您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

EXECUTIVE SUMMARY:

{alcircleadd}In the first instalment of this AL Circle exclusive series, we mapped the physical footprint of the giga-casting revolution. In the second instalment, we dissected the metallurgical science required to make a 1.5-metre structural casting viable. We established that the machines are functional and the alloys exist. Consequently, the global automotive supply chain is no longer asking whether giga-casting works. It is actively deciding who will survive its implementation.

The deepest and most consequential transformations are no longer confined to the press hall. The true disruption has shifted to the macroeconomic survival strategies of the Tier 1 foundry ecosystem. Furthermore, it is triggering a massive upstream threat. If your procurement strategy or your primary smelting output relies on a world of traditional 2,000-tonne presses and standard ADC12 alloys, you are walking blindly into a terminal margin trap.

To survive this industry-wide reconfiguration, we must first examine the brutal macroeconomic fallout currently destabilising the traditional foundry ecosystem.

The deployment of giga-casting is occurring against a highly volatile global macroeconomic backdrop. The financial stakes are staggering. The global giga-casting presses market is compounding at a robust annual growth rate of roughly 12.6 per cent. This forces legacy foundries into an aggressive, multi-million-dollar capital equipment race that many cannot afford.

This geographic redistribution of automotive production has created distinct operational theatres. In Europe, particularly within the historic automotive manufacturing heartland of Germany, the traditional die-casting sector is undergoing a painful contraction. Surging energy prices, elevated raw material costs, and high interest rates have pushed profit margins in the German die-casting sector down to a precarious 5 to 7 per cent. The recent insolvency of the AE Group, a prominent German automotive supplier, perfectly exemplifies this crisis.

Conversely, the rapid expansion of Giga casting capacity within China has triggered an intense domestic price war. The average profit margin for the Chinese automotive industry fell from a healthy 6.1 per cent in 2021 to a highly constrained 2.9 per cent by early 2026. While Chinese foundries possess a distinct structural cost advantage in tooling procurement, the saturation of the domestic market is pushing them to aggressively export their manufacturing capabilities. This dynamic place severe pricing pressure on Western competitors.

The global aluminium casting usage is expected to reach 24.2 million tonnes in 2026. To know about the future market trends, prebook our upcoming report “Global Aluminium Casting Market 2026-2032”

Faced with the existential threat of automakers directly purchasing giga-presses and bypassing the traditional supply chain entirely, Tier 1 suppliers are executing divergent strategies to remain relevant.

One of the most consequential strategic manoeuvres was the decision by Nemak to acquire the automotive division of GF Casting Solutions. This USD 336 million deal provides immediate access to premium Western automakers alongside high-growth Chinese electric vehicle manufacturers. This acquisition underscores the absolute necessity of massive scale to compete effectively in the structural casting arena.

While Nemak pursued global consolidation, Japanese suppliers are sharply divided on the optimal press tonnage. Ryobi Limited is fully committing to the massive giga-scale, investing roughly USD 35.2 million in massive presses. Conversely, Aisin Corporation is strongly advocating for a modular approach. Aisin aims to utilise 4,000-tonne class machines. By designing vehicle structures so that a massive component is divided into two modular sections, Aisin can repurpose existing foundry infrastructure and drastically minimise upfront capital expenditure.

