您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

As aluminium increasingly becomes a strategic raw material for decarbonisation and advanced manufacturing, the focus is no longer limited to primary metal production. From export restrictions and carbon pricing to import duties and circular economy measures, a growing wave of policy interventions is reshaping global aluminium scrap flows. These developments are influencing availability, pricing and competitiveness across aluminium supply chains.

{alcircleadd}Trade scenarios

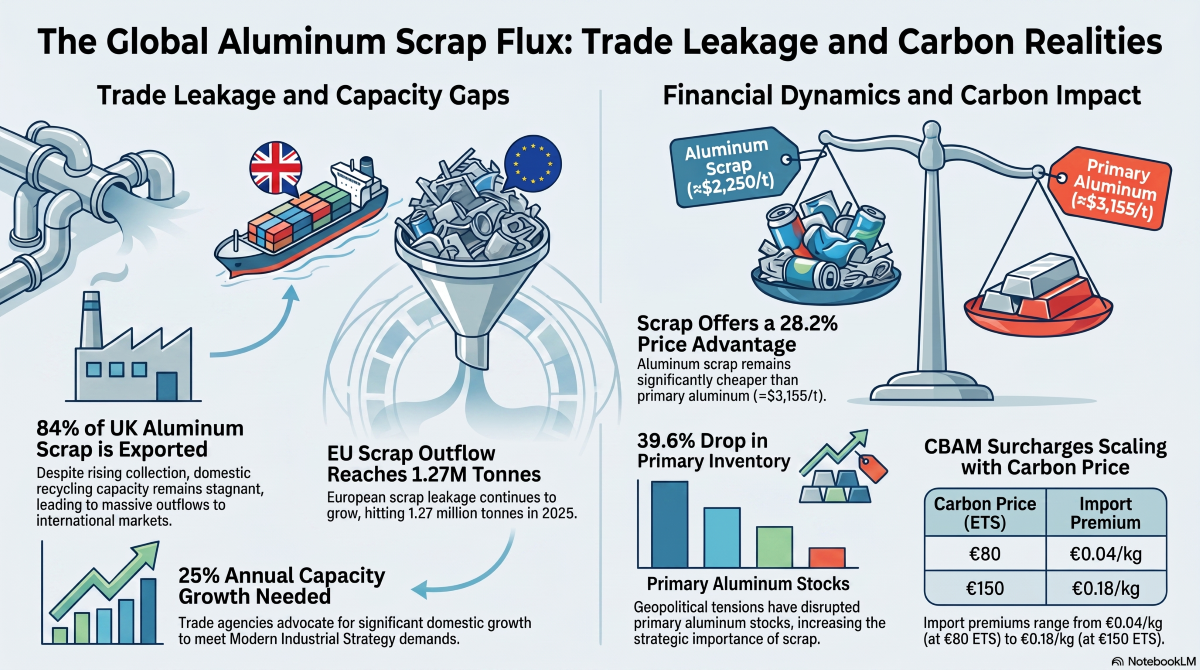

When it comes to scrap leakage, Europe takes the centre stage. While in 2024 the European Union’s aluminium scrap outflow exceeded 1.2 million tonnes, in 2025 it neared 1.3 million tonnes, settling at 1.27 million tonnes.

As industrial analysts warn the administration of stricter measures to safeguard quality aluminium scrap and treat it as a strategic resource, the following nations offer a contrasting export chart:

The United Kingdom’s total aluminium scrap exports reached 623,584 tonnes in 2025, according to Customs data. These volumes have been on the rise since the start of this decade as the collection grows and the domestic recycling capacity remains largely stagnant.

Domestic manufacturing trade agency Make UK has advocated that the country needs a 25 per cent annual growth rate in recycling capacity to meet its Modern Industrial Strategy demands. It acknowledges that around 84 per cent of the UK’s aluminium scrap is still being exported today.

In January-April 2026, the UK’s aluminium scrap exports climbed 9 per cent to 217,611 tonnes from 200,374 tonnes in the year prior.

Primary markets: UK’s largest markets with import potential are:

_0_0.png)

Germany exported 311,491 tonnes of aluminium scrap to the global market in Q1 2026, up marginally by 0.5 per cent from 310,057 tonnes in Q1 2025. The increase was more pronounced on a quarterly basis, with exports rising 8.8 per cent from 286,285 tonnes in Q4 2025.

Primary markets: While its largest market, Italy, reported an import decline, sourcing 46,941 tonnes, the following markets held strong with shipment volume hikes.

The sourcing surge by these countries is expected to open new business avenues.

Key takeaways:

Considering an intra-continent vs inter-continent trade scenario, the calculation will be like this:

Emissions Trading System (ETS) cost calculating formula: Total Cost = Fuel Consumed × CO₂ Factor × Phase-in × Trade Share × EUA Price

Carbon Border Adjustment Mechanism (CBAM) calculating formula: Carbon Cost (per tonne) = Scope 1 Intensity (t CO₂e / t metal) x Current EU ETS Price

Converted to EUR per kilogramme: EUR per kilogram impact = (Intensity × ETS price) ÷ 1,000

The ETS formula can change a lot depending on the phase-in factor and trade share, while CBAM is more straightforward because it charges on the carbon intensity of the imported product itself.

