您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

The global aluminium industry saw activity across trade enforcement, downstream expansion, automotive technology, corporate restructuring and end-user markets, with developments stretching from the United States and Europe to China, Ghana, India and Southeast Asia. While a major US customs case involving Chinese aluminium moved towards its final chapter, fresh investments and supply agreements pointed to continued expansion in value-added products.

{alcircleadd}At the same time, cost pressure and new casting technologies were reshaping the automotive supply chain, while aluminium gained ground in applications ranging from electric vehicles and wiring to beverage cans, bicycles, smartphones and premium construction systems.

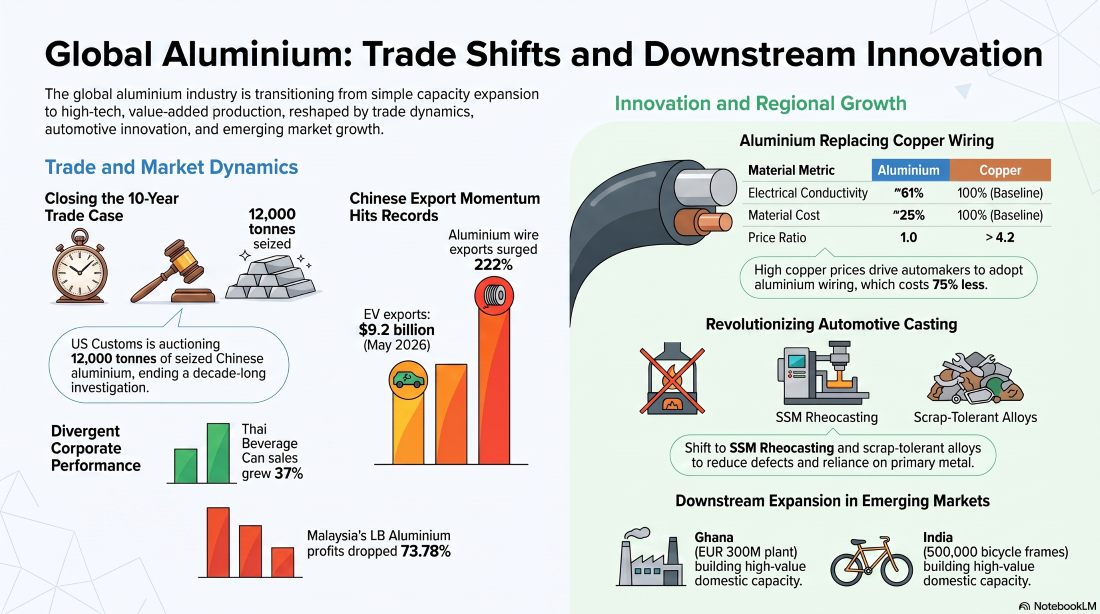

Trade flows shift as the US closes a decade-long case and China’s exports accelerate

One of the most significant trade developments came from the United States, where US Customs and Border Protection (CBP) is preparing to hold the second and final public auction of approximately 12,000 tonnes of seized extruded aluminium profiles imported from China. Scheduled for July 23, 2026, in Riverside, California, the sale will bring a nearly 10-year investigation into Chinese aluminium imports to a close.

According to CBP, more than 160,000 aluminium “pallets” stored across 623 shipping containers will be included in the auction, with the containers themselves also forming part of the sale. The material is currently held at an Amentum Holdings LLC facility in Riverside.

While the US prepares to dispose of seized Chinese aluminium, China’s own export picture is showing strong momentum in selected downstream products. Aluminium wire exports reached 50,224 tonnes in May, jumping 222.67 per cent from April as exporters capitalised on rising aluminium prices and favourable trade incentives. The May volume alone surpassed the combined 42,955 tonnes shipped during the first four months of the year.

The country also set a new record in electric vehicle exports. China exported about 448,000 electric passenger vehicles in May 2026 , comprising around 279,000 battery electric vehicles (BEVs) and 169,000 plug-in hybrid electric vehicles (PHEVs). The value of EV exports reached a record USD 9.2 billion, up 49 per cent year-on-year and above the previous monthly high of USD 9.1 billion recorded in April 2026. According to energy think tank Ember, growing demand from the Association of Southeast Asian Nations (ASEAN) continued to support the expansion.

Automotive aluminium enters a new phase of technology and supply-chain change

The automotive sector remained a major centre of change, but the pressure is increasingly shifting from simple capacity expansion to cost control, material efficiency and manufacturing quality. European foundries are facing critical insolvencies as heavy capital expenditure on massive giga-presses compresses profit margins to around 5 per cent, driving aggressive consolidation among Tier 1 suppliers.

Against this backdrop, new alloy and casting technologies are challenging established production models. Oak Ridge National Laboratory’s “RidgeAlloy” enables structural automotive castings to absorb high iron levels from post-consumer scrap, reducing the electric vehicle industry’s reliance on primary aluminium dilution. At the same time, the industry is moving towards Semi-Solid Metal (SSM) rheocasting to address the severe defect rates associated with standard High-Pressure Die Casting (HPDC) and achieve the near-zero porosity required for modern drivetrains. Read the full story here.

Changes are also unfolding within established automotive supply chains. CITIC Dicastal has revised its aluminium alloy wheel supply agreement with affiliated companies, increasing annual purchase caps through 2028 following changes to its supplier network and expectations of stronger market demand. According to a filing with the Hong Kong Stock Exchange, the new framework replaces an earlier arrangement after several wheel manufacturers became, or are expected to become, connected parties following acquisitions by parent company CITIC Group.