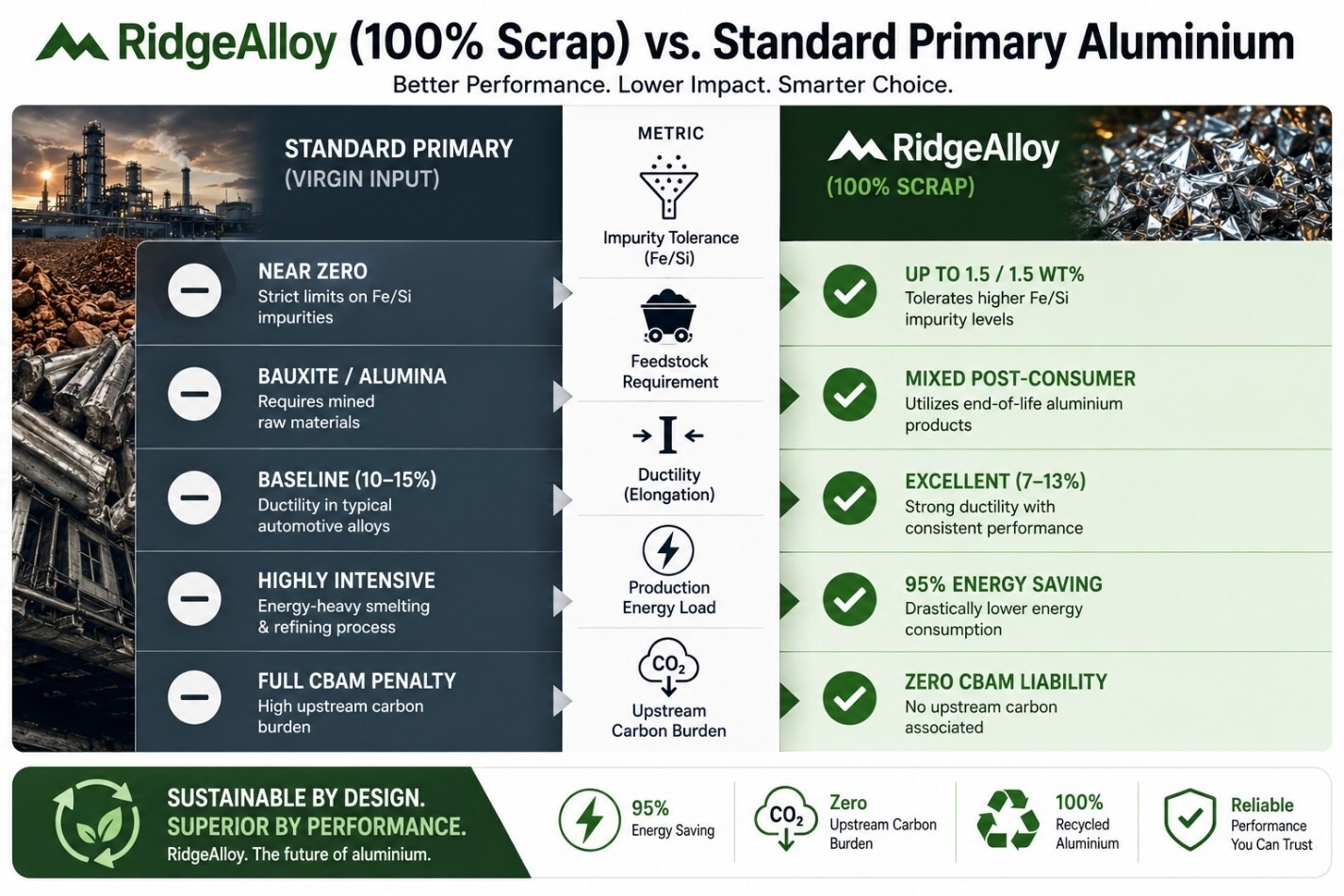

The greatest threat to the upstream primary aluminium sector is the metallurgical science currently occurring within the die cavity.

Historically, downstream casters were forced to buy virgin primary metal to dilute their dirty, post-consumer scrap. Standard secondary structural alloys cannot absorb elevated iron and silicon levels without precipitating brittle intermetallic phases. This chemical limitation has fundamentally protected primary smelter volume for decades.

That protective barrier is collapsing. To solve this critical bottleneck, researchers at the U.S. Department of Energy’s Oak Ridge National Laboratory engineered a groundbreaking material known as RidgeAlloy. Formulated using high-throughput computing, this novel composition is specifically designed to tolerate extreme impurity loads.

This image is generated with an AI tool and does not depict any real-time moment

This geographic redistribution of automotive production has created distinct operational theatres. In Europe, particularly within the historic automotive manufacturing heartland of Germany, the traditional die-casting sector is undergoing a painful contraction. Surging energy prices, elevated raw material costs, and high interest rates have pushed profit margins in the German die-casting sector down to a precarious 5 to 7 per cent. The recent insolvency of the AE Group, a prominent German automotive supplier, perfectly exemplifies this crisis.

Conversely, the rapid expansion of Giga casting capacity within China has triggered an intense domestic price war. The average profit margin for the Chinese automotive industry fell from a healthy 6.1 per cent in 2021 to a highly constrained 2.9 per cent by early 2026. While Chinese foundries possess a distinct structural cost advantage in tooling procurement, the saturation of the domestic market is pushing them to aggressively export their manufacturing capabilities. This dynamic place severe pricing pressure on Western competitors.

The global aluminium casting usage is expected to reach 24.2 million tonnes in 2026. To know about the future market trends, prebook our upcoming report “Global Aluminium Casting Market 2026-2032”

Faced with the existential threat of automakers directly purchasing giga-presses and bypassing the traditional supply chain entirely, Tier 1 suppliers are executing divergent strategies to remain relevant.

One of the most consequential strategic manoeuvres was the decision by Nemak to acquire the automotive division of GF Casting Solutions. This USD 336 million deal provides immediate access to premium Western automakers alongside high-growth Chinese electric vehicle manufacturers. This acquisition underscores the absolute necessity of massive scale to compete effectively in the structural casting arena.

