您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The aluminium value chain has been shaped by a mix of expanding raw material supply, geopolitical tensions and shifting market signals. While bauxite mining activity has continued to grow across several producing regions, developments further downstream - particularly around the Strait of Hormuz - have raised concerns about supply security for both alumina and primary aluminium. Corporate results from major producers have also highlighted how companies are navigating this evolving landscape.

{alcircleadd}Bauxite sector sees steady expansion and new resource developments

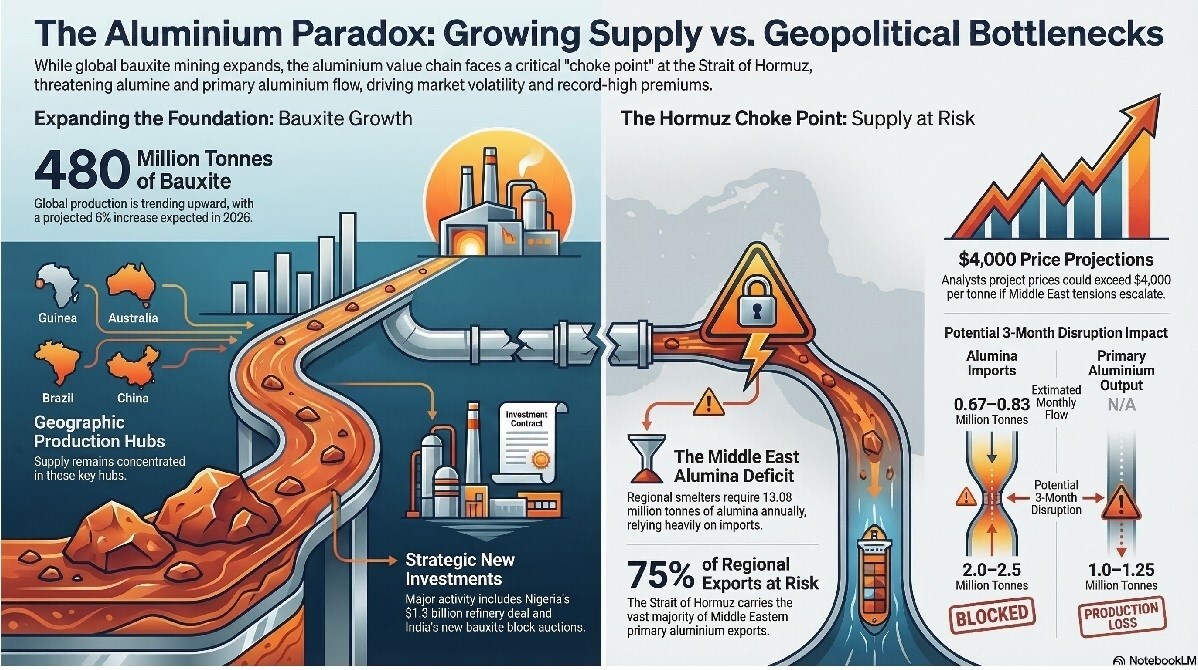

Global bauxite production continued to trend upward in 2025. Estimates from AL Circle place worldwide output at around 475–480 million tonnes, with projections suggesting that production could rise by roughly 6 per cent in 2026.

Supply remains concentrated among a few major producers. Guinea and Australia continue to account for a significant share of global output, while China, Brazil, Indonesia and India also rank among the leading suppliers. Large-scale operations stretching from Weipa in Australia to Paragominas in Brazil remain key pillars of global production. To read more click.

Mining activity during the year reflected this continued momentum. Metro Mining restarted operations at its Bauxite Hills mine in Cape York, North Queensland, after completing maintenance during the wet-season shutdown. Meanwhile, Rio Tinto has been focusing on operational improvements at its Amrun bauxite operations in far north Queensland, where production in 2025 increased by 6 per cent to 62.4 million tonnes. Read more.

India also saw movement on the resource front. In a competitive auction organised by the Government of Odisha, Vedanta Limited secured preferred bidder status for the Karnapodikonda bauxite block.

Despite the generally positive supply picture, import trends in the United States told a different story. US bauxite imports slowed during 2025, after recording relatively steady growth in the previous year. By the third quarter, inbound shipments stood at 403,000 tonnes, down 27 per cent from the 553,000 tonnes recorded in Q3 2024 and 38 per cent lower than Q3 2023 levels. Even so, Jamaica remained the country’s primary supplier of bauxite.

