您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The images used in this article is generated with an AI tool and does not depict any real-time moment

Imagine it is the final trading week of December 2031. A cargo vessel loaded with Guinean bauxite is approaching a Chinese port after weeks at sea. An aluminium smelter in the Middle East is preparing to price its next monthly shipment to an automotive customer in Europe. A commodity trader in Singapore is rolling forward a hedge linked to the London Metal Exchange (LME), while a bank in London is calculating the value of aluminium inventories pledged as collateral under a trade finance facility.

{alcircleadd}Thousands of kilometres apart, these activities appear unrelated. Yet they all depend on one common factor: whether the LME is open for business.

To many outside the metals industry, the LME’s trading calendar is simply a schedule of exchange holidays and trading days. However, for aluminium professionals, it is far more than an administrative document. It acts as the industry’s operating timetable, influencing how aluminium is priced, hedged, financed, shipped and delivered across the world.

LME’s trading calendar represents the increasingly long planning horizons of a global aluminium industry where billion-dollar investments, decade-long supply agreements and sophisticated financial hedging strategies require certainty well beyond the current financial year.

In today’s market, understanding when aluminium can be traded has become almost as important as understanding where prices are heading.

Attend the webinar Hedging for recyclers - Become an expert in 6 hours to learn metal price risk management for recycling

