您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

This image is generated with an AI tool and does not depict any real-time moment

Aluminium demand is visibly entering another phase of transition. Until a few years ago, the demand used to be largely driven by packaging, transportation and the electrical and electronics sectors. Then came renewable energy, infrastructure, and electric vehicles, adding a fresh layer of demand for the metal. And now, data centres emerge as a new demand engine for the metal.

{alcircleadd}The rapid expansion of artificial intelligence, cloud computing and digital infrastructure is creating an increasing requirement for materials that can support high-performance cooling, reliable power distribution and large-scale structural systems. Since aluminium fits into this equation because of its thermal conductivity, light weight, corrosion resistance, formability and cost advantage over several competing materials, it is largely gaining demand in data centres.

However, this demand story is not one-sided. Data centres may lift aluminium consumption, but they are also intensifying competition for the same resource that aluminium producers depend on most, and that is electricity. So, if the opportunity is real, then the pressure is also.

Why aluminium matters for data centres

Heat dissipation and cooling systems, power distribution, structural frameworks, and building & containment are the four key areas in data centres where aluminium application is most visible. Industry reports indicate aluminium demand for the internal infrastructure of data centres is likely to peak around 1.1 million tonnes between 2025 and 2030, representing an 8 to 10 per cent compound annual growth rate. 55 per cent of this demand is estimated to be driven by cooling systems and 25 per cent by racking and enclosures.

However, aluminium demand linked to data centres does not stop inside the facility. A significant volume is also driven by grid upgrades, transmission networks and on-site power infrastructure. The demand begins at the facility boundary and then moves inward, as operators increasingly build their own power systems to manage slow grid connections and tightening local power availability.

On-site power infrastructure is also becoming more diverse. Data centre operators are now looking at solar and wind projects with storage, gas engines and turbines, solid oxide fuel cells and emerging small modular reactor concepts. Each of these systems creates additional material demand, particularly for aluminium used in power distribution, cabling support, structural systems and thermal management.

So, the next major demand push is expected to come from the grid itself. Annual power capacity additions for data centres are projected to rise from 15 to 20 gigawatts to a peak of approximately 30 to 33 gigawatts in the early 2030s.

This growth, however, is expected to continue till the early 2030s and then start plateauing and declining at approximately 2 to 3 per cent per annum as efficiency gains and AI-led design optimisation reduce material intensity.

But until then, the momentum is likely to remain strong. The global data centre sector is estimated to grow at a 14 per cent CAGR through 2030, requiring an investment of up to USD 3 trillion. By 2030, data centre capacity is estimated to exceed 100 GW, almost double today’s installed base.

Where is aluminium needed?

Aluminium’s high thermal conductivity makes it suitable for heat sinks, heat exchangers and cooling fins in data centres as servers and networking equipment generate large volumes of thermal energy, making temperature control critical to performance and reliability. Aluminium extrusions can also be designed with complex fin geometries that increase surface area and improve heat dissipation across passive convection, forced-air and liquid-cooling systems.

In addition, aluminium plays an important role in aisle containment systems. Ceiling panels, vertical partitions, containment walls and doors can be made from aluminium because the material is modular, durable and easy to reconfigure when rack layouts change.

In power distribution, aluminium busbars serve as high-current electrical conductors in busway and upstream power distribution systems. Since the metal has lower electrical conductivity than copper, it offers advantages in weight and cost. This makes it a practical option in applications where larger cross-sections can offset the conductivity difference without creating excessive structural load.

Data centre interiors also require a wide range of aluminium-based components. These include cable management systems, equipment enclosures, mounting frames, modular wall systems, partition framing and ceiling grid structures.

All these aluminium extrusions are made of specific aluminium grades. For instance, thermal management extrusion profiles are made of 6061 and 6063 billets, structural framing and modular T-slot systems are made of 6063, 6060, 6061 and 6082, and enclosure systems, cable management components and electrical applications use 1050, 1070 and 3003 grades.

