您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The aluminium value chain moved through a week shaped less by routine output numbers and more by structural forces - environmental accountability, resource nationalism, tariff recalibration and fresh capacity ambitions. Across continents, governments and producers alike signalled that aluminium is increasingly tied to policy leverage and economic strategy.

{alcircleadd}Environmental reckoning and resource retention

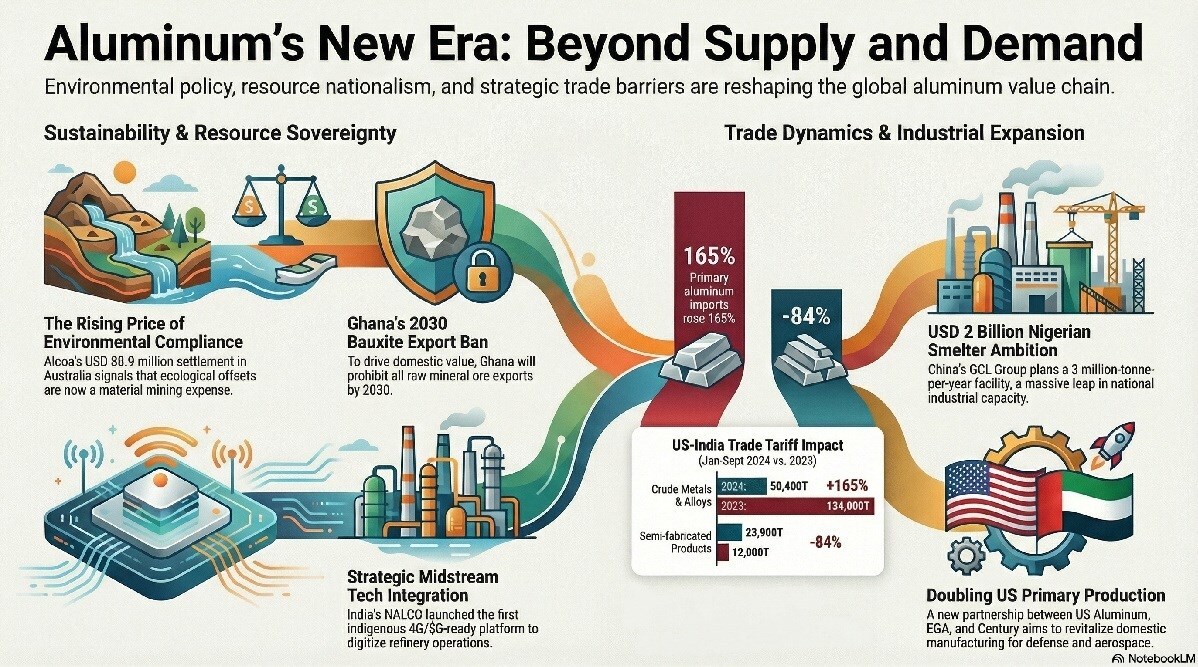

In Western Australia, long-running tensions between environmental authorities and mining operations resurfaced as Alcoa reached a settlement with the Australian Department of the Environment over bauxite extraction in the North Jarrah Forest, south of Perth. The company agreed to pay USD 38.9 million (AUD 55 million) in penalties linked to clearing 2,100 hectares between 2019 and 2025. Of this, USD 28.14 million will reportedly fund permanent ecological offsets to compensate for habitat destruction - underlining how environmental compliance is now materially shaping mining economics. To know more about it, click here.

At the same time, Ghana signalled a decisive shift in mineral policy. With bauxite reserves estimated at 900 to 960 million tonnes and production capacity between 1.5 and 1.8 million tonnes, the country is seeking to curb raw exports. Speaking on February 14 at the Accra Reset Addis Reckoning event in Addis Ababa, President John Dramani Mahama declared that by 2030, no mineral ore would leave Ghana, reinforcing a push toward domestic value addition. Read here.

For the global aluminium value-chain 2026 outlook, book our exclusive report “Global ALuminium Industry Outlook 2026"

Operational upgrades and strategic partnerships in alumina

Midstream developments reflected both technological modernisation and evolving supply-chain alignment.

NALCO strengthened digital connectivity at its Koraput alumina refinery in Odisha through the launch of a BSNL Base Transceiver Station using Swadeshi 4G technology - India’s first fully indigenous 4G (5G-ready) platform developed by C-DOT, Tejas (Radio Access Network), and TCS. The installation integrates domestic telecom capability into industrial operations. The full story is here.