While Nemak pursued global consolidation, Japanese suppliers are sharply divided on the optimal press tonnage. Ryobi Limited is fully committing to the massive giga-scale, investing roughly USD 35.2 million in massive presses. Conversely, Aisin Corporation is strongly advocating for a modular approach. Aisin aims to utilise 4,000-tonne class machines. By designing vehicle structures so that a massive component is divided into two modular sections, Aisin can repurpose existing foundry infrastructure and drastically minimise upfront capital expenditure.

Also read: The intelligence gap in aluminium casting and how to bridge it

The greatest threat to the upstream primary aluminium sector is the metallurgical science currently occurring within the die cavity.

Historically, downstream casters were forced to buy virgin primary metal to dilute their dirty, post-consumer scrap. Standard secondary structural alloys cannot absorb elevated iron and silicon levels without precipitating brittle intermetallic phases. This chemical limitation has fundamentally protected primary smelter volume for decades.

That protective barrier is collapsing. To solve this critical bottleneck, researchers at the U.S. Department of Energy’s Oak Ridge National Laboratory engineered a groundbreaking material known as RidgeAlloy. Formulated using high-throughput computing, this novel composition is specifically designed to tolerate extreme impurity loads.

This image is generated with an AI tool and does not depict any real-time moment

This image is generated with an AI tool and does not depict any real-time moment

RidgeAlloy can successfully accommodate up to 1.5 wt% iron and 1.5 wt% silicon simultaneously. These are impurity levels that would instantly embrittle conventional alloys, yet RidgeAlloy maintains a highly ductile elongation rate. If deployed at scale, this possesses the potential to displace up to half of primary aluminium production for automotive castings. Downstream innovation is actively severing its reliance on primary smelting volume.

Even with perfectly calibrated alloy chemistry, the physical mechanics of injecting molten aluminium into a 1.5-metre die cavity present profound quality control limitations. At injection velocities exceeding 50 metres per second, the metal flow is inherently violent. This turbulent flow traps oxidised surface skins, creating destructive oxide bifilms that dictate the fatigue life of the component.

To fundamentally solve these limitations, the industry is increasingly turning toward Semi-Solid Metal (SSM) processing, specifically rheocasting.

Rheocasting diverges from traditional casting by manipulating the aluminium alloy not as a fully liquid melt, but as a semi-solid slurry. When mechanical pressure is applied, the slurry flows smoothly into complex mould geometries using laminar flow. Because the material fills the mould as a highly viscous, cohesive front, it effectively pushes ambient air ahead of it. This prevents the chaotic fold-over mechanisms that generate destructive oxide bifilms.

This methodology creates a highly dense, forge-like internal structure with near-zero entrainment porosity. It is rapidly emerging as the gold standard for producing the most thermally and dimensionally demanding components in the electric drivetrain.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

As electric vehicle platforms continuously increase in power density, managing the thermal loads generated by traction motors requires highly efficient, active liquid cooling systems. Casting standard, lightweight aluminium tubes directly into a die-cast component is physically impossible, as extreme injection pressures instantly crush the hollow tube.

To overcome this bottleneck, a specialised consortium initiated the CoolCast research project to develop the ZLeak Tube technology. This breakthrough utilises a highly specialised, two-layer sacrificial filler insert placed inside an aluminium tube before it is set into the casting die.

During the violent injection process, this solid filler matrix provides the internal resistance necessary to prevent the aluminium tube from collapsing. Once the casting solidifies, the internal filler structure is flushed out using high-pressure water. This leaves behind a perfectly formed, inherently leakage-free hollow cooling channel seamlessly bonded within the monolithic casting.

The final verdict: The MSME survival pivot and the future of casting

The giga-casting revolution, as chronicled throughout this three-part series, began as an arms race for massive press tonnage. However, the true future of the global automotive foundry is not simply about building larger machines; it is about absolute metallurgical control.

The market is aggressively trending toward a bifurcated supply chain. Massive OEMs and consolidated Tier 1 giants will dominate the structural body-in-white market, utilising high-impurity secondary metals like RidgeAlloy to insulate themselves from primary market volatility and carbon taxes.

For Micro, Small, and Medium Enterprises (MSMEs), trying to compete on sheer press tonnage is a guaranteed path to insolvency. The survival playbook for the MSME sector relies entirely on strategic specialisation. MSMEs must abandon the high-volume, low-margin commodity die-casting market. Instead, they must aggressively pivot into the exact precision spaces that a 9,000-tonne press physically cannot execute.

By mastering semi-solid metal rheocasting and integrating active thermal management technologies like ZLeak, mid-tier MSME foundries can secure the highly lucrative contracts for EV motor housings, complex inverter casings, and hermetically sealed sensors. The giga-casting era will not eradicate the traditional supply chain; it will ruthlessly filter it. The foundries that survive the next decade will be those that accept a fundamental new truth: assembly is no longer the primary cost driver-metallurgy is.

Note: This is exclusive coverage by AL Circle and may not be reproduced, republished or shared without prior permission.

Responses