Aluminium use in data centres in terms of volume

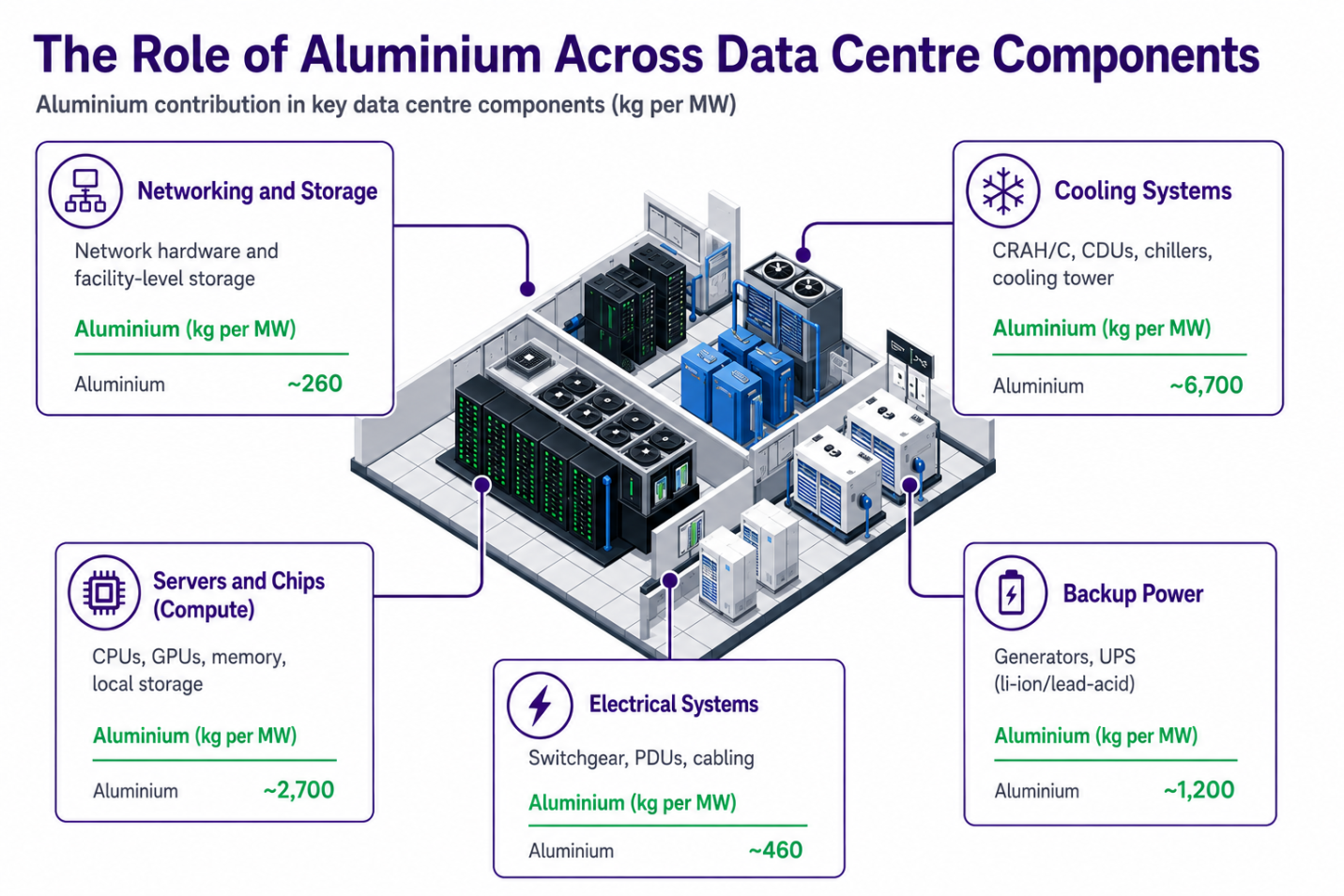

The volume of aluminium applications in data centres varies significantly across areas. In networking and storage, around 260 kg of aluminium is used per MW of capacity for network hardware and facility-level storage systems. Cooling systems account for a much larger share, with nearly 6,700 kg of aluminium per MW used in CRAH/C units, CDUs, chillers and cooling towers.

Servers and chips also represent a sizeable consumption area, with approximately 2,700 kg of aluminium per MW used across CPUs, GPUs, memory and local storage components. Meanwhile, electrical systems and backup power infrastructure require around 1,200 kg of aluminium per MW, mainly for generators and UPS systems based on lithium-ion or lead-acid battery technologies.

On average in the industry, each megawatt of data centre embeds around 60-75 tonnes of minerals, mainly in power and cooling systems, rather than servers.

Who leads the demand outlook?

