您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

When aluminium prices moved this year, demand was not always the driving force. Sometimes the catalyst was a Guinean bauxite export terminal. At other times, it was a power contract in South Africa, tensions in the Strait of Hormuz.

{alcircleadd}Taken together, these developments reflected a broader shift in the upstream aluminium industry. Geopolitics, government policy and supply-chain resilience are increasingly shaping raw material flows, investment decisions and long-term market strategy.

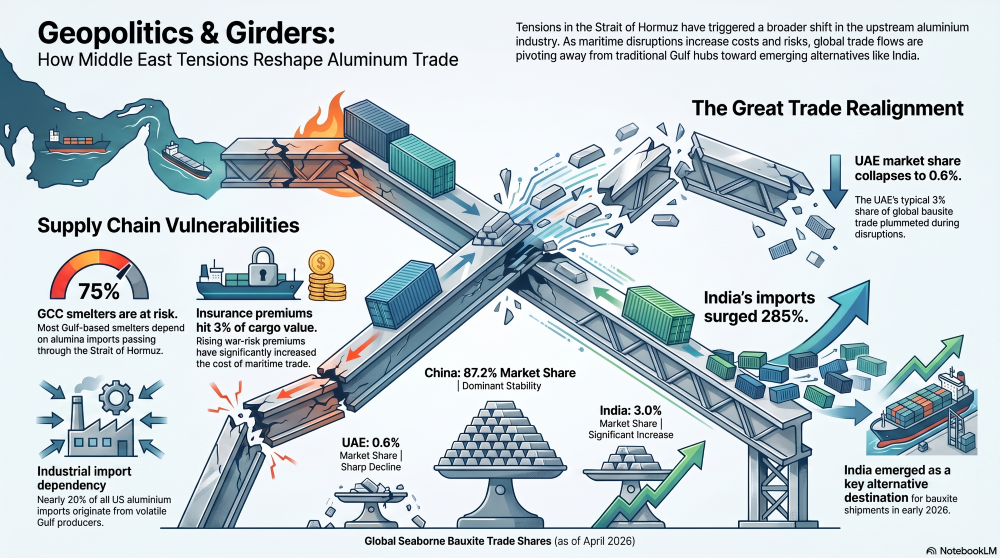

Strait of Hormuz disruption reshaped trade

The Middle East conflict highlighted the vulnerability of the aluminium supply chain to maritime disruptions. Tensions in the Strait of Hormuz caused higher freight costs, rising war-risk insurance premiums and shipping uncertainty disrupted bauxite movements into the Gulf, particularly the UAE.

As cargoes were redirected, global trade flows shifted. India emerged as a key alternative destination, significantly increasing its bauxite imports, while China maintained its dominant position as the world's largest buyer of Guinean ore.

Key takeaways

Middle East supply-chain risk

Trade routes shifted

Guinea's export surge drove changes across the bauxite market

Guinea remained at the centre of the upstream aluminium market as exports continued to rise and reinforced its position as China's primary supplier. However, higher export volumes also pushed prices lower as supply outpaced demand.

Attention later shifted from growing exports to the possibility of export restrictions, highlighting how policy decisions in a single producing country could influence global raw material availability.

Key takeaways

Guinea dominated China's bauxite supply

Prices fell despite higher trade volumes

Explore: The most comprehensive and forward-looking industry-focused report – Global Bauxite & Alumina Market Forecast to 2036: Supply–Demand, Trade Flows & Price Outlook

Export curb proposal created fresh uncertainty

South32's aluminium exit reflected a changing investment strategy

Corporate decisions during the period also reflected broader structural changes in the upstream industry.

Despite low LME aluminium inventories and expectations of a market deficit, South32 chose to reduce its exposure to aluminium by selling most of its business to Alcoa. The move underscored how rising electricity costs and long-term operating risks are increasingly influencing investment decisions.

For Alcoa, the acquisition strengthens its integrated mine-to-metal strategy and significantly expands its upstream presence.

Key takeaways

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

Responses

A proud

ASI member

AL Circle Private Limited | CIN: U72200WB2017PTC221175

Registered Office: Ecospace Business Park, Block 3A, Unit 401A, New Town, Rajarhat, Kolkata, WB 700160

Corporate Office: Ecospace Business Park, Block 3A, Unit 401A, New Town, Rajarhat, Kolkata, WB 700160

© 2026 AL Circle. All rights reserved. AL Circle is not responsible for content from external sources.