您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

_0_0.png)

Executive Summary: The global aluminium sector is feeling the heat of a supply crisis, as major aluminium producers face policy curbs, geopolitical crises, sanctions and tariff hurdles, and environmental setbacks. The war in Iran has further inflated the crisis with shipping disruptions and attacks on oil and aluminium facilities in the West Asian region.

{alcircleadd}Top aluminium producers in 2025 (,000 tonnes)

|

Country |

Production 2024 |

Production 2025 |

Capacity 2024 |

Capacity 2025 |

|

China |

44,000 |

45,000 |

44,600 |

45,000 |

|

India |

4,200 |

4,200 |

4,200 |

4,200 |

|

Russia |

3,880 |

3,900 |

4,080 |

4,080 |

|

Canada |

3,200 |

3,300 |

3,270 |

3,270 |

|

UAE |

2,690 |

2,700 |

2,790 |

2,790 |

|

Bahrain |

1,620 |

1,600 |

1,620 |

1,620 |

|

Australia |

1,570 |

1,500 |

1,730 |

1,730 |

|

Norway |

1,300 |

1,300 |

1,460 |

1,460 |

Source: USGS

Global aluminium production in 2025 is estimated at 73.8 million Mt (International Aluminium Institute), with China accounting for 45 Mt. As we can see, all major primary producers are operating at almost 100 per cent capacity, leaving no room for a rise in production in 2026. Global secondary aluminium production in the year was about 42.4 Mt, resulting in a total metal supply of 116 million mt. On the other hand, rising aluminium consumption and shrinking capacity across Europe and the U.S. have created global supply uncertainties.

The great Asian supply crisis

Coming back to 2026, the year began with multiple events signalling a decline in global supply. China has almost exhausted its self-inflicted annual primary aluminium capacity cap of 45 million. Furthermore, with growing anti-dumping investigations across economies against Chinese imports and import tariff blockage, China’s position as a global aluminium supplier is slipping. On the other hand, Russia, one of the largest suppliers of aluminium to the US and Europe, remains out of the league due to the Western sanctions after the war with Ukraine. This was followed by South 32's announcement in March of the closure of the Mozal Aluminium smelter, which has a capacity of 580,000 tonnes per year.

Supply chain disruptions intensified following the outbreak of war with Iran, severely impacting primary aluminium operations and shipments to and from the Gulf. The closure of the Strait of Hormuz disrupted a region that accounts for around 20 per cent of ex-China aluminium production and 8–9 per cent of global supply. Further pressure came from announced production cuts at Qatalum and Alba due to gas shortages, compounding market instability. Reports of Iranian missile and drone attacks on EGA’s Al Taweelah smelter and Alba’s Bahrain operations have reinforced expectations that the global aluminium market will face a tight, structural deficit in 2026.

Exploring alternatives

Europe is reeling under policy hurdles, energy costs, and a strict carbon tax mechanism, which keeps the region out of the league in the supply scenario for primary aluminium. The U.S., one of the largest aluminium markets, has begun efforts to secure its domestic aluminium supply chain amid import tariffs that have soured its trade relationship with its largest aluminium supplier, Canada. Although the country’s primary aluminium capacity has shrunk to its lowest level, it is expanding its secondary aluminium capacity, with a strategic focus on end-of-life aluminium scrap recovery.

This situation has strategically positioned other key Asian aluminium producers, such as India and Indonesia, at the forefront of the global supply chain. This paper provides a critical evaluation of emerging aluminium hubs across regions and how they are leveraging geographical, natural, and logistical advantages to attract large-scale investments to expand aluminium capacity and upgrade production technology.

Emerging aluminium hubs outside China

_0_0.png)

Odisha (India): The raw material hub

Odisha is at the forefront of the Indian aluminium supply chain with abundant raw materials (bauxite), port connectivity, and captive power options. Major investments are being directed towards expanding brownfield capacity and adding greenfield aluminium capacity in the state. Odisha has about 1.5 billion tonnes of metallurgical-grade bauxite reserves, making it the perfect hub for aluminium production. The state accounts for about 54pc of India’s total aluminium smelting capacity, with 2.7 million tonnes (Mt) split among Vedanta, Nalco, and Hindalco. Odisha also houses two alumina refineries operated by Nalco and Vedanta, with a combined capacity of over 5Mt per year. With the brownfield expansion in place for Vedanta Nalco, alumina capacity in Odisha will be over 8Mt by 2030.