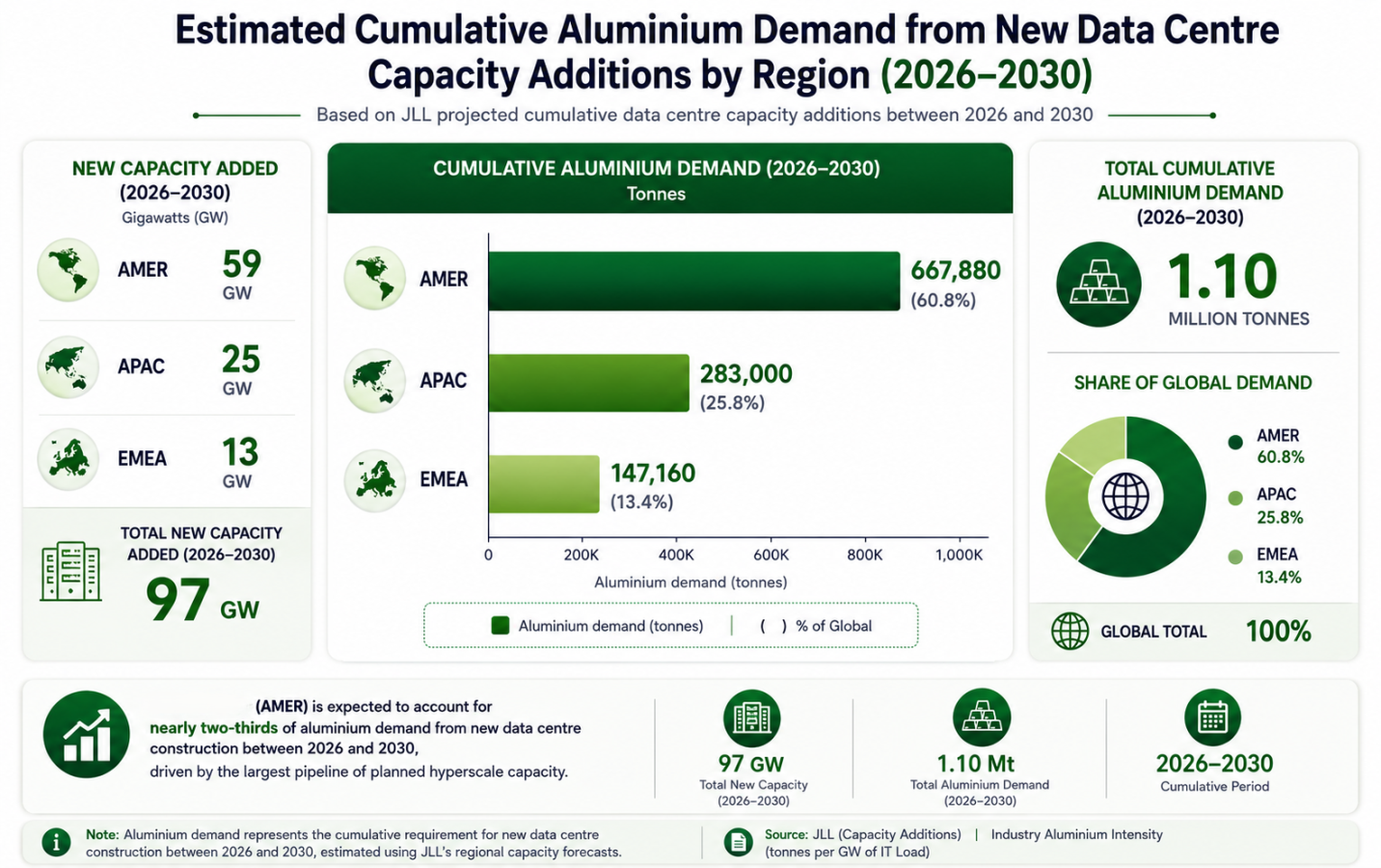

As per the available data, the demand for aluminium is likely to be skewed towards the Americas. Estimates suggest the region is likely to account for 667,880 tonnes of data centre demand, representing a 60.8 per cent share of the world’s total demand. Asia-Pacific is likely to be the second-highest aluminium demand driver for data centres, taking it to 283,000, accounting for 25.8 per cent of the global cumulative demand, followed by Europe, Africa, and the Middle East (EMEA) to drive the demand of 147,160 tonnes, which represents 13.4 per cent of the total demand.