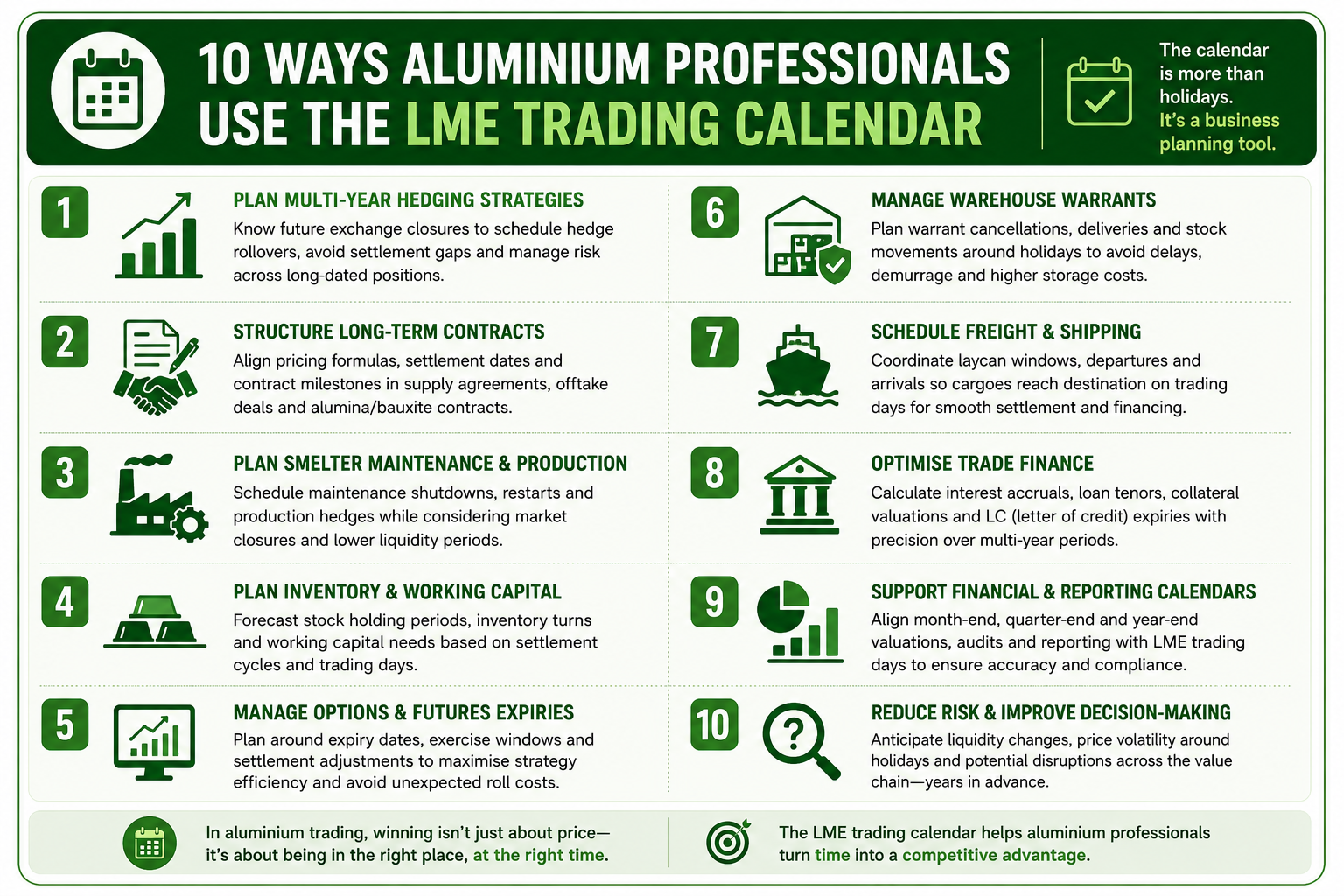

More than a calendar: A blueprint for global aluminium trading

Every commodity exchange publishes a trading calendar, but very few attract much attention. The LME’s calendar is different because the exchange itself is different.

Unlike most futures exchanges, which primarily offer standardised monthly contracts, the LME operates using a unique prompt-date system that mirrors the way industrial metals are physically bought and sold.

Traders can access daily prompt dates out to three months, weekly prompt dates from three to six months, and monthly prompt dates extending as far as 123 months, more than ten years into the future.

This extended timeline is not designed simply to accommodate speculative trading. It exists because aluminium, like a few other commodities, is fundamentally a long-cycle business.

A bauxite mine cannot be developed within a quarter. An alumina refinery cannot be financed on annual price expectations. A modern aluminium smelter is expected to operate for decades, while automotive manufacturers, beverage can producers and aerospace companies routinely negotiate procurement programmes spanning several years.

Why does aluminium need a ten-year horizon?

The industry’s investment cycle begins with bauxite mining, progresses through alumina refining and primary smelting, and continues into downstream rolling, extrusion, casting and fabrication before reaching end-use sectors such as automotive, construction, aerospace and packaging.

Each stage involves significant capital expenditure. Constructing a modern aluminium smelter with an annual capacity of around 750,000 tonnes can require investments exceeding USD 6 billion, alongside a construction period of five to seven years. Once operational, the facility depends on stable electricity supplies secured through long-term power purchase agreements (PPAs), as electricity typically accounts for roughly one-third of production costs.

Financiers supporting such projects need confidence that future revenues can withstand fluctuations in aluminium prices.

Rather than relying solely on today’s market price, producers and lenders can examine forward prices years into the future to estimate cash flows, assess debt-servicing capability and structure financing arrangements that remain viable throughout the project’s life.

What makes the LME different?

While the Chicago Mercantile Exchange (CME) lists aluminium futures extending approximately five years into the future, and the Shanghai Futures Exchange (SHFE) primarily concentrates liquidity in near-term monthly contracts, the LME provides forward visibility extending to 123 months.

It is also the only major exchange offering a combination of daily, weekly and monthly prompt dates across such an extended horizon.

Physical shipments rarely arrive on the final day of the month. Cargoes encounter weather delays, port congestion, customs inspections and geopolitical disruptions. Producers negotiate deliveries for specific business days rather than generic monthly periods.

The LME’s prompt-date structure therefore allows financial contracts to align much more closely with physical commercial activity.

This reduces what is known as timing risk for traders, i.e., the mismatch between the financial hedge and the actual physical delivery.

