您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

As 2026 begins, the upstream aluminium value chain is expanding under rising pressure. New capacity is coming online, capital is returning to upstream assets, and prices are reacting more sharply to supply risk. Leadership reshuffles and cross-border partnerships point to a sector repositioning for tougher competition. Growth is no longer simple - the industry is adjusting as scale, resource control and market influence are being renegotiated across the chain.

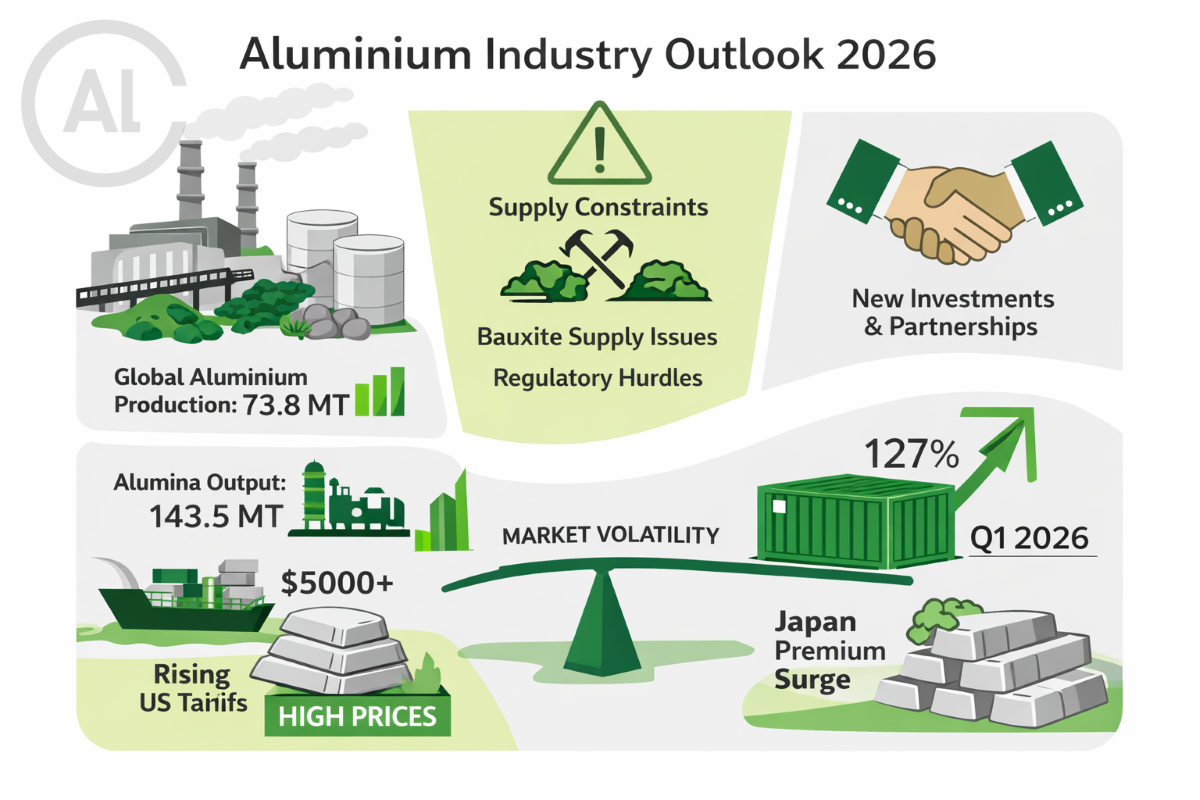

{alcircleadd}According to the International Aluminum Institute, primary aluminium production increased only 1.06 per cent in 2025 compared to 2024’s increase of 3.24 per cent. Annual growth was typically maintained at between 2.4 per cent and 2.9 per cent during the four years from 2020 through 2023; therefore, the current growth rate is reflective of an anomalous soft year as opposed to being a typical volatility within an established trendline. World production was 73.784 million tonnes versus 73.009 million tonnes in 2024. Average daily output increased from 199,500 tonnes per day to 202,100 tonnes per day.

The slowdown reflects weakening GCC output and China nearing its 45-million-tonne ceiling - two structural limits pressing on the world’s largest supply base.

Aluminium Upstream Weekly Recap by AL Circle Pvt Ltd

At the same time, alumina moved on a different clock. Smelter-grade production rose from 134.2 million tonnes in 2023 to 136.9 million tonnes in 2024 and is expected to reach between 143.3 and 143.6 million tonnes in 2025. The nearly seven-million-tonne jump is not a speculative surge but backlog capacity finally entering ramp-up. There will also be 0.8-million-tonne surplus in 2025. AL Circle estimates smelter-grade alumina demand could reach about 145.2 million tonnes in 2026, with the broader market nearing 147 million tonnes.

Explore- Most accurate data to drive business decisions with our Outlook 2026 insights across the value chain

What company results reveal about the sector

Corporate performance across the sector suggests operators are executing well. The pressure sits further back in the chain.