Odisha's aluminium capacity is poised for significant growth from its current level. Nalco aims to achieve an installed capacity of about 1 million mt by FY2030, adding 500kt. Additionally, Vedanta plans to develop a 6 MTPA alumina refinery and a 3 MTPA aluminium smelter in Rayagada district, with an investment of $ 11 billion. With these expansion plans in place, Odisha will produce over 6Mt of aluminium annually by 2030.

The state government is also developing the Angul Aluminium Park to encourage ancillary and downstream industries, providing a comprehensive ecosystem for value-added aluminium production.

Russia: The sanction mayhem

Russia produces 3.8 Mt of primary aluminium per year and accounts for 6.2 per cent of global primary aluminium output. Rusal produces the entire output using hydropower, accounting for more than 90 per cent of its electricity generation. This makes Russian aluminium one of the greenest aluminium supplies globally. Rusal also produces Allow green aluminium, which has a carbon intensity of not more than 4 tonnes of CO2 equivalent per tonne of aluminium.

However, sanctions on Rusal aluminium, imposed by the US and UK in April 2024 over its invasion of Ukraine, kept it out of the western markets. Following that, the London Metal Exchange (LME) banned Russian metal produced on or after April 13, 2024. Since then, Russian aluminium has mostly been shipped to Asian countries, with the bulk going to China.

Quebec (Canada): The green aluminium advantage

Quebec is the largest aluminium producer in North America, with a total annual capacity of approximately 3.2 million tonnes of primary aluminium, supplying 90 per cent of Canadian aluminium. With an export value of $7.1 billion, this sector accounts for 10 per cent of the province's exports.

Its largest smelter, Alouette (40 per cent owned by Rio Tinto), can produce 634,000 tonnes per year. Other major facilities include the Bécancour smelter, co-owned by Alcoa and Rio Tinto (462,000 tonnes), and Rio Tinto's ongoing expansions in Alma and Saguenay, totalling about 360,000 mt per year. Quebec's aluminium output benefits from abundant renewable energy, making it one of the "greenest" aluminium productions in the world.

Rio Tinto’s other smelters, including Alma, Arvida-AP60, Grande-Baie, Laterrière, and PLS-Dubuc, account for the rest of the output. Rio Tinto’s Saguenay operations produce Renewal, the industry's first certified low-carbon aluminium, with a footprint of 4 tCO2/tAl or lower. Quebec houses the production centre for ELYSIS’s inert anode aluminium potline in Alma, Québec.

Quebec remains at the forefront of global green aluminium supply, as Russian aluminium remains restricted. The U.S. share of Quebec aluminium exports has continued to decline since the tariff was implemented, while Europe’s share rose to 18 per cent from 0.2 per cent, according to S&P Global Market Intelligence. U.S. aluminium imports from Canada declined significantly in 2025, dipping 26 per cent to 2.33Mt from 3.15Mt in 2024 (International Trade Administration).

UAE (Gulf): The strategic shift from oil to aluminium

Aluminium production in the six Gulf Cooperation Council (GCC) countries reached about 6.45 Mt in 2024, according to data from the Gulf Aluminium Council (GAC). UAE became the world’s fifth biggest aluminium producer, with an annual output of nearly 2.7 Mt coming from Emirates Global Aluminium (EGA). Nearly 60pc of the aluminium produced by the GCC smelters is exported to Japan, South Korea, and other countries.

However, aluminium producers in the Gulf are not planning to expand capacity in 2025-26. The aluminium smelters, including EGA, plan to concentrate on upgrading operational efficiency and technical capabilities to increase output. EGA is focusing on expansion through mergers and acquisitions and on raising its share of renewable energy (solar and nuclear) to capture the western market. EGA’s acquisition of US-based secondary alloy producer Spectro Alloys has been one of the most strategic developments in this regard. EGA Spectro’s expansion adds 55,000 tonnes of secondary billet production capacity in the first phase, raising total production capacity to 165,000 tonnes per year. Additionally, it is constructing a recycling plant in the UAE with a capacity of 170,000mt per year of secondary aluminium billets.

On the primary side, EGA plans to develop an aluminium smelter in Oklahoma, U.S. The plant is expected to have a capacity of 600,000 tonnes of primary aluminium per year, nearly doubling US aluminium production. The smelter construction is expected to begin by the end of 2026, with the first hot metal by the end of 2030.

