您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

When South32 agreed at the start of July to sell almost its entire aluminium value chain to Alcoa for up to USD 5.6 billion, the instinctive read was that a diversified miner had blinked and walked away from aluminium. The sharper question is the one the market keeps misframing: did South32 sell at the bottom, or did it finally price the single variable that decides an aluminium smelter’s life — power?

{alcircleadd}The “bottom” theory does not survive contact with the tape. Aluminium is trading near historic highs, not lows. The LME three-month price touched a four-year peak around USD 3,750 per tonne in early June before a roughly 9 per cent correction on Gulf de-escalation; even after that pullback, it holds above USD 3,100, more than 21 per cent higher year on year. LME stocks have fallen below 300,000 tonnes for the first time since 2022, Macquarie has the market in a deficit of about 930,000 tonnes this year, and alumina is holding near USD 330 per tonne. South32’s own alumina earnings had already been lifted by a roughly 45 per cent rise in realised prices through 2025. This is not a trough. The company is selling into strength, which means the decision is not a call on the price cycle. It is a call on the cost curve and on the part of that curve South32 could no longer control.

In aluminium, the cost curve is a power curve

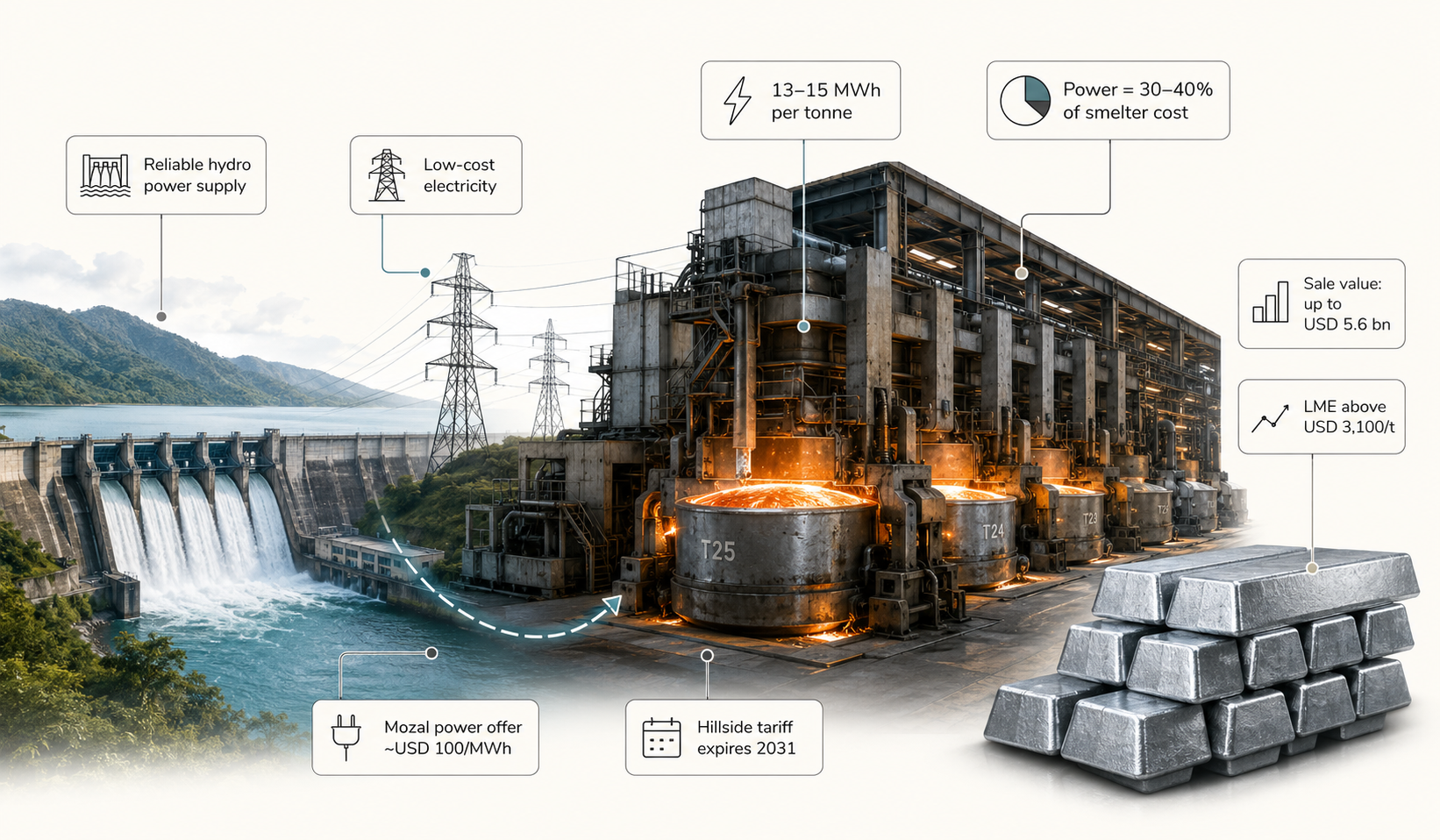

Primary aluminium is electricity in solid form. A Hall-Héroult smelter draws roughly 13–15 MWh for every tonne of metal, and power typically accounts for 30–40 per cent of the cost of production, more than alumina, carbon and labour combined. That one line item is why the industry’s economics are set by long-term electricity contracts, not by the LME screen. Outside China, fewer than one smelter in a hundred runs on power priced above USD 50/MWh. Above that level, the metal barely covers its own energy bill.