These volumes indicate that the Americas will lead aluminium demand in data centres by 2030, accounting for 60.8 per cent of the cumulative demand. North America alone is likely to account for more than 40 per cent of the demand. Also, in terms of the number of data centres, the United States leads with 4,423 units, followed by the United Kingdom with 555 units and Germany with 523 units.

Turkey, as part of West Asia, also illustrates this broader trend. The country has been actively strengthening its position as a regional digital hub, supported by growing investments in cloud services, AI adoption and digital transformation programmes. According to industry estimates, Turkey's data centre market is expected to expand from 66 MW of installed IT capacity in 2025 to approximately 140 MW by 2030, representing a compound annual growth rate (CAGR) of 16.2 per cent.

Other countries with the next highest numbers of data centres include France (394 units), China (369 units). India (296 units), Canada (288), Australia (284), Japan (257 units), and Italy (252 units).

For aluminium, the relevance is clear. Fast-growing digital markets need reliable, energy-efficient infrastructure. That creates demand for aluminium in cooling systems, structural applications, electrical components and power-support infrastructure.

Yiğit Kasapoğlu, Director of RUSAL's Representative Office in Turkey, commented:"AI infrastructure is gradually emerging as a new driver of aluminium demand globally. The expansion of data centres requires substantial investments in energy, engineering and construction infrastructure, where aluminium's unique combination of properties makes it an increasingly valuable material. This trend is becoming particularly visible in rapidly digitalising economies, including Turkey."

As digital transformation accelerates worldwide, RUSAL continues to monitor emerging opportunities for aluminium across data centres, electricity networks, renewable energy integration and other advanced infrastructure segments that support the growth of the digital economy.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