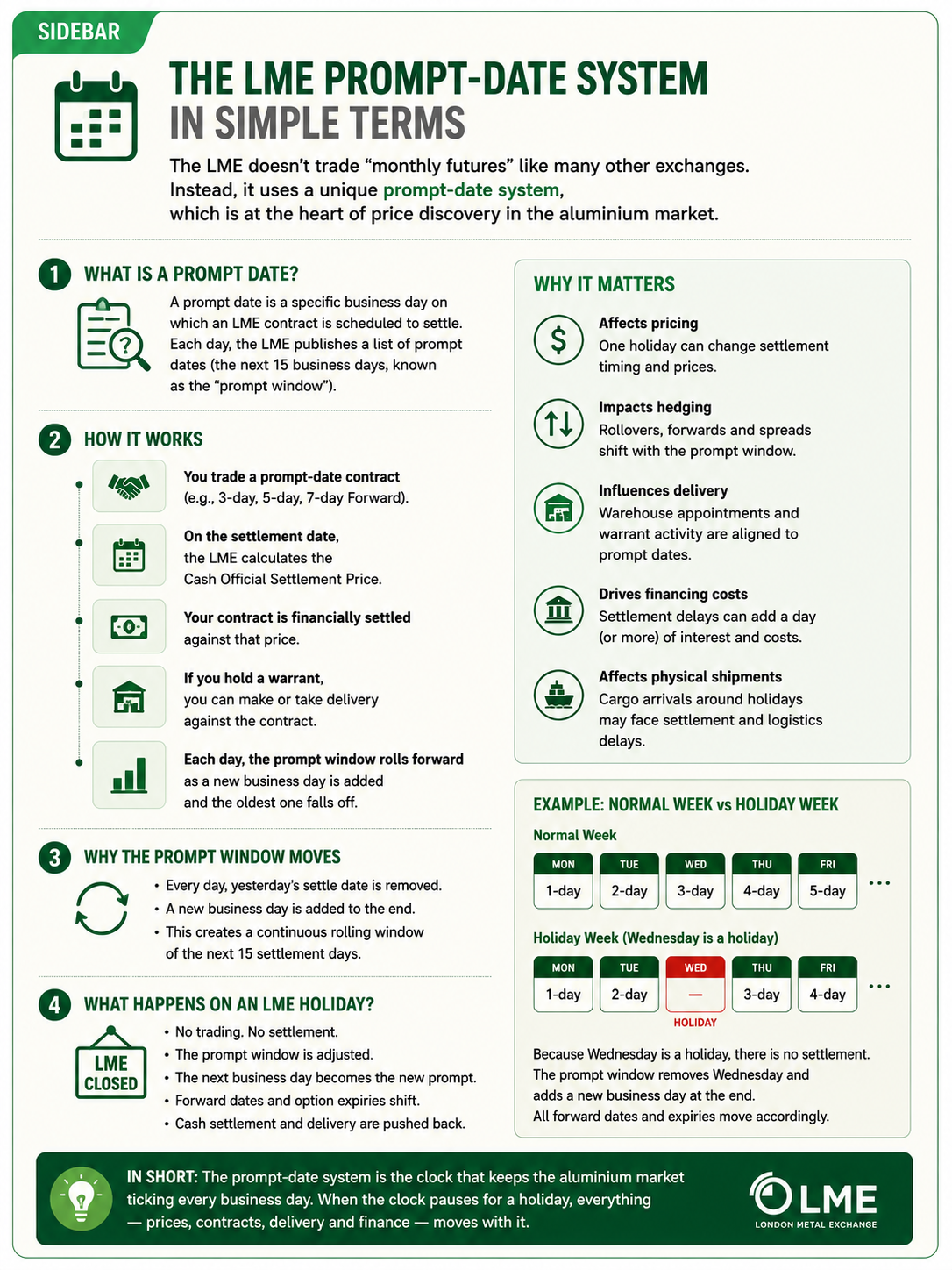

The prompt-date system: The industry’s invisible clock

At first glance, the phrase prompt date sounds highly technical. In reality, the concept is remarkably straightforward. A prompt date is simply the business day on which an LME contract settles.

Rather than concentrating all contracts into monthly expiry dates, the LME allows participants to choose settlement on specific business days. During the first three months, contracts can settle daily. Between three and six months, settlement shifts to weekly intervals, while contracts beyond six months settle monthly until the end of the ten-year curve.

Think of it as booking an airline ticket. Instead of choosing only ‘July’, travellers select a specific departure date. Similarly, aluminium traders often need contracts matching precise shipment schedules, production runs or customer delivery commitments.

This flexibility enables the LME to echo the realities of physical metals trading more accurately than traditional monthly futures markets.

It also explains why holidays matter so much. If the exchange closes on a scheduled prompt date, settlement moves. That shift affects every contract linked to that date.

