您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

Image used for representational purpose only

Aluminium casting is the process of melting aluminium and pouring it into a mould, taking a fixed shape when it cools. That shape can be an engine block, a wheel, a gearbox housing, a window frame or a battery tray for an electric car.

{alcircleadd}People pick aluminium over steel or iron for one simple reason: It is lightweight but still strong. A cast aluminium part can be up to half the weight of the same part in steel. Less weight means a car burns less fuel, an EV drives further on one charge and a plane carries more.

There are three main ways to cast aluminium and the difference between them decides cost, speed and quality:

|

Casting method |

How it works |

Best for |

Typical use |

|---|---|---|---|

|

Die casting |

Molten aluminium is forced into a steel mould under high pressure |

High volumes, thin walls, complex shapes |

Car parts, electronics housings |

|

Sand casting |

Metal is poured into a mould made of packed sand |

Small batches, large parts, low cost |

Prototypes, heavy machinery parts |

|

Permanent mould (gravity) casting |

Metal flows into a reusable metal mould by gravity |

Strong parts, medium volumes |

Wheels, pistons, pump bodies |

Inside die casting, there are more sub-methods you will see named in tenders and reports: High-pressure die casting (HPDC), low-pressure die casting (LPDC), gravity die casting, squeeze casting and vacuum die casting. HPDC is the workhorse of the auto industry because it is fast and repeatable.

Also read: Thrust Capital Partners acquires aluminium and titanium casting company Alphacasting

The market at a glance

The global aluminium casting market is worth about USD 106.7 billion in 2025. It is expected to touch roughly USD 110.5 billion in 2026 and grow to somewhere between USD 150 billion and USD 171 billion by 2032–2033. The yearly growth rate sits between 4.7 per cent and 6.2 per cent, depending on how each research house draws the boundary of the market.

Three numbers tell you almost the whole story:

If you remember nothing else, remember this: Aluminium casting is growing because the world wants lighter vehicles and it is slowing down only when metal prices spike. Everything below is a longer version of that one sentence.