In Australia, Impact Minerals marked a milestone in advanced materials as its 50 per cent-owned associate Alluminous shipped approximately 15 kilograms of HiPurA high purity alumina from its Perth pilot plant to Charge CCCV LLC (C4V) in the United States. The shipment, made under a Technology Development Agreement signed in December, came just nine months after Impact’s investment in the technology.

In Europe, Alteo entered into a logistics agreement with HES Fos, a subsidiary of HES International BV, to relocate a major portion of hydrated alumina logistics to Fos-sur-Mer. HES Fos will oversee vessel unloading, storage and delivery to Alteo’s industrial plant in Gardanne. Read here.

Trade barriers, market signals and inventory strain

Primary aluminium markets continued to be influenced by trade policy and exchange competition.

The Chicago Mercantile Exchange approved Taiwan and Hong Kong as new aluminium warehouse locations, expanding beyond Malaysia, Singapore and South Korea. The move strengthens CME’s presence in Asia - which accounts for two-thirds of global aluminium production - and intensifies its challenge to the London Metal Exchange.

Meanwhile, US-India aluminium trade flows shifted markedly in 2025 following tariff actions. Washington imposed a 25 per cent tariff under Section 232 in March and later raised tariffs on aluminium and steel imports, including derivative products, to 50 per cent on June 4. From January to September 2025, the United States imported 134 thousand tonnes of crude metals and alloys and 12 thousand tonnes of semi-fabricated aluminium products from India. During the same period in 2024, imports totalled 50,400 tonnes of primary aluminium and 23,900 tonnes of aluminium products. Year-on-year, primary aluminium shipments rose 165 per cent, while aluminium product imports declined by roughly 84 per cent, according to USGS data. Read the whole story here.

Amid declining aluminium stocks and pressure from businesses, US Trade Representative Jamieson Greer indicated that while broader tariffs could be recalibrated, the core measures would remain in place, describing them as “very successful.” The review comes as President Trump faces criticism over rising living costs ahead of November midterm elections.

Australia is also reassessing its trade footing after President Donald Trump announced plans for a new 15 per cent tariff on all imports. The proposal follows a US Supreme Court ruling that struck down the sweeping “reciprocal” tariffs introduced in April last year, overturning the 10 per cent “liberation day” tariff while leaving intact the sector-specific 50 per cent duties on steel and aluminium. Click for more.

Expansion ambitions and national economic stakes

Beyond policy friction, the week underscored aluminium’s central role in industrial planning.

Vedanta Aluminium, India’s largest primary aluminium producer with around half of the domestic primary market share, continues to position itself to benefit from India’s 6 per cent annual aluminium demand growth, well above global averages. The company is expanding capacity and planning to operationalise captive mines to secure raw material supply, banking on aluminium’s role in infrastructure, automotive, aerospace, power transmission and clean-energy sectors. Read here.

In Mozambique, the International Monetary Fund warned that the suspension of the Mozal aluminium smelter in Maputo province poses significant downside risks. Owned by Australia’s South32, the smelter - representing 4 per cent of Mozambique’s GDP - is scheduled to move into care and maintenance from mid-March after failing to secure a new electricity supply agreement at competitive US tariffs. Read here.

In the United States, US Aluminum Company signed an agreement with Emirates Global Aluminium (EGA) and Century Aluminum to explore developing a fabrication plant near the planned Oklahoma Primary Aluminium smelter in Inola. The broader project aims to double US primary aluminium production, with the downstream plant targeting the electrical, defence, aerospace, automotive and machinery sectors.

Nigeria also reopened its aluminium ambitions as Minister of Steel Development Shuaibu Abubakar Audu received a delegation from China’s GCL Group. The firm signalled plans for a 3 million-tonne-per-year primary aluminium smelter, with projected costs exceeding USD 2 billion - potentially one of the country’s most significant metals investments in decades. Read here.

Across mining, refining and smelting, the aluminium sector is being shaped as much by policy frameworks and national strategy as by supply and demand. These developments suggest that aluminium’s trajectory is increasingly intertwined with environmental mandates, trade leverage and long-term industrial positioning.

Don't miss out- Buyers are looking for your products on our B2B platform

Responses