您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

_0_0.jpg)

The image used in this article is generated with an AI tool and does not depict any real-time moment

{alcircleadd}As aluminium producers place greater emphasis on recycled metal, scrap has become an increasingly important part of the wider aluminium value chain. Against this backdrop, Germany entered 2026 with a shift in its export picture, as aluminium scrap shipments moved higher after declining on an annual basis in 2025.

Germany exported 311,491 tonnes of aluminium scrap to the global market in Q1 2026, up marginally by 0.5 per cent from 310,057 tonnes in Q1 2025. The increase was more pronounced on a quarterly basis, with exports rising 8.8 per cent from 286,285 tonnes in Q4 2025.

The change in direction came at an interesting time for Germany’s aluminium industry. Recycled aluminium production weakened, semi-finished output declined and demand from automotive, construction and mechanical engineering remained subdued. Meanwhile, stronger competition for European scrap was creating opportunities beyond the domestic market.

So, where did Germany’s aluminium scrap go, and what pushed shipments higher at the start of 2026?

Where did Germany’s aluminium scrap go in Q1 2026?

Italy remained Germany’s largest aluminium scrap destination in Q1 2026, although Austria moved closer to the top position following a strong increase in shipments.

Italy imported 46,941 tonnes of German aluminium scrap, down 2.3 per cent year-on-year from 48,034 tonnes in Q1 2025 and 0.7 per cent quarter-on-quarter from 47,295 tonnes in Q4 2025.

Austria, meanwhile, recorded strong growth. Imports rose 13.2 per cent year-on-year to 43,838 tonnes from 38,711 tonnes and surged 23.3 per cent quarter-on-quarter from 35,553 tonnes. This narrowed the gap with Italy to just over 3,000 tonnes.

The Netherlands followed with 31,438 tonnes, marking an 8.5 per cent year-on-year decline from 34,373 tonnes but a 9.8 per cent quarterly increase from 28,639 tonnes.

Poland imported 22,859 tonnes, down sharply by 25.6 per cent year-on-year from 30,743 tonnes. However, shipments recovered 3.5 per cent from 22,080 tonnes in Q4 2025.

France recorded the strongest annual growth among these major destinations. Imports jumped 41.2 per cent year-on-year to 20,026 tonnes from 14,180 tonnes and increased 8.4 per cent quarter-on-quarter from 18,479 tonnes.

The mixed destination pattern shows that the overall increase was not driven by uniform growth across Germany’s major markets. To understand the broader shift, the trade figures need to be viewed alongside conditions at home. Delve deeper into the recycled aluminium and secondary aluminium market with our World Recycled ALuminium Market Analysis Industry forecast to 2032

What pushed German scrap exports higher in Q1 2026?

Weak domestic demand limits absorption at home

Germany’s domestic aluminium market remained subdued in Q1 2026. Recycled aluminium production fell by around 3 per cent year-on-year to 684,564 tonnes, while semi-finished aluminium output declined by 1 per cent to 568,688 tonnes.

Demand from automotive, construction and mechanical engineering also remained weak. With domestic consumption under pressure, exporters had greater incentive to place available scrap in foreign markets.

The weakness extended further into the downstream chain. Extruded product output declined by 4 per cent, indicating pressure beyond the recycling segment and contributing to instability in scrap collection and trade flows.

The broader recycling figures showed where the pressure was concentrated. Total recycling volumes fell by 3 per cent to 684,564 tonnes. Refiners managed a modest 2 per cent increase to 128,639 tonnes, but this was outweighed by a 4 per cent decline in remelter output to 555,925 tonnes, dragging down the overall segment.

The wider manufacturing environment remained equally subdued. A recent industry survey found that 66 per cent of companies rated their current order books as “poor” or “very poor”, while 71 per cent reported low capacity utilisation. Another 57 per cent did not expect business conditions to improve before the end of 2026.

Longer-term confidence was also weak. Some 76 per cent of surveyed firms considered it currently improbable or impossible for Germany to achieve its 2045 climate neutrality targets while simultaneously maintaining industrial production within the country.

Taken together, weaker consumption, lower output across key parts of the aluminium chain and subdued industrial confidence reduced the strength of Germany’s domestic market. But conditions at home were only one part of the export shift. Delve deeper into the recycled aluminium and secondary aluminium market with our World Recycled ALuminium Market Analysis Industry