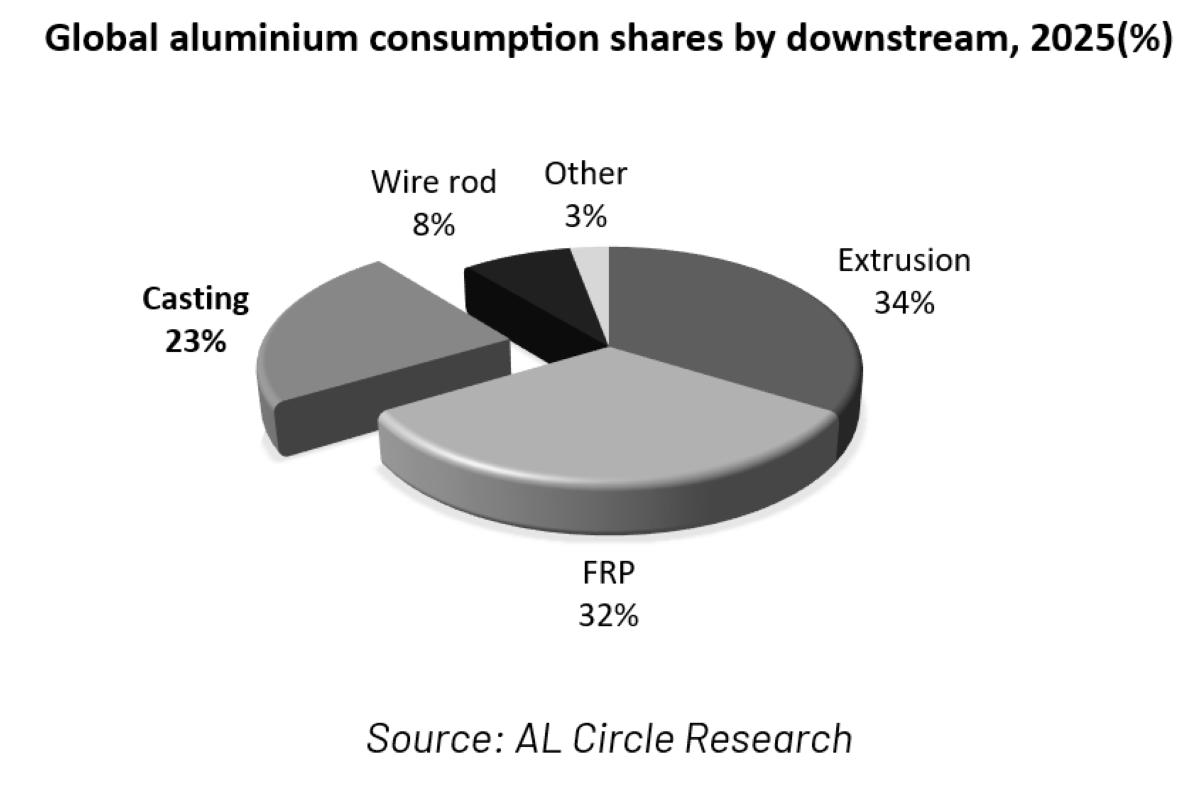

Global aluminium consumption shares by downstream, 2025(%)

Globally in 2025, aluminium casting accounted for 23 per cent of the total downstream aluminium consumption, representing a substantial share of the aluminium value chain. As electrification, lightweighting, urbanisation and manufacturing localisation reshape demand, the market is said to be entering a period where understanding where growth will emerge and how demand patterns will shift through 2032 will be critical for informed business decisions.

What is driving growth in aluminium casting?

Growth comes down to one big force and several supporting ones, including:

Car makers are replacing steel and iron with aluminium casting in engine blocks, transmission housings, wheels, battery enclosures and structural parts. Today, light vehicles typically make use of 30–40 per cent aluminium by relevant part count and that share is expected to climb toward 70 per cent over the coming years as emission rules get stricter.

An EV needs a big, strong, light case to hold its battery. That single part alone has created fresh demand for large aluminium castings.

Instead of welding 70 small parts together, car makers now cast one giant piece. This cuts cost, cuts weight and speeds up the line. It is one of the fastest-moving trends in the whole industry.

Planes and defence equipment want light, strong parts too and this sector pays a premium for quality.

Window frames, panels, pump bodies and industrial parts give the market a floor of demand that does not swing much.

Also read: 3D printing to replace casting? Nikon SLM, Bosch unveil one-piece aluminium V8 engine block

How is the aluminium casting market evolving?

The current aluminium casting market is evolving because of two forces: Price and energy.

Aluminium foundries run on thin margins, so they feel every swing in metal prices. When the aluminium price rises, the price of casting also rises with it, and buyers delay orders. This is not a small risk. By January 2026, aluminium for US buyers had risen by nearly 40 per cent, crossing USD 5,200 per tonne, driven by higher import tariffs and tighter global supply.

Energy is the other pressure. Melting aluminium takes a lot of power, so foundries in high-electricity-cost regions struggle to compete.

A third, quieter force is material competition. Magnesium alloys are light and strong too and in some parts they can replace aluminium. For now, aluminium stays ahead on cost and supply, but it is worth watching.

Aluminium casting prices and cost pressures in 2026

Price is the single biggest thing to watch in 2026. As noted earlier, US aluminium had climbed nearly 40 per cent to over USD 5,200 per tonne by January 2026, pushed up by tariffs and tight supply.

For an aluminium caster, this matters more than for almost anyone else in the chain, because metal is the largest input cost. When the price rises fast, three things happen: Margins shrink, long-term contracts get harder to sign, and buyers push back on orders.

This is exactly why serious casting buyers now want pricing intelligence, not just a market forecast. Knowing where aluminium casting prices, along with which industry and in which region, are heading is worth more than knowing where they have been.

Aluminium casting market by segment at a glance

By the casting process:

By the end-use industry:

By the region:

Which regions lead the aluminium casting market?

The reason is simple: The biggest aluminium-producing countries and the biggest car factories are in this region. China, India, Indonesia and others turned into manufacturing powerhouses over the last two decades, and casting demand followed.