The physics make the exposure worse. The pots run continuously above 950°C, and the current cannot be switched off the way a mill or a mine can pause. A cold shutdown degrades the carbon lining, and an extended one destroys it. So when power economics turn against a smelter, the operator has no cheap option to idle and wait for a better year. The choice is to keep feeding an uncompetitive cost base or take the plant offline and treat restarting it as a capital project in its own right. That asymmetry is the whole game.

South32 no longer owned its cost position

Read the two Southern African assets through that lens, and the divestment stops looking like a cycle call. Mozal in Mozambique — 560,000 tonnes of capacity, built specifically around hydropower from Cahora Bassa — went onto care and maintenance in March after South32, the Mozambican government, HCB and Eskom deadlocked on price, with drought compounding the supply problem. The power on offer reportedly approached USD 100/MWh, roughly double the level above which a smelter outside China struggles to survive. A plant designed to run on cheap hydro could not secure it, and no amount of operating discipline closes a gap that size.

Hillside in Richards Bay is the larger and better asset—the biggest smelter in the Southern Hemisphere, around USD 2 billion of revenue and USD 200 million of EBITDA in 2025—but it sits on the same fault line. It runs today on an Eskom tariff discounted by roughly half against the standard large-user rate, and that arrangement expires in 2031.

On Alcoa’s own presentation, Hillside sits in the third quartile of the 2025 cost curve, while Worsley-Boddington and the Brazilian assets sit far lower. Hillside is a strong cash generator at today’s price and today’s tariff, but its cost position rests on a negotiated discount in a single jurisdiction with a strained grid, not on anything South32 controls. That is a cost position you rent, not one you own.

This is a structured exit, not a fire sale

The terms confirm the read. The headline is up to USD 5.6 billion, but the shape matters more than the number: about USD 3.1 billion in upfront cash, roughly USD 1 billion in Alcoa stock, some USD 750 million of assumed net debt and lease liabilities, and up to a further USD 750 million in contingent consideration — a contingent value right tied to alumina and aluminium prices over four annual periods from July 2026. Alcoa also assumes around USD 1.2 billion of rehabilitation provisions. A locked-box from 1 April and a 5 per cent annual ticking fee on the cash component protect South32’s economics through to completion.

Two features tell you this is not a distressed seller. First, aluminium contributed about 37 per cent of South32’s underlying earnings over the five years to FY25. You do not surrender a third of your earnings base at the bottom of a cycle unless you have concluded the problem is structural. Second, the contingent USD 750 million keeps South32 exposed to the upside if prices stay firm.

A seller who thought metal was cheap would want cash and a clean break; South32 kept a price-linked tail. That is a judgement about where it can win, not a bet that aluminium has peaked. Moody’s promptly placed the group on review for downgrade, citing the loss of scale and diversification — the honest price of simplification, not evidence of a mistake.

Alcoa is buying a cost curve it can actually move

The mirror image explains why Alcoa is the natural buyer. It is structurally long raw materials and was already a net seller of alumina, so adding Worsley and the Brazilian refineries gives it more say over Atlantic-basin alumina pricing and the option to feed its own smelters. Wood Mackenzie put the synergies at around USD 900 million, driven largely by Worsley’s proximity to Alcoa’s existing Western Australian operations, and calculates that the deal makes Alcoa the world’s largest bauxite miner, lifting its share from 8.5 per cent to 13 per cent, ahead of Rio Tinto, while raising smelting capacity by about a quarter. Its group aluminium cash cost barely moves; its bauxite cost actually falls, with Boddington among the lowest-cost bauxite mines in the world.

More to the point, Alcoa can do with Hillside what South32 could not: integrate it. A third-quartile smelter inside a mine-to-metal system, backed by an owner with the balance sheet and the incentive to sit across from Eskom until 2031, has a very different future from the same plant held by a diversified miner for whom it was one asset among many. There is a strategic layer too. With Chinese capacity effectively capped near 45 million tonnes, Western greenfield smelters carrying five-to-seven-year lead times, and CBAM and US tariffs reshaping trade flows, non-Chinese primary capacity is becoming scarce. Keeping Hillside with an operator willing to invest is worth more to Alcoa than the third-quartile cost line suggests in isolation.

The real lesson is about owning your cost driver, not timing the market

So, bottom or cost curve? On the numbers, this is not an exit at the bottom. Prices are high, and South32 sold into a strong year. It is a company reading its own cost position honestly and acting on it.

I have sat on the owner’s side of these decisions, and the discipline is always the same. Before you argue about the metal price, ask whether you control the variable that sets the plant’s margin. In aluminium that variable is power, and in South Africa and Mozambique South32 concluded it did not control it and could not fix the grid. Selling the metal was really selling the power risk to a buyer better placed to carry and reshape it, while keeping a priced claim on any upside. That is not surrender. It is the correct read of a cost curve that, in this industry, is a power curve first and a price curve second. The operations that get into trouble are the ones still betting on the LME to bail out a cost position they were never going to own.

This article was written exclusively for AL Circle.

The views expressed are the author’s own. All figures cited are drawn from publicly available information; this piece is opinion and analysis, not investment advice.

Responses

A proud

ASI member

AL Circle Private Limited | CIN: U72200WB2017PTC221175

Registered Office: Ecospace Business Park, Block 3A, Unit 401A, New Town, Rajarhat, Kolkata, WB 700160

Corporate Office: Ecospace Business Park, Block 3A, Unit 401A, New Town, Rajarhat, Kolkata, WB 700160

© 2026 AL Circle. All rights reserved. AL Circle is not responsible for content from external sources.