您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

The global aluminium downstream market has been experiencing staggering declines, mapped with price and trade volatility. Recent incidents and market trends are must-watch, to be monitored closely for navigating and decision-making about future trading, hedging and subsequent investments.

{alcircleadd}Products in the spotlight and where to buy them

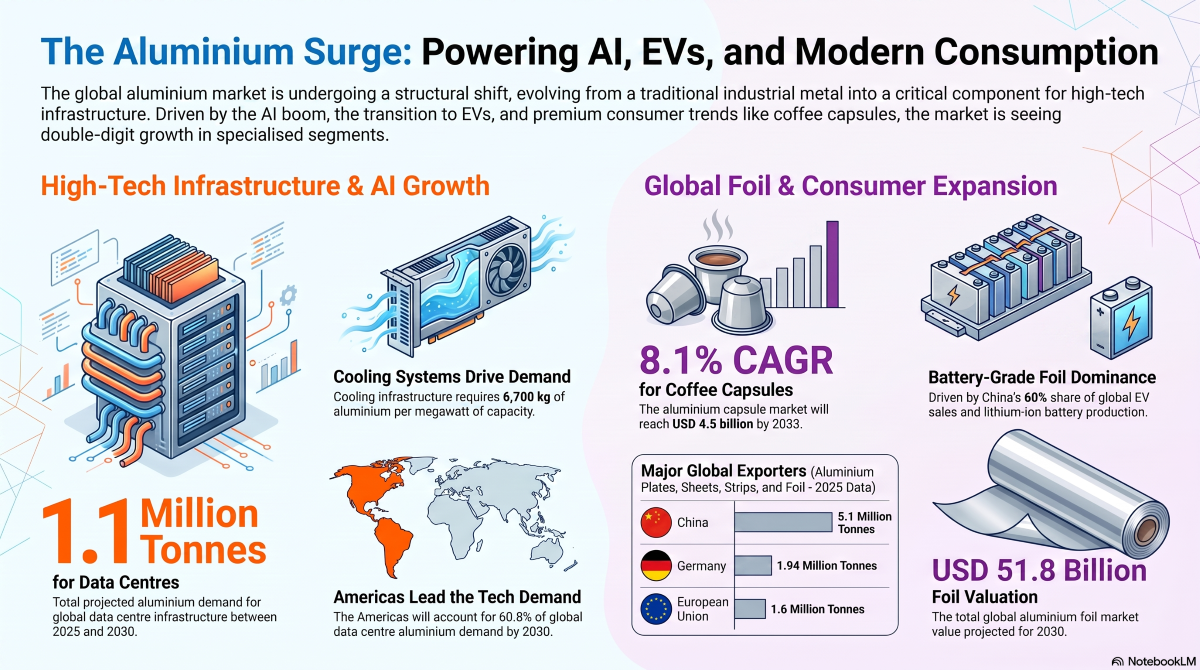

The global aluminium coffee capsule market is expanding rapidly, driven by rising coffee consumption and demand for convenient, premium-quality brewing solutions. Valued at USD 2.48 billion in 2025, the market is projected to reach USD 4.5 billion by 2033, growing at a CAGR of 8.1 per cent. Europe accounts for about 40 per cent of global aluminium coffee capsule consumption, followed by North America with 32 per cent.

The industry's growth is driven by specialised aluminium alloys like 8011 and 3003, which offer strength, formability and corrosion resistance required for capsule designs. The foil used for the capsule body generally has a thickness of 0.07-0.12 mm, or 70-120 μm.

Gather an in-depth understanding of the extrusion segment of the global aluminium industry with The World of Aluminium Extrusions – Industry Forecast to 2032

With global consumption reaching nearly 25 billion capsules annually, the market's future will depend not only on rising demand but also on improving circularity.