Data centre capacities around the world

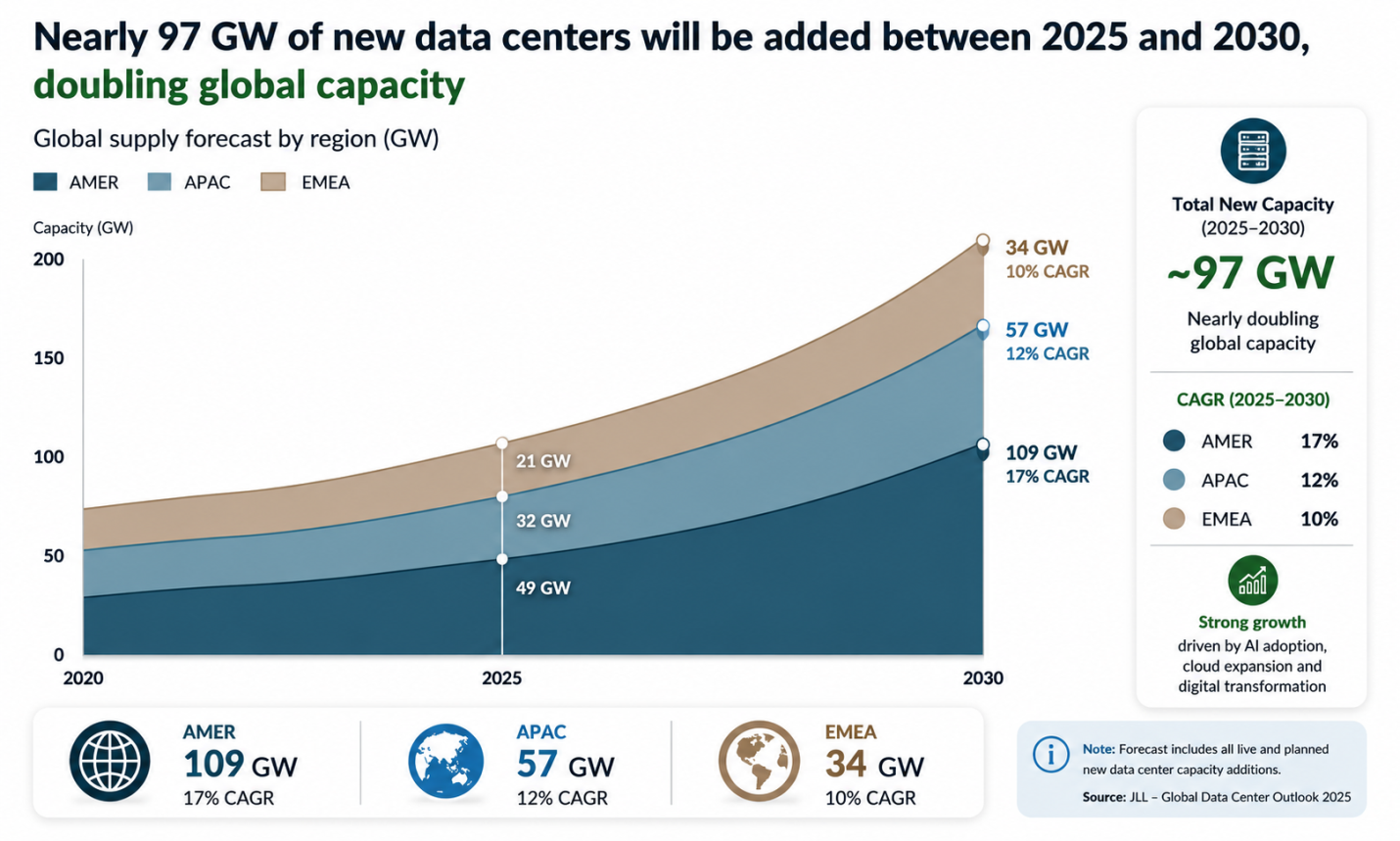

In terms of capacity, around 59 GW of new capacity is planned to be installed in the Americas, followed by 25 GW in Asia-Pacific and 13 GW in Europe, Africa, and the Middle East. In total, 97 GW of new capacity is estimated to be added across these regions. In 10 years' time, data centre capacity in the Americas is estimated to grow by 17 per cent CAGR during 2020-2030. Until 2025, the capacity was 49 GW.

Already, US Midwest aluminium manufacturers are seeing a shift in the demand environment with the rise of data centre construction. Especially, after a dip in the booming aluminium demand from EV sectors following the suspension of electric vehicle purchase incentives by the Trump government, aluminium manufacturers are eyeing potential demand growth from data centres and artificial intelligence infrastructure.

Bennett added that Metra North America, an aluminium extruded company, expects its aluminium product demand from data centre customers to be up by "several per cent" in 2026, while overall demand growth for the general US aluminium extrusion market is expected to range from 0 to 1.5 per cent.

The growth rate in 10 years in Asia Pacific is likely to be recorded at 12 per cent CAGR, as capacity until 2025 was 32 GW. In Europe, the Middle East, and Africa, the capacity growth rate during 2020-2030 is projected to be a 10 per cent CAGR. Until 2025, the capacity was 21 GW.

In Russia, the commercial capacity of data centres is 1,210 MW, with over 250 active facilities. Over 60 per cent of data centre capacity is clustered around the Moscow region. The data centres market in Russia is valued at roughly USD 2.95 billion in 2026 and is estimated to grow at a 14.4 per cent CAGR.

Explore aluminium extrusion suppliers, products and active trade opportunities on our marketplace

However, the tussle for power cannot be ignored

And finally, we reach that part of the story that depicts the perplexed chemistry between data centres and the aluminium industry. While on one hand, data centres need aluminium, on the other, they are competing with the metal for power. Both data centres and the aluminium industry survive on massive electricity supply, and the former secures a large part of the volumes, often at competitive or premium rates.

Moreover, with the number of data centres expanding, electricity demand is skyrocketing. Global demand for electricity, driven by the rapid expansion of artificial intelligence, is surging toward 950 TWh by 2030. Per the Bank of America, electricity demand in the United States is expected to grow 5 to 10 times faster over the next 10 years compared to the previous decade.

In 2024, global data centre electricity consumption was roughly 415 terawatt-hours, according to the International Energy Agency, which is equivalent to the annual use of Italy. Europe expects data-centre electricity demand to almost double to 36 gigawatts by the end of the decade.

This creates a strategic tension. The same sector that is opening a new aluminium demand channel may also increase the cost and scarcity of power needed to produce the metal.

The United States already shows signs of this pressure. The average electricity price to industrial customers has risen by 24.9 per cent from 2015 to 2025.

In a country like Nordic, which used to be considered an oasis of abundant clean energy, grid operators warn that demand from data centres will tighten electricity capacity faster than expected.

Hence, in the long run, electricity availability at uncompetitive prices is expected to be under strain for power-intensive industries like aluminium. This is a dual paradox for the industry. Just as Big Tech’s data centre boom is triggering new demand for aluminium, the industry’s insatiable desire for power and its capability to purchase it at higher market costs is disrupting the domestic production of the metal.

Responses