AS CBAM also uses the EU ETS price, under a conservative EU ETS scenario of EUR 80, CBAM surcharges increase extrusion import costs by EUR 0.04-0.10 per kilogramme.

In contrast, under an aggressive EUR 150 scenario, this premium widens to EUR 0.075-0.18 per kilogramme, and could climb even higher if default values are applied.

Looking at the other side of the coin, primary aluminium price as per the London Metal Exchange (LME) benchmark hovers around USD 3,150 to USD 3,160 per tonne, while aluminium scrap is priced around USD 2,200 to USD 2,300 per tonne, 28.22 per cent less.

In terms of availability, while aluminium scrap gains greater attention as a strategic material, primary aluminium inventory, usually stocked sufficiently, has recently sustained disruptions owing to geopolitical tensions in the Middle East.

Consequently, its demand has shot up considerably, from tonnes at the close of February to tonnes on July 9, down 39.6 per cent over the months.

Delve deeper into the recycled aluminium and secondary aluminium market with our World Recycled ALuminium Market Analysis Industry forecast to 2032

Policy measures

A forecast of 2026 trade policies included the imposition of CBAM, or the likelihood of inclusion of aluminium scrap into the US tariff regime. Japan’s circular economy and the United Arab Emirates’ export fee policy were worth a deep dive into.

In reality, which regions have come under the limelight?

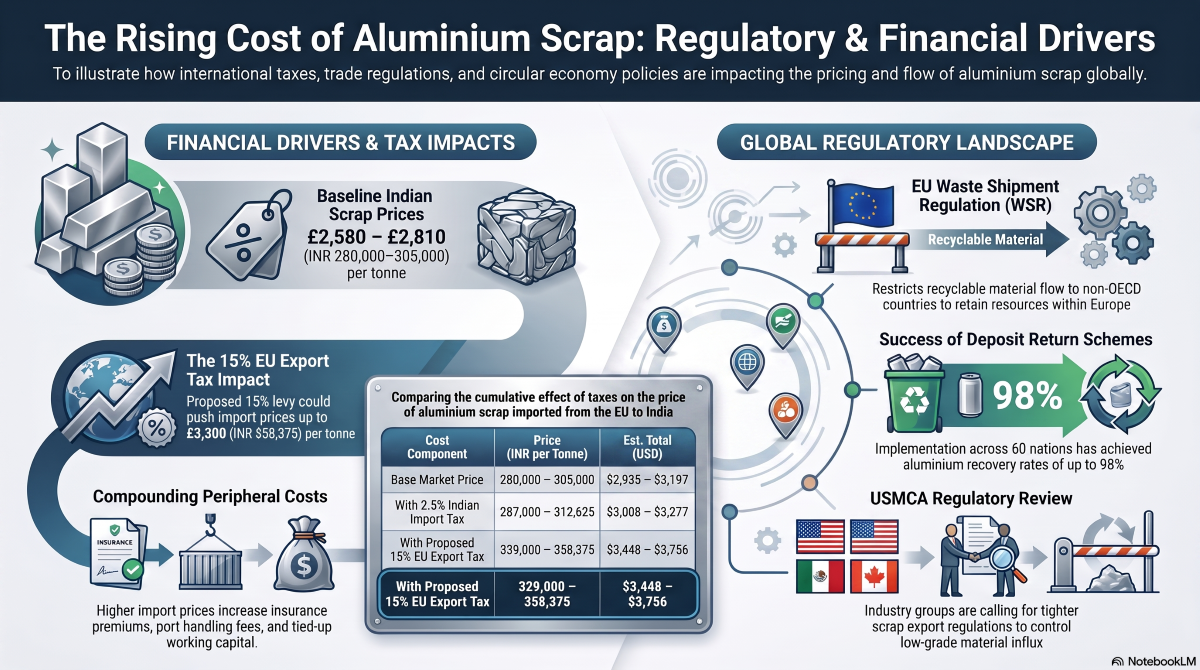

The European Commission has proposed a 15 per cent duty on aluminium scrap exports as part of a broader effort to strengthen the EU's circular economy and secure more recycled metal for domestic industry. The proposal aims to address concerns that large volumes of valuable scrap are leaving Europe while demand for low-carbon secondary aluminium continues to rise. Industry groups have largely welcomed the move, arguing that retaining more scrap within the region could support recycling capacity, reduce import dependence and improve the competitiveness of Europe's aluminium value chain, although the measure will still require approval through the EU legislative process.

The American Aluminum Association has urged the US administration to strengthen the nation’s aluminium supply chain by expanding both primary and secondary production. The association noted that although US primary aluminium production has fallen about 80 per cent since the 1980s, recycling now accounts for nearly 85 per cent of domestic aluminium output, supported by more than USD 11 billion in industry investment over the past decade.

