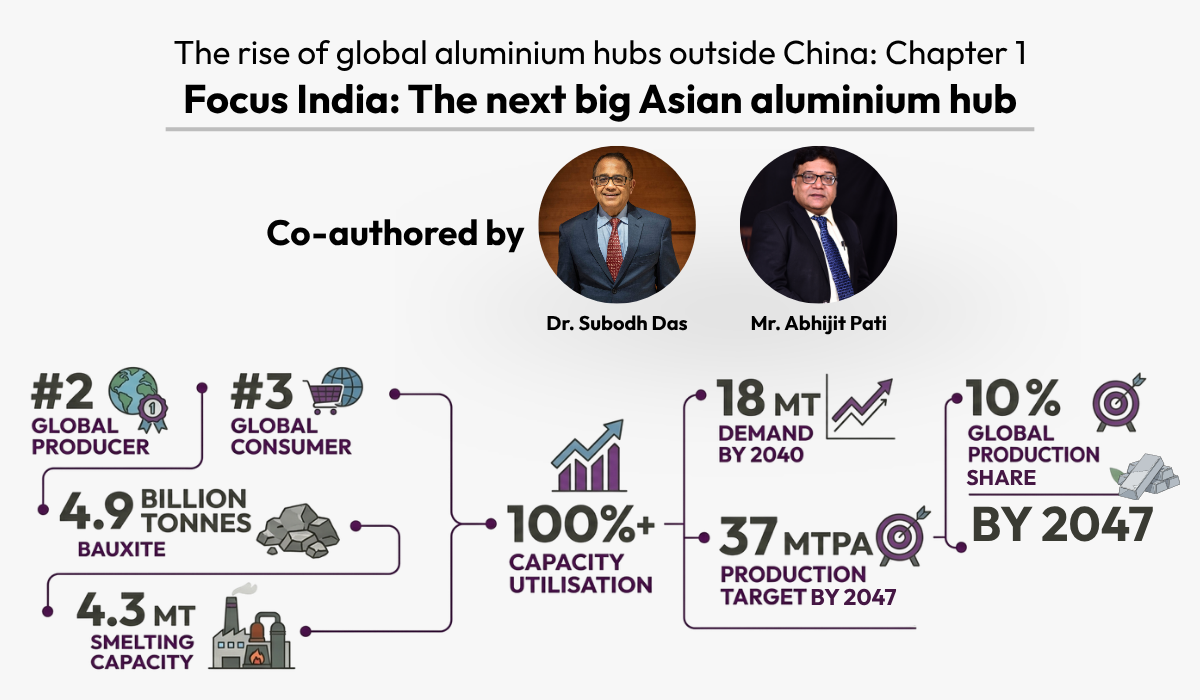

As part of the series, “The Rise of Global Aluminium Hubs Outside China”, the first chapter explores India’s emergence as a key player in the global aluminium landscape. Co-authored by two industry experts, Dr. Subodh Das and Mr. Abhijit Pati, the article provides an in-depth assessment of the country’s current status, pressing challenges, and future growth prospects.

{alcircleadd}India stands as the world’s second-largest producer of primary aluminium, contributing roughly 5.5% to 8% of global output, backed by an industrial framework of fully integrated domestic producers and specialised downstream manufacturers. The primary aluminium ecosystem is anchored by national champions NALCO, Hindalco, Vedanta, and BALCO, which command a combined primary smelting capacity of approximately 4.3 million tonnes (MT).

Driven by rapid urbanisation, infrastructure development, and a clean energy transition, India's annual aluminium consumption has climbed to 4.5-5 MT, making it the third-largest consumer globally. However, the domestic market is highly unequal: per capita consumption rests at just 3.4kg, vastly lagging the global average of 8-12 kg. Consequently, India routes 60% (approx. 2.6 MT) of its current primary aluminium output to international export markets. Backed by expanding capabilities, India is uniquely positioned to transition into a major global supply and downstream consumption hub.

…and so much more!

SIGN UP / LOGINResponses