Explore- Most accurate data to drive business decisions with Global Aluminium Industry Outlook 2026 across the value chain

Alumina supply routes draw attention as trade risks emerge

Further along the aluminium value chain, the focus has increasingly shifted toward the movement of alumina and the vulnerabilities associated with global shipping routes.

A key point of concern is the Strait of Hormuz, which plays a crucial role in the flow of raw materials into the Middle East. The region has a combined aluminium production capacity of about 6.92 million tonnes per year, requiring approximately 13.08 million tonnes of alumina annually. Because local production does not meet this demand, smelters in the region rely heavily on imported alumina, much of which travels through this narrow shipping corridor. Read the full story here.

Policy developments have also been emerging elsewhere. China has outlined plans to tighten supervision in sectors such as alumina, copper, coal and chemicals, while simultaneously planning reductions in industries including steel manufacturing and oil refining.

In Europe, environmental concerns have surfaced around refining capacity. The Environmental Trust Ireland (ETI) has indicated that it intends to bring a High Court case concerning the proposed expansion of the Aughinish Alumina refinery in County Limerick. Read more.

At the same time, Nigeria has taken steps to strengthen its mining sector. The country has signed a USD 1.3 billion alumina refinery agreement with the Africa Finance Corporation (AFC). The project falls under the Solid Mineral Development Fund (SMDF), a sovereign investment initiative designed to stimulate private sector growth in mining. The full story is here.

Middle East tensions raise concerns for aluminium supply

Geopolitical developments have added another dimension to the market outlook. Escalating tensions surrounding the US–Israel conflict involving Iran have brought renewed focus to the Strait of Hormuz, one of the world’s most important maritime trade routes.

The passage is critical not only for energy markets but also for aluminium. It carries around 5.14 million tonnes of primary aluminium exports, accounting for roughly 75 per cent of the Middle East’s production. At the same time, 20–21 million barrels of crude oil and petroleum liquids move through the route each day, representing 20 to 30 per cent of global consumption.

A prolonged disruption could therefore have far-reaching consequences. Based on annual flows of 8–10 million tonnes of alumina, roughly 0.67–0.83 million tonnes pass through the route each month. If the strait were to remain closed for three months, around 2.0–2.5 million tonnes of alumina shipments could be affected.

Given that aluminium production typically requires two tonnes of alumina for each tonne of metal, such a disruption could potentially impact 1.0–1.25 million tonnes of primary aluminium output. Read the whole article here.

Market reactions reflect rising supply uncertainty

The possibility of supply disruptions has already begun to influence market expectations. Analysts at ING Group have projected that aluminium prices could move above USD 4,000 per tonne if tensions in the Middle East intensify.

Stock markets have also reacted. In India, Hindalco shares climbed nearly 7 per cent, while NALCO shares rose 18 per cent within eight days, supported by stronger aluminium prices and concerns over supply disruptions in West Asia. Read more.

Meanwhile, production data shows that the US primary aluminium sector continues to face structural challenges. During the first nine months of 2025, domestic production reached 497,000 tonnes, compared with 506,000 tonnes during the same period in 2024, representing a 1.8 per cent year-on-year decline. Click for more.

Supply concerns have also influenced contract negotiations. Rio Tinto increased its aluminium premium offer to Japanese buyers to USD 350 per tonne for April–June shipments, a 79 per cent increase compared with the current quarter.

Producers close the year with mixed financial results

Corporate earnings across the aluminium sector reflected a mixed picture. Press Metal reported strong financial performance in 2025. The company’s fourth-quarter profit reached RM 696 million (USD 178 million), surpassing consensus estimates of RM 600–650 million and marking a 38 per cent increase year-on-year. The figure also represents the company’s highest quarterly profit so far. Read here.

Emirates Global Aluminium (EGA), meanwhile, recorded cast metal sales of 2.83 million tonnes in 2025. Net profit for the year stood at AED 2.12 billion.

Excluding the Guinea Alumina Corporation, the company reported underlying net profit of AED 4.93 billion (USD 1.34 billion), a 16 per cent increase year-on-year. Underlying revenue rose 14 per cent to AED 31.98 billion (USD 8.71 billion), while EBITDA reached AED 9.28 billion (USD 2.53 billion). Full report is here.

Together, these developments underscore how expanding resource supply and growing geopolitical risks are simultaneously shaping the global aluminium market.

Must read: Key industry individuals share their thoughts on the trending topics

Responses