The global aluminium casting usage is expected to reach 24.2 million tonnes in 2026. To know about the future market trends, prebook our upcoming report “Global Aluminium Casting Market 2026-2032

Constellium, meanwhile, has sold its ownership stake in its automotive structures joint venture in Changchun, China, along with its partner, to a Chinese automotive holding company. The company said the transaction forms part of its Vision 2028 strategy to optimise its manufacturing footprint and improve competitiveness.

Beyond castings and structural components, rising copper prices are opening another avenue for aluminium in vehicles. Automakers and manufacturers are increasing the use of aluminium wiring as a lighter and lower-cost alternative, with companies such as Ferrari and BMW expanding adoption across new models. The shift comes as the copper-to-aluminium price ratio has moved above 4.2. Aluminium provides around 61 per cent of copper’s electrical conductivity but costs roughly one-quarter as much, allowing manufacturers to lower material costs by using thicker aluminium cables where design requirements permit.

Ghana and India push downstream aluminium expansion

Investment in value-added aluminium capacity also gathered pace across emerging markets. Ghana took a step towards strengthening its domestic aluminium value chain through a Memorandum of Understanding between the Ghana Integrated Aluminium Development Corporation (GIADEC) and Italian engineering company Danieli & C. Officine Meccaniche S.p.A.

Under the agreement, Danieli is set to invest around EUR 300 million (USD 341.61 million) in an aluminium sheet and foil rolling facility at the proposed Tema Integrated Industrial Park. The plant is expected to produce 40,000 to 45,000 tonnes of value-added aluminium products annually across ten categories, serving industries including packaging, pharmaceuticals, food processing, catering and other industrial uses.

India also saw fresh downstream expansion, with Hindalco Industries launching an aluminium bicycle component manufacturing facility in Chakan, Pune, Maharashtra, strengthening its position in the country’s mobility sector. Designed to serve both Indian and overseas markets, the plant will manufacture aluminium frames, rigid forks, wheel rims, handlebars and other bicycle components, reflecting the company’s growing focus on lightweight and sustainable mobility solutions.

The facility uses advanced manufacturing and finishing technologies and is expected to produce approximately 500,000 bicycle frames and forks annually, along with 750,000 handlebars and 800,000 pairs of wheel rims.

The country’s premium construction market is also drawing new aluminium product launches. Window Magic introduced WM AURA, an ultra-luxury aluminium fenestration range, alongside Window Magic Atelier, a dedicated luxury fenestration experience centre in South Delhi. The company described the Atelier as an immersive destination for architects, developers, interior designers and homeowners, with dedicated experiential zones showcasing luxury doors, windows and façade systems.

Corporate performance and manufacturing investment send mixed signals

Not all developments pointed in the same direction. In Malaysia, LB Aluminium Bhd reported a sharp decline in fourth-quarter earnings as weaker contributions from its aluminium segment weighed on performance. Net profit fell 73.78 per cent year-on-year to MYR 1.88 million (USD 459,736) for the quarter ended April 30, 2026 (4QFY2026), compared with MYR 7.18 million (USD 1.7 million) in the corresponding period last year. Read here.

In the United States, however, manufacturing investment continued. Anheuser-Busch announced more than USD 20 million in investment across its facilities in St. Louis and Arnold, Missouri, aimed at expanding production capacity and strengthening manufacturing operations. The programme includes upgrades to brewery and aluminium can manufacturing equipment to support growing demand for brands such as Michelob ULTRA and Busch Light.

The contrasting developments underline the varied conditions across aluminium-consuming industries: some businesses are dealing with weaker segment contributions and margin pressure, while others are committing fresh capital to capacity, manufacturing efficiency and downstream growth.

To learn about the autonomous furnace tending in aluminium cast houses from RIA Cast House Engineering, join the webinar Autonomous furnace tending in aluminium cast houses: Improving safety, productivity and yield

End-user demand broadens across cans, beverages and consumer technology

Further downstream, aluminium can manufacturers are introducing new designs and technologies centred on circularity, lightweighting, production efficiency and consumer convenience. Companies including Canovation, Henkel Adhesive Technologies and Sonoco say the sector is focusing on resealable packaging, water-based sealants and digital manufacturing tools alongside broader circularity and lightweighting goals. Read here.

Thailand offers one example of how changing consumer preferences are supporting this market. Thai Beverage Can Ltd (TBC) expects domestic demand for aluminium beverage cans to continue growing as consumers increasingly choose functional drinks, energy drinks and premium beverages. The company recorded a 37 per cent year-on-year increase in sales volume during the first quarter of 2026, indicating stronger demand despite continued uncertainty in global markets. Read here.

Aluminium’s reach is also expanding in consumer electronics. Xiaomi unveiled the new Sky Blue colour option for the REDMI K90 Ultra one day before the smartphone’s official launch in China. The device features an aluminium alloy CNC frame, while the latest teaser shows a low-saturation blue finish with a flowing metallic texture and a flat metal camera module. As part of the REDMI K Ultra series, the model is expected to serve as the basis for the Xiaomi 17T Pro in global markets.

Taken together, these developments show an aluminium market being shaped by several forces at once. Trade enforcement is closing long-running cases even as Chinese downstream exports accelerate; automotive producers are looking to scrap-tolerant alloys, rheocasting and aluminium wiring to manage costs and technical demands; Ghana and India are building new value-added capacity; and end-user markets are widening aluminium’s role across mobility, packaging, beverages, electronics and premium construction.

Responses