China leads the global aluminium foil market as the world's largest producer, consumer and exporter. In 2024, China produced about 4.7 million tonnes of foil, consuming 3.32 million tonnes (over 50 per cent of global demand). Its exports rose 18.3 per cent year-on-year to 1.55 million tonnes, the value reaching USD 5.7 billion. The top buyers were India, Thailand, Indonesia, Mexico and South Korea.

Battery-grade aluminium foil has emerged as the strongest growth segment, fuelled by China's dominant EV and lithium-ion battery industries. Demand remains steady, with China’s contribution above 60 per cent of global EV sales.

According to AL Circle's report, Aluminium Foil and its End Uses: Current Trends and Forecast till 2030, China's continued leadership reflects its ability to align industrial policy with emerging industries.

Special note: Understanding these for aluminium producers and downstream manufacturers will be critical for future investment, capacity expansion and market positioning.

The rapid expansion of artificial intelligence (AI), cloud computing and digital infrastructure is creating a new demand engine for aluminium. According to industry estimates, data centre infrastructure growth could take aluminium demand to around 1.1 million tonnes between 2025 and 2030, growing at a CAGR of 8-10 per cent.

Cooling systems account for the largest share of aluminium consumption at roughly 6,700 kg per MW of capacity. Servers and semiconductor hardware use around 2,700 kg per MW, with electrical and backup power systems at approximately 1,200 kg per MW. Networking and storage infrastructure require a of about 260 kg per MW.

Regionally, the Americas are projected to account for 60.8 per cent of global aluminium demand from data centres by 2030, followed by Asia-Pacific (25.8 per cent) and Europe, the Middle East and Africa (13.4 per cent).

Kenanga Research expects aluminium supplier AMS Bhd to benefit from the ongoing global semiconductor equipment upcycle, driven by rising investment in artificial intelligence (AI) infrastructure and wafer fabrication equipment (WFE). Kenanga projects AMS' revenue to grow 17 per cent in FY2026 and 20 per cent in FY2027, while net profit is forecast to increase 49 per cent and 60 per cent, respectively.

Growth is expected to be supported by stronger semiconductor demand, value-added processing services and expanding WFE spending, particularly outside China, alongside accelerating AI-related capital expenditure by major hyperscale technology companies.

Semiconductor-related revenue, which has doubled since 2024, is expected to contribute 55 per cent of total revenue by FY2027, up from 37 per cent in FY2025.

Key takeaway: As per the 2025 data, investors should watch closely the market trends of countries performing well in the categories of a) aluminium plates, sheets and strips; b) aluminium bars, rods and profiles; c) aluminium foil

Why? – Since data centres have been gathering momentum, coupled with EV and solar module demand. These are ultimately leading the nations closer to the targeted Net Zero goal for a green future where aluminium semis have a key role to play.

Looking to source or sell aluminium extrusions? Discover relevant business opportunities on our B2B marketplace.