India stands out as one of the fastest-rising markets, backed by growing auto production, new foundries and strong government focus on manufacturing.

These regions hold the next two spots. Their strength is high-value casting for autos and aerospace, home to names like Airbus, Boeing and the major German and US car brands.

These regions are deemed to be smaller given today’s market. Africa mostly exports raw aluminium rather than casting it locally, which leaves room for future growth.

Who are the major aluminium casting companies?

The market is a mix of large integrated aluminium producers and specialist foundries and these are the names you will see throughout:

The pattern is clear: Whoever serves the car industry well tends to lead, because transportation is where most of the aluminium casting goes.

Recycled aluminium and sustainability niche in casting

Recycled or secondary aluminium is becoming central to casting and not just a side story. Melting aluminium scrap uses a fraction of the energy needed to make new metal from ore, which cuts both cost and carbon.

Two forces are pushing this: Tighter emission rules, especially in Europe and the EU Carbon Border Adjustment Mechanism (CBAM), which puts a carbon cost on imported aluminium.

For foundries, using more recycled metal is now both a green move and a smart financial one. Any casting strategy built for 2032 has to plan for a higher share of recycled feedstock.

What is the outlook for aluminium casting to 2032?

This growth trajectory is being underpinned by long-term shifts across manufacturing, transportation, energy systems and infrastructure, creating new demand dynamics and strategic opportunities for businesses across the aluminium casting value chain.

By 2032, the market is expected to sit somewhere around USD 150–170 billion. The pull comes from EVs, mega-casting and stricter emission rules that keep pushing metal into vehicles. The drag comes from metal-price swings and energy costs.

The winners over the next few years will be the casters who can do three things at once: Hold quality high, keep costs low even when metal prices jump and use more recycled aluminium. Buyers who understand plant economics and pricing, not just the headlines of the current market, will make better calls.

Go deeper with the AL Circle’s upcoming report

Our upcoming report, “Global Aluminium Casting Market 2026–2032”, provides the market intelligence that today’s businesses need but is not available elsewhere, such as plant economics, alloy segmentation, pricing intelligence and supply-chain analysis and strategic recommendations, which are built for people who buy, sell or invest in casting.

Make smarter business decisions with insights on:

… and much more!

Want to see it first? Request a free sample of the report and one of our research specialists will walk you through it. Still confused? Take a 45-minute consultation with our research team.

Also read: Final Call: Pre-book the Market Intelligence Every Aluminium Casting Business Needs

Some frequently asked questions that the report addresses

Q. What will the aluminium casting market be worth by 2032?

A. Most forecasts point to USD 150–170 billion by the early 2030s, at a growth rate between 4.7 per cent and 6.2 per cent a year.

Q. What is the biggest casting process?

A. Die casting accounts for about 76 per cent of the market.

Q. Which industry uses the most aluminium castings?

A. Transportation accounts for about 57.7 per cent, mainly because of cars, EVs and commercial vehicles.

Q. Which region leads the market?

A. Asia Pacific holds about a 52.1 per cent share, and China holds the position of the largest country.

Q. What is the difference between die casting and sand casting?

A. Die casting forces metal into a steel mould under high pressure and suits high-volume, complex parts. Sand casting pours metal into a sand mould and suits small batches and large, low-cost parts.

Q. What is mega-casting or gigacasting?

It is casting one very large part instead of welding many small ones together. It cuts weight, cost and assembly time, and it is one of the fastest-growing trends in the auto industry.

Q. Why are aluminium prices important for casters?

A. Metal is a caster's highest cost, and when aluminium prices rise sharply, as they did in early 2026, crossing USD 5,200 per tonne for US buyers, margins shrink and orders slow.

Q. Who are the leading aluminium casting companies?

A. Nemak, Ryobi, Rheinmetall Automotive, Alcoa, Rio Tinto, Ahresty, Dynacast and others, most of them tied closely to the auto industry.

Q. Is recycled aluminium used in casting?

A. Yes, and its share is rising fast. Recycled metal uses far less energy, cuts carbon and helps manage costs under schemes like the EU’s CBAM.

Responses