您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

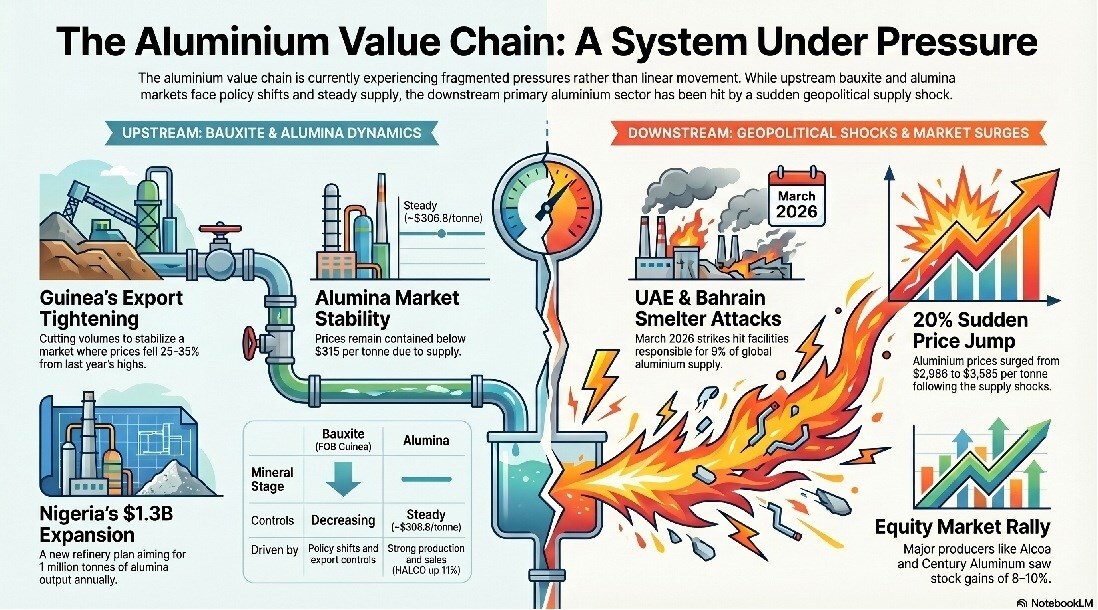

Over the past two weeks, the aluminium value chain has unfolded in fragments rather than a single, linear move. What starts as policy shifts and price pressure in bauxite moves through a well-supplied alumina market, before ending in a sudden supply shock in primary aluminium. Each layer is reacting to a different trigger-but together, they are reshaping the balance across the system.

{alcircleadd}Bauxite: export controls, price signals and new capacity plans

At the upstream end, supply discipline and expansion are moving side by side. Nigeria has stepped forward with plans to build a 1 million tonne alumina refinery, backed by USD 1.3 billion in financing, with expectations of producing 19 million tonnes over 20 years and contributing USD 1.2 billion annually to GDP. The full story is here.

At the same time, Guinea-Conakry is tightening its grip on exports. After shipping 183 million tonnes in 2025-up 25 per cent year-on-year-and targeting 200 million tonnes for 2026, the country is now set to cut volumes from April to stabilise a market where prices have already fallen 25–35 per cent from last year’s highs. Nearly 70 per cent of its exports continue to move to China, keeping demand concentrated even as supply risks grow. Read more.

Pricing trends reflect this tension. FOB Guinea bauxite stood at USD 33–38 per dry metric tonne on March 27, up slightly week-on-week but still down USD 8–11 per dmt since December. Industry views suggest that if exports rise unchecked towards 240 million tonnes, prices could slip further to around USD 50 per tonne, putting additional pressure on producers.

Bauxite supply: structural gaps and emerging players

Beyond immediate policy moves, deeper supply imbalances remain visible. Brazil continues to hold around 1.7 billion tonnes of reserves, yet production has remained unchanged at 30-33 million tonnes for five years, even as exports rose 20 per cent in 2025-highlighting a persistent gap between potential and output. A similar pattern is visible in its rare earth sector, pointing to broader structural constraints. Click here.

Meanwhile, new supply is being lined up to capture opportunity. Canyon Resources is advancing its Minim Martap project in Cameroon, with its first shipment targeted for September, positioning itself within a market still searching for high-grade bauxite.

Alumina: steady supply keeps prices contained

As the story moves downstream, the tone shifts. Alumina continues to reflect a well-supplied market, with prices unable to break past USD 315 per tonne. From USD 321 per tonne in October 2025, prices have eased to around USD 306.8 by the end of Q1 2026, moving within a narrow band despite volatility elsewhere. Click for more.

Operationally, production remains strong. NALCO reported an 11.2 per cent increase in alumina output and a 30.7 per cent rise in sales, supported by higher bauxite handling of over 7.7 million tonnes. Alumina hydrate output stood at 2.3 million tonnes, while calcined alumina rose 11.16 per cent to 2.275 million tonnes, with aluminium production steady at 472,000 tonnes.

Indonesia reflects another layer of imbalance. While alumina output rose from 1.2 million tonnes in 2024 to 1.5 million tonnes in 2025, and bauxite production edged up to 10 million tonnes, the pace of refining and smelting expansion is beginning to outstrip upstream supply, exposing gaps despite large reserves.

Explore- Most accurate data to drive business decisions with 50+ reports across the value chain

Disruptions: conflict begins to redirect flows

Even within a stable alumina market, disruptions have started to shift material flows. Following strikes linked to the US–Israel–Iran tensions, Emirates Global Aluminium has moved to offload alumina cargoes after impacts on its smelting operations near Abu Dhabi.

What began as a disruption quickly escalated into a direct supply shock. Read the full story.

Primary aluminium: attacks, price surge and market reaction

On March 28, 2026, Iranian missile and drone attacks hit major aluminium facilities in the UAE and Bahrain, including Emirates Global Aluminium’s Al Taweelah smelter and Aluminium Bahrain. The incident brought geopolitical risk directly into a region that supplies around 9 per cent of global aluminium, marking a shift in how supply security is being viewed. Read here.

Markets reacted almost immediately. Aluminium prices climbed from USD 2,986 per tonne to USD 3,585 per tonne by March-end, with momentum accelerating through March and reaching USD 3,520 per tonne on March 13. Click here.

Equities followed the same direction. Alcoa Corporation rose as much as 11.8 per cent intraday before closing 8.23 per cent higher at USD 63.22. Press Metal Aluminium Holdings gained 6.3 per cent, while Century Aluminum advanced around 10 per cent, reflecting tightening supply expectations.

Shifting strategies in a tightening market

As prices rise, companies are adjusting course. Vedanta Limited has extended its demerger deadline to June 30, 2026, citing pending regulatory approvals, while continuing to push large-scale investments in Odisha worth INR 1.8 lakh crore and highlighting over 5 lakh jobs created.

At the same time, RUSAL is redirecting shipments from China to Japan and other Asian markets, as geopolitical tensions begin to redraw trade routes and influence regional premiums.

A critical metal under pressure

Across major economies-including the US, EU, UK, Canada and Africa-aluminium continues to gain ground as a critical mineral, tied closely to industrial growth, defence and decarbonisation. In the United States alone, the sector supports around 400,000 jobs and contributes USD 228 billion to the economy. Read more.

Over the past two weeks, however, the bigger takeaway is not just its importance—but how quickly different parts of its value chain can move out of sync, turning a connected system into a series of diverging pressures.

Don't miss out- Buyers are looking for your products on our B2B platform

Responses

_0_0.jpg/500/0)