Tariffs, trade and policy changes in aluminium market dynamics

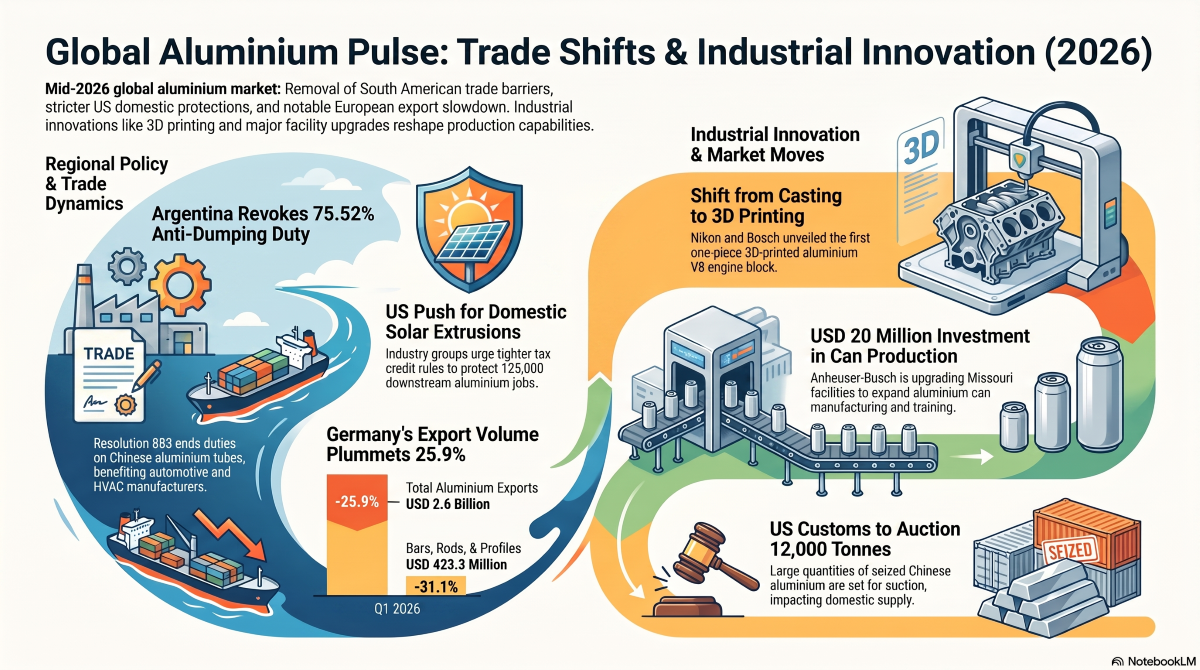

Argentina's Ministry of Economy has withdrawn the anti-dumping (AD) duties imposed on aluminium tube imports from China after completing a sunset review and a review of changed circumstances.

The ruling covers unalloyed aluminium tubes like those made from 3xxx and 6xxx series aluminium alloys, IRAM Standard 681 compliant, featuring an external diameter of 130 mm or less, including coil-form products.

The anti-dumping investigation was first initiated in May 2019, introducing a 75.52 per cent anti-dumping duty in November 2020. Having reviewed the dumping practices between July 2024 and June 2025, the duties have been revoked with immediate effect under Resolution No. 883.

Special note: While the move would ease manufacturing costs for Argentine industries like automotive and HVAC, on the flip side, competitive pressure on domestic metal producers would intensify.

The Coalition for a Prosperous America (CPA) and the Aluminum Extruders Council (AEC) have urged the US Treasury Department and Internal Revenue Service (IRS) to tighten domestic content rules under Sections 45Y and 48E, as aluminium extrusions for solar module frames should be manufactured in the US to qualify for federal tax credits.

Aluminium extrusion accounts for 61 per cent of production costs and 52 per cent of capital investment. Thus, incentives for imported extrusions discourage investment in domestic manufacturing, despite the US downstream aluminium industry supporting over 125,000 jobs.

CPA President Jon Toomey stated, “Extrusion is where the capital, the jobs, and the value are,” adding that incentives should not be available for products undergoing minimal processing after being imported.

Germany's aluminium exports recorded a sharp slowdown in Q1 2026, with total shipments falling 25.9 per cent Y-o-Y to 469,178 tonnes, valued at USD 2.6 billion. Among product categories, aluminium bars, rods and profiles witnessed an even steeper decline, dropping 31.1 per cent to 52,072 tonnes, worth USD 423.3 million.

The category accounted for 11.1 per cent of Germany's total aluminium exports during the quarter, extending the downward trend seen in 2025.

Despite overall aluminium exports posting modest annual growth in 2025, exports of bars, rods and profiles continued to weaken. In Q1 2026, Switzerland remained the largest importer of these products from Germany, followed by France, Austria, the Netherlands and the Czech Republic. However, Germany still holds one of the top positions among the world’s largest exporters in the segment.

Key takeaway: While these countries undergo shifts in trade dynamics, market participants should closely monitor the following project and investment announcements in the said nations:

Why? – As these nations navigate market shifts, investors can benefit from the progress and updates on these incidents as to how they have been impacting the global aluminium downstream supply chain.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

Responses