The association pushed recycling boosts through stronger scrap retention policies and, for primary aluminium, recommended expanding access to affordable electricity, streamlining project approvals, supporting critical mineral production, and maintaining targeted trade measures against unfair imports. It estimates global aluminium demand will rise by around 80 per cent by 2050 and a stronger domestic supply chain will be critical to supporting the US manufacturing footprint.

India's aluminium industry remains divided over the future of aluminium scrap imports, with primary producers advocating tighter controls while secondary manufacturers push for duty relief. The Aluminium Association of India (AAI), representing primary aluminium producers, warned that the growing inflow of compromised quality scrap could undermine planned investments exceeding INR 3 trillion (USD 31.5 billion).

India currently imposes a 7.5 per cent Basic Customs Duty (BCD) on primary aluminium and 2.5 per cent on aluminium scrap.

However, according to the Material Recycling Association of India (MRAI), import duty on aluminium scrap should eventually be removed, since India largely imports processed scrap rather than unprocessed waste. The Aluminium Secondary Manufacturers Association (ASMA), hosting nearly 3,500 MSMEs, backed the opinion, as lower import costs would ease raw material expenses, which account for up to 80 per cent of downstream production costs.

AAI has further urged for immediate implementation of the Bureau of Indian Standards (BIS) norms for aluminium scrap, warning that India risks receiving poor-quality scrap. The association has proposed retaining the 2.5 per cent BCD until BIS standards and grade-wise HSN codes are notified, after which it recommends raising duties on Grade 3 to Grade 7 scrap to 7.5 per cent.

AAI argues that stricter quality standards are essential to protect manufacturing competitiveness, product quality and consumer safety. The move comes as India's secondary aluminium industry has expanded from 0.85 million tonnes in FY2015-16 to nearly 2.2 million tonnes in FY2025-26, accounting for around 35 per cent of domestic aluminium consumption. However, domestic end-of-life scrap generation currently satisfies only 15-20 per cent of industry requirements, leaving 80-85 per cent dependent on imports.

Aluminium scrap imports reached 2 million tonnes, resulting in a foreign exchange outgo of INR 402.03 billion (USD 4.22 billion). AAI also highlighted that recycled aluminium is critical to India's Net Zero 2070 roadmap.

According to NITI Aayog, recycled aluminium could account for around 45 per cent of India's aluminium demand by 2028, while the country's primary aluminium capacity is expected to nearly double to 9 million tonnes per annum by FY33 through investments planned by Vedanta, Hindalco and NALCO.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

Key takeaways:

At present, scrap prices in India from the aluminium tense to aluminium extrusion category range between INR 280,000 (USD 2,934.82) per tonne and INR 305,000 (USD 3,196.85) per tonne.

Additional charges to look out for include the 2.5 per cent import tax imposed on aluminium scrap by the Government of India and the 15 per cent export tax proposed by the European Commission to slow scrap leakage.

In case of the Indian import tax, if retained, would continue to add around INR 7,000 (USD 73.37) to INR 7,625 (USD 79.92) per tonne, with the price totalling around INR 28,7000 (USD 3,008.19) to INR 312,625 (USD 3,276.78) per tonne.

As of the proposed export tax, a 15 per cent duty would include another surcharge of INR 42,000 (USD 440.22) to INR 45,750 (USD 479.53) per tonne.

This would raise the pricing bar around INR 329,000 (USD 3,448.41) to INR 358,375 (USD 3,756.3) per tonne of aluminium scrap imported into India from the EU.

The figure would continue to gain a larger size as the other surcharges of Goods and Services Tax (GST) reduction on metal scrap from 18 per cent to 5 per cent, exemption of imported non-ferrous scrap from proposed Extended Producer Responsibility (EPR) requirements, and the removal of the mandatory Pre-Shipment Inspection Certification (PSIC) system.

Upcoming policies to look out for include a review of the United States-Mexico-Canada Agreement (USMCA), with industry groups seeking to include aluminium scrap under tighter export regulations amid concerns over rising shipments of low-grade material.

The EU’s Waste Shipment Regulation (WSR), due to take effect in September, will restrict recyclable waste exports, including aluminium scrap, to non-OECD countries.

Meanwhile, existing EU policies continue to strengthen circularity. The Waste Framework Directive promotes resource efficiency and a circular economy, while the Packaging and Packaging Waste Regulation (PPWR) mandates recyclable packaging and Deposit Return Schemes (DRS).

The Critical Raw Materials Act (CRMA) supports domestic supply chains and recycling investment. New vehicle circularity rules aim to improve aluminium recovery from end-of-life vehicles.

European Aluminium has also urged the EU to close the CBAM recycled aluminium loophole by recognising post-consumer scrap and adopting a single default carbon value for unwrought aluminium.

Potential peripheral impacts that industry stakeholders might need to consider include freight and shipping charges, insurance premiums, port handling and terminal charges, warehousing, storage, and demurrage fees and financing or working-capital costs, amongst others.

These are the most common ripple-effect costs because a higher import price usually raises the landed cost, slows clearance, and increases the amount of cash tied up in the shipment.

Responses