Metro Mining finished 2025 with 6.2 million wet tonnes shipped, including 543,000 tonnes in December. The company closed the year with AUD 57 million in cash and reduced junior liabilities that management says improved leverage. Leadership changes follow in 2026. Mine and marine operations at Bauxite Hills are now integrated under Paul Green as Executive General Manager Operations. Troy McMillan joins as General Manager, People & Culture. CFO Nathan Quinlin expands his role into supply chain planning, operational performance and margin optimisation.

Rio Tinto posted record bauxite production of 62.4 million tonnes, up 6 per cent from 58.7 million tonnes in 2024. Quarterly performance was uneven, but the full year shows steady operational discipline rather than volatility. For the complete story click: here.

Vedanta’s December quarter underlined how aluminium pricing strength feeds through to earnings. Net profit reached INR 571 billion, up 60.1 per cent year-on-year. Revenue rose 19 per cent. Other income also improved. Yet the same results sit beside a raw material constraint that has not been solved.

Regulatory delays, legal challenges and community resistance - including the halted Sijimali bauxite mine in Odisha and pending environmental and forest approvals - continue to slow captive mining. As a result, the company remains heavily reliant on imports. Long-term cost competitiveness depends on approvals that are still uncertain.

Also read: From bauxite to alumina: key projects redefining aluminium supply in 2025

Trade routes shift under policy pressure

Country-level flows show governments increasingly shaping where raw material moves.

Ukraine expanded bauxite imports by 23.7 per cent in 2025 to 43.5 thousand tonnes. In monetary terms, imports rose 15.8 per cent to USD 4.754 million. Turkey supplied 81.84 per cent of value, China 15.97 per cent and Guyana 2.19 per cent. Unlike 2023 and 2024, no re-exports took place. Click here.

China moved in the opposite direction, expanding alumina exports by 43 per cent year-on-year. December shipments alone rose 22.6 per cent month-on-month and 9.3 per cent annually to 205,863 tonnes. Russia remained the dominant destination with 2.02 million tonnes, accounting for 79.3 per cent of exports and marking a 24.7 per cent increase from 2024. Indonesia and the United Arab Emirates followed. For more details click here.

Europe chose restriction rather than expansion. After six months of review, the European Commission imposed anti-dumping duties between 88.7 and 110.6 per cent on Chinese fused alumina. To avoid severe supply disruption, a limited duty-free quota will apply for five years. Imports above that level face full tariffs. Read the full story here.

Also read: Aluminium Vision 2047 vs Reality in 2025: Ambition, progress and the gaps in between

New projects advance across the supply chain

New developments have not paused. It has narrowed its focus toward strategic positioning and downstream value.

Alpha HPA secured USD 225 million through an institutional placement, including USD 75 million backed by Australia’s National Reconstruction Fund Corporation and commitments from AustralianSuper and Orica. USD 210 million supports Stage 2 construction of the HPA First Project, USD 5 million upgrades Stage 1, and USD 10 million is allocated to corporate purposes. The Gladstone facility is expected to complete in late 2027 or early 2028.

Hindalco announced INR 210 billion for smelter expansion at its Odisha complex and INR 45 billion for flat-rolled and battery-grade foil production. The project sits inside a broader INR 370 billion Odisha capex plan and a INR 550 billion national expansion strategy. The smelter adds 360,000 tonnes annually, while the foil facility supports up to 100 GWh of lithium-ion manufacturing demand. Click here.

In the United States, Emirates Global Aluminium and Century Aluminum agreed to build the first new primary smelter since 1980. The Oklahoma plant targets 750,000 tonnes per year and is expected to create over 1,000 permanent jobs and 4,000 construction roles.

Previously idle capacity is also returning. RUSAL received approval to resume full operations along Guyana’s Berbice River and a two-year extension at Aroaima, with infrastructure rebuilding aimed at a full restart by 2027. Read here.

Guinea authorised Guinea International Corp and Sinohydro to resume bauxite mining following a confidential settlement. Indonesia is preparing for Nanshan Aluminium’s proposed 250,000-tonne facility in the Galang Batang Special Economic Zone, estimated at USD 436.57 million and pending approvals.

Prices start telling the story

Aluminium accounts for roughly 1.2–1.3 per cent of a projected USD 114 trillion global economy, yet each dollar of output supports USD 3–5 in downstream activity across infrastructure, transport and energy systems. When price signals distort, the wider economy feels it.

In the United States, buyers now pay a 68 per cent premium over London Metal Exchange prices after tariffs climbed from 10 to 25 to 50 per cent. Midwest delivery premiums add about USD 560 per tonne beyond tariff costs, pushing effective prices above USD 5,000 per tonne. The full story is here.

Japan’s import premium moved just as sharply. Mozal’s closure tightened supply into CBAM-affected markets and triggered a 127 per cent quarterly jump. The Q1 2026 benchmark reached USD 195 per tonne CIF, up from roughly USD 86 in Q4 2025. After a year of weak demand and falling settlements, the reversal signals how quickly the supply balance can shift. Expectations suggest the premium may hold into Q2.

Must read: Key industry individuals share their thoughts on the trending topics

Responses