Indonesia: Ore export ban and smelting expansion

Indonesia is slowly ramping up its aluminium capacity to strengthen its position as a major player in the global supply chain. The country implemented a bauxite export ban starting in June 2023 to boost domestic smelting. Although Indonesia’s market share would remain small, the country is expected to ramp up production substantially from 0.7 Mt in 2025 to about 1.4 Mt by 2027. The plan will be supported by increased bauxite and alumina output of 16 Mt and 7.6 Mt by 2027. The ramp-up will raise Indonesia’s share of global primary production from 1.0 per cent in 2025 to 1.8 per cent by 2027.

Bahrain, Australia, and Norway continue to account for about 4.5Mt of primary aluminium output, with no major expansion plans on the cards. Norway produces around 1.3 Mt of primary aluminium annually, primarily through Norsk Hydro, and supplies mostly in the EU, with production relying heavily on renewable energy and low-carbon aluminium. Bahrain’s Alba, on the other hand, is upgrading its smelting technology and has launched a green aluminium brand, Eternal, using recycled aluminium and carbon offset.

Kentucky (U.S.): Aluminium downstream hub

While the production base for primary aluminium has shifted to Asia, the U.S. has remained the aluminium consumption hub with rising demand from the transport and packaging sectors. Kentucky’s metals economy is one of the most robust in the nation—spanning aluminium, steel, copper, and advanced alloys. It drives $38B in annual economic activity, supports 96,000 jobs, and leads the nation in primary metals job growth.

Kentucky is already home to the U.S.'s existing primary aluminium capacity, which is housed in Century Aluminum’s Hawesville and Sebree facilities. Hawesville was idled in 2022 due to energy security concerns, but has been the focus of restart/retrofit discussions, whereas Sebree is operating at 220,000 mt capacity. Smelters can serve as a foundation for any regional primary cluster. Century plans to build the first new U.S. primary aluminium smelter in 45 years in Kentucky. Upon completion, the smelter would double the current U.S. primary aluminium capacity. The U.S. DOE selected Century for negotiations on up to $500 million to design a low-emissions smelter demonstration in Kentucky. That makes Kentucky a focal point for rebuilding primary supply.

In the downstream space, Kentucky is home to Logan Aluminium, the largest can sheet mill in North America. It produces aluminium sheet for the beverage can and automotive markets, supplying over 45 per cent of the North American can market. It is a joint venture owned by Novelis and Tri-Arrows Aluminium. It is a fully integrated operation with recycling, casting, rolling, and finishing. The state has also drawn large-scale recycling investment, including Novelis’ Guthrie advanced recycling centre. The centre, with an annual casting capacity of 240,000 tonnes of sheet ingot, will be a textbook example of Novelis' closed-loop recycling programs.

Looking at the end-use side, Kentucky has several major automotive Original Equipment Manufacturers (OEMs), including Toyota’s largest plant in Georgetown and General Motors and Ford. This makes the state a perfect hub for domestic supply chain resiliency and closed-loop recycling.

On the flip side, the major roadblock remains the absence of a deposit return scheme in Kentucky. The state has an aluminium can recycling rate of 15 per cent, one of the lowest in the country. The state needs quick policy support and consumer awareness on UBC recycling.

Other developments

As far as the aluminium downstream players are concerned, Novelis and Hydro remained at the forefront with rolling, extrusion, and recycling capacities. Meanwhile, players such as Hindalco, Kobelco, UACJ Corporation, and Sumitomo are churning out aluminium rolled products in Asia. These companies have been working to increase the share of secondary aluminium in their raw materials to manage costs and reduce carbon intensity.