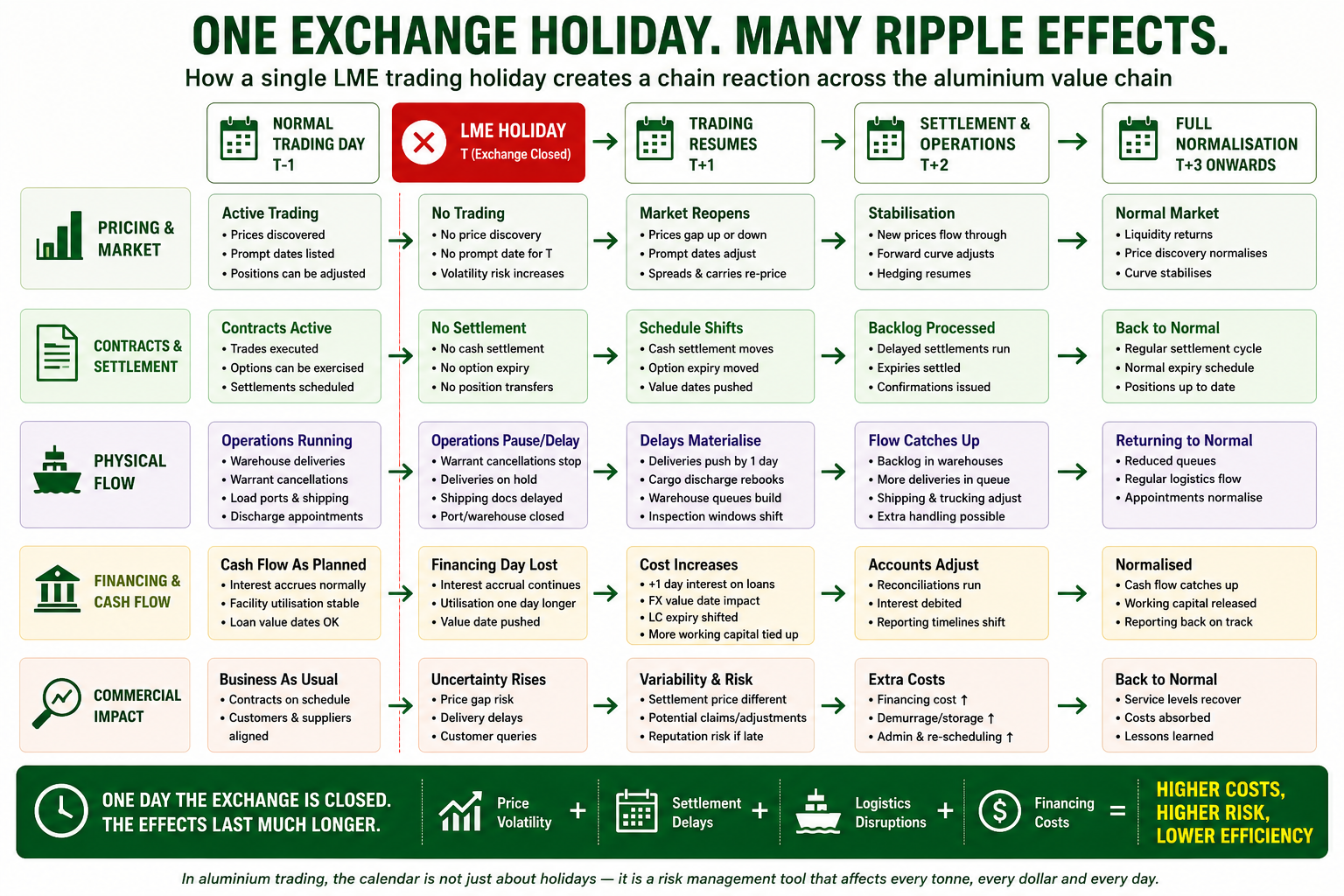

How one exchange holiday triggers a global chain reaction

To understand the importance of the trading calendar, consider what happens when the LME closes for a public holiday. The most immediate impact is on price discovery.

Without trading, there is no official cash settlement price for that day. Contracts referencing daily settlements must wait until trading resumes.

The impact extends to:

This is precisely why experienced traders treat the LME calendar as a risk-management tool rather than a holiday schedule.

Time has become a competitive advantage

Perhaps the most significant change in aluminium trading over the past decade is that the market has become increasingly synchronised.

Mining companies, refiners, smelters, traders, logistics providers, banks and downstream manufacturers no longer operate as isolated participants. They form an interconnected global ecosystem where commercial success depends on coordinating physical operations with financial markets.

Realistic example: How one exchange holiday can ripple through a five-year supply contract

Consider a Middle Eastern aluminium smelter supplying primary aluminium to a leading automotive manufacturer in the United States under a five-year offtake agreement.

Rather than fixing a price years in advance, the contract is linked to the LME Official Settlement Price over a specified quotation period, plus the US Midwest Premium, which reflects regional supply-demand dynamics, freight and logistics costs. Both parties also use the LME to hedge their price exposure, while banks, shipping companies and treasury teams coordinate financing and cargo movements around expected settlement dates.

Now imagine the quotation period ends during a week when the LME is closed for a public holiday.

Without an official settlement price, the pricing period shifts to the next available trading day. Hedge rollovers may need to be adjusted, invoices cannot be finalised until the revised settlement price is available, and treasury teams must update cash flow projections.

Meanwhile, the cargo continues its journey to North America. If it reaches the destination before financial settlement is completed, trade finance facilities, including letters of credit and working capital loans, may remain outstanding for an additional business day, increasing financing costs.

The challenge becomes even greater when regional premiums are volatile. Alongside the LME benchmark, traders must simultaneously manage exposure to the US Midwest Premium, freight costs and changing trade flows.

Explore- Most comprehensive and forward-looking industry-focused report — Global Bauxite & Alumina Market Forecast to 2036: Supply–Demand, Trade Flows & Price Outlook

The role of long-term offtake agreements

In the aluminium industry, trading houses frequently commit to purchasing a producer’s future output for several years. In return, producers often receive advance financing, enabling them to fund expansion projects or strengthen working capital.

These agreements are generally priced against LME reference prices, such as the Official Settlement Price or monthly average settlement values. Every shipment delivered over the life of the agreement is therefore linked to the exchange calendar.

Understanding market structure: Contango, backwardation and basis risk

One of the most valuable applications of a long-term trading calendar is helping traders manage changes in the shape of the forward curve.

Commodity markets generally move between two broad pricing structures.

In a contango market, forward prices are higher than spot prices. This typically reflects the cost of storing, financing and insuring physical metal over time. Under favourable conditions, traders may purchase aluminium today, place it into storage and simultaneously sell forward contracts to capture the difference between current and future prices.

Conversely, backwardation occurs when nearby prices exceed forward prices, usually signalling immediate physical tightness or supply shortages.

Neither condition is permanent.

As inventories fluctuate, geopolitical events unfold and demand changes, the forward curve continuously evolves.

For aluminium traders, understanding these shifts is critical because every hedge eventually needs to be rolled forward. The timing of those rollovers, combined with the structure of the forward curve, determines whether the trader incurs additional costs or generates carry income.

The calendar therefore serves as more than a scheduling tool—it provides the framework within which forward pricing strategies are executed.

When the physical market and financial market diverge

The aluminium market regularly demonstrates that prices alone do not tell the complete story.

During 2026, for example, LME warehouse inventories declined significantly as physical demand strengthened and sanctions affected the availability of deliverable metal. Opening stocks fell from approximately 420,000 tonnes at the beginning of the year to around 289,000 tonnes by July.

Ordinarily, declining inventories might be expected to push prices higher.

Yet market sentiment is influenced by many variables, including interest rates, economic growth expectations and currency movements. As a result, traders often observe situations where inventory levels and prices move in different directions.

This is precisely why sophisticated market participants monitor not only prices but also warehouse stocks, cancelled warrants, prompt dates and the shape of the forward curve.

The trading calendar provides the temporal framework that allows these variables to be interpreted together rather than in isolation.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

Why the calendar matters even more today

If the aluminium market had remained as it was twenty years ago, a ten-year trading calendar would still have been useful. Today’s market, however, is considerably more complex.

The rise of green aluminium, regional carbon pricing, geopolitical tensions and supply-chain diversification has fundamentally altered how aluminium is traded.

Trade barriers such as the United States’ Section 232 tariffs, evolving carbon border adjustment mechanisms in Europe, sanctions affecting Russian aluminium and shifting regional supply chains have all contributed to increased market fragmentation.

Instead of one global aluminium price, companies increasingly manage a combination of:

The dramatic movement in US Midwest premiums during recent trade disruptions demonstrated how delivered aluminium prices can diverge significantly from the underlying LME benchmark. Managing that basis risk over multi-year commercial agreements requires far more sophisticated planning than was necessary a decade ago.

As a result, the trading calendar has become an increasingly important tool for coordinating financial hedges with changing regional market conditions.

Note: This is exclusive coverage by AL Circle and may not be reproduced, republished or shared without prior permission.

Responses

A proud

ASI member

AL Circle Private Limited | CIN: U72200WB2017PTC221175

Registered Office: Ecospace Business Park, Block 3A, Unit 401A, New Town, Rajarhat, Kolkata, WB 700160

Corporate Office: Ecospace Business Park, Block 3A, Unit 401A, New Town, Rajarhat, Kolkata, WB 700160

© 2026 AL Circle. All rights reserved. AL Circle is not responsible for content from external sources.