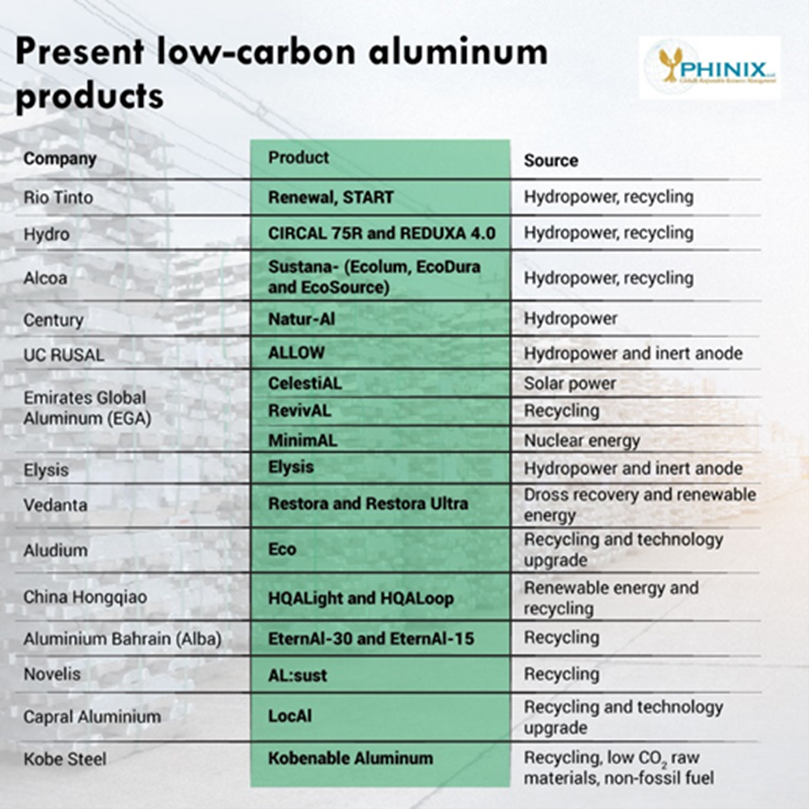

Meanwhile, several aluminium majors have launched low-carbon aluminium brands to meet the changing demands of high-end consumers.

Bottom line

Primary smelting remains power-intensive; projects only pencil out with competitive, reliable, and preferably low-carbon electricity. Policy or utility arrangements that secure long-term competitive power are essential. Additionally, both primary and advanced recycling plants require large CAPEX and time, which remains a bottleneck in finding a short-term solution. Hence, primary capacity expansions are taking place in regions that have access to raw materials and cheaper power.

Supply remains tight globally, and benchmark prices and premiums are likely to remain high due to tariffs, taxes, and energy costs. Quebec has already shifted some of its aluminium exports to Europe, as US tariffs came into effect. Meanwhile, the European Union (EU) Carbon Border Adjustment Mechanism (CBAM) is expected to be in force in 2026. The tax applies to EU imports of aluminium and other metals with higher carbon footprints. With the CBAM in place, Canada’s low-carbon aluminium will be the preferred choice for European buyers. The US, on the other hand, has been raising its secondary aluminium capabilities, but immediate actions are required to secure the metal supply chain.

Meanwhile, if we set aside the present geopolitical situation, Asian producers are at an edge to capture the market. They have recognised that their green credentials must be enhanced to appeal to export markets. Hence, investments are being directed towards renewable power procurement and expansions of recycled aluminium production. With Chinese growth capped, buyers, especially automakers, aerospace, and Western markets, subject to carbon/CBAM pressures, will pay premiums or prefer supply chains that can guarantee lower carbon intensity. Hence, global aluminium majors are re-evaluating their production strategies to capture the rising demand from the new energy economy for the metal of the future and to fill the supply gap caused by geopolitical events and policy directives.

The series opens with coverage of India, offering a closer, deeper look at its growing aluminium ambitions, underlying strengths, and the hurdles it must navigate.

内容提要

受各国产业政策管控、地缘冲突、进出口关税壁垒及环保约束多重因素影响,全球铝行业深陷供应紧缺困境。伊朗战事进一步加剧行业危机,西亚航运受阻、区域油气与铝生产设施接连遇袭,扰动全球铝供应链。

据国际铝业协会(IAI)统计,2025年全球原铝总产量7380万吨,其中中国产出4500万吨。全球主流原铝生产国产能利用率近乎满负荷(100%),2026年全行业几乎没有新增增产空间。同年全球再生铝产量约4240万吨,全品类铝总供应量1.16亿吨。与此同时,欧美地区铝消费稳步抬升、本土冶炼产能持续收缩,全球铝原料供应不确定性进一步放大。

一、亚洲供应链危机全面显现

步入2026年,多重利空因素接连落地,全球铝原料供应呈收缩态势。中国原铝产能已触达4500万吨年度政策上限,增长空间枯竭;叠加多国对华铝产品发起反倾销立案、进口关税壁垒加高,中国在全球铝出口市场的份额逐步回落。俄罗斯作为欧美市场核心铝原料供应商之一,受俄乌冲突后西方国家制裁限制,铝品难以进入欧美主流市场。3月South32公司官宣关闭Mozal铝厂(年产能58万吨),再度收紧全球供应。

伊朗开战加剧全球供应链断裂风险:霍尔木兹海峡通航受限,该区域铝产量约占全球除中国外总产量20%、全球总产量8%~9%;卡塔尔铝业(Qatalum)、巴林铝业(Alba)因天然气供应短缺陆续宣布减产;阿联酋环球铝业(EGA)塔维拉(Al Taweelah)冶炼厂、巴林铝业接连遭遇伊朗导弹与无人机袭击,市场普遍预判:2026年全球铝市将迎来结构性供给短缺。

二、全球寻找替代产能,新兴铝产业集群快速成型

欧洲受制于严苛环保法规、高企能源成本与碳税制度,本土原铝产能扩张停滞;美国作为全球主要铝消费市场,对加拿大加征进口关税导致双边贸易受挫,本土原铝产能跌至历史低位,但该国正大力布局再生铝产业,聚焦报废铝料回收利用。

供需格局变化之下,印度、印尼等亚洲铝生产大国迎来发展窗口期,逐步跻身全球供应链核心位置。本文聚焦全球各地新兴铝产业集聚区,详解各区域如何依托矿产、地缘、物流优势吸纳大额投资,落地产能扩建与生产技改项目。

三、全球五大新兴铝产业核心集聚区

(一)印度奥里萨邦:上游原料核心产区

奥里萨邦坐拥丰富冶金级铝土矿(储量约15亿吨)、港口配套完善、可配套自备电厂,稳居印度铝产业链核心。当地依托存量技改+新建项目持续加码产能,全邦铝土矿储量禀赋优越,是印度天然铝冶炼基地。

全邦电解铝产能270万吨,占印度全国总产能54%,由韦丹塔(Vedanta)、印度国家铝业(NALCO)、印度欣达尔科(Hindalco)三家龙头瓜分;印度国家铝业、韦丹塔合计运营两座氧化铝厂,年总产能超500万吨。伴随两家企业技改落地,2030年当地氧化铝总产能将突破800万吨。

产能扩建规划:印度国家铝业计划至2030财年新增50万吨产能、总产能突破100万吨;韦丹塔拟在Rayagada区投资110亿美元,新建年产600万吨氧化铝厂+300万吨电解铝项目。全部项目落地后,2030年奥里萨邦铝年产量将超600万吨。邦政府同步打造安古尔铝产业园,培育配套及下游深加工产业,完善铝全产业链生态。

(二)俄罗斯:深陷欧美制裁的绿铝产区

俄罗斯年产原铝380万吨,占全球总产量6.2%;俄铝(Rusal)全部产能依托水电生产,电力自给率超90%,产品属于全球低碳绿铝范畴,旗下Allow绿铝产品碳排放控制在4吨二氧化碳当量/吨铝以内。

2024年4月美英出台俄铝产品制裁政策,伦敦金属交易所(LME)禁止交割2024年4月13日后生产的俄罗斯铝锭,俄铝彻底无缘欧美市场,出口货源绝大部分转向亚洲、以中国为主要目的地。

(三)加拿大魁北克:北美低碳铝标杆产区

魁北克是北美第一大原铝产区,年产能约320万吨,贡献加拿大90%铝产量,铝产业出口额71亿美元,占全省出口总值10%。

主力厂区:力拓持股40%的Alouette铝厂(63.4万吨/年);美国铝业+力拓合资贝坎库尔铝厂(46.2万吨/年);力拓在阿尔玛(Alma)、萨格奈地区(Saguenay)在建项目合计新增产能36万吨/年。力拓的其他冶炼厂,如阿尔玛、Arvida-AP60, Grande-Baie, Laterrière, and PLS-Dubuc,等补齐剩余产能,旗下萨格奈(Saguenay)基地量产Renewal低碳铝(碳排放≤4吨CO₂/吨铝),魁北克是ELYSIS惰性阳极铝生产线在阿尔马的生产中心。

由于俄罗斯铝仍受限制,魁北克在全球绿色铝供应方面保持领先地位。根据标普全球市场财智的数据,自关税实施以来,魁北克铝对美出口占比持续下滑、对欧出口占比自0.2%飙升至18%;2025年加拿大对美铝出口同比下滑26%,由315万吨降至233万吨。

(四)海湾阿联酋:从油气大国转型铝工业重镇

据海湾铝业协会(GAC)数据,2024年海湾合作委员会六国原铝总产量645万吨,阿联酋依托阿联酋环球铝业(EGA)年产270万吨原铝,跻身全球第五大铝生产国;海湾地区近60%铝产品销往日韩等亚洲国家。

2025-2026年海湾铝企暂缓新建产能,EGA等企业聚焦技改提效、优化生产效率;同步布局新能源(光伏、核电)降低产品碳排,依托并购扩张全球版图:

(五)印度尼西亚:原矿出口禁令倒逼本土冶炼落地

印尼自2023年6月起全面禁止铝土矿原矿出口,倒逼本土氧化铝、电解铝产业发展。规划数据显示:印尼原铝产量由2025年70万吨提升至2027年140万吨;同期铝土矿年产量1600万吨、氧化铝760万吨;该国全球原铝产能占比由1%提升至1.8%。

(六)巴林、澳大利亚、挪威

巴林、澳、挪三国合计年产原铝450万吨,暂无大型新建产能计划。挪威海德鲁依托水电年产130万吨原铝,产品主要供给欧盟,主打低碳铝;巴林铝业(Alba)升级冶炼工艺,推出依托再生铝+碳抵消的绿铝品牌Eternal。

(七)美国肯塔基州:全球铝深加工枢纽

虽然原铝的生产基地已转移至亚洲,但随着交通和包装行业需求的增长,美国仍然是铝消费中心。肯塔基州有色金属产业年经济产值380亿美元,带动9.6万就业岗位,是美国有色金属用工增速最快地区。

原铝产能:世纪铝业霍斯维尔工厂2022年因能源安全问题停产、正在洽谈复产改造;塞布里工厂当前运行产能22万吨/年。世纪铝业计划在肯塔基落地美国45年来首座新建原铝厂,建成后美国本土原铝产能直接翻倍;美国能源部拟最高提供5亿美元补贴,用于低碳冶炼示范项目建设,肯塔基成为美国重振原铝产能核心落脚点。

深加工板块:北美最大制罐铝板厂Logan Aluminium落地本地(诺贝丽斯+Tri-Arrows合资),产品占据北美45%制罐用铝市场,实现回收-熔铸-轧制全链条一体化;诺贝丽斯古斯里先进再生铝中心投产,年铸锭产能24万吨,是闭环再生标杆项目。

终端优势:肯塔基集聚丰田、通用、福特等头部整车厂,完善的下游需求助力本土铝闭环产业链建设;短板在于当地无铝罐押金回收制度,铝罐回收率仅15%,为全美低位,亟需政策扶持提升废铝回收。

四、全球铝材下游产业近况

诺贝丽斯、海德鲁稳居全球铝板带、铝型材、再生铝龙头;亚洲市场欣达尔科、神户制钢(Kobelco)、UACJ、住友等企业量产各类铝加工材,各大加工企业纷纷提高再生铝投料占比,实现降本减碳。

与此同时,几家铝业巨头已经推出了低碳铝品牌,以满足高端消费者不断变化的需求。

五、全文总结

原铝冶炼属于高耗电行业,项目落地前提是具备稳定、低成本、低碳电力资源;新建冶炼与大型再生铝项目投入资本开支巨大、建设周期漫长,短期难以快速弥补全球供应缺口,因此全球新增产能集中在资源充沛、电价低廉的新兴地区。

受关税、碳税、能源成本影响,全球铝供应整体偏紧,铝锭现货升水、基准价易涨难跌。欧盟碳边境调节机制(CBAM)2026年落地实施,高碳排铝材进口面临额外关税,加拿大低碳铝将成为欧盟进口优选。美国加速扩充再生铝产能,但短期仍难完全保障本土供应链安全。

抛开地缘冲突因素,亚洲铝企凭借资源与成本优势抢占全球市场,各大厂商加速布局绿电采购、扩建再生铝产线,完善低碳产品体系。在中国原铝产能触顶、欧美受碳政策约束的背景下,汽车、航空等终端品牌受碳关税约束,愿意为低碳铝支付溢价;全球铝业巨头重新调整生产布局,填补地缘扰动带来的供应缺口、抢抓新能源行业铝原料增量红利。

本系列专题后续将深度解析印度铝产业发展机遇与现存挑战。

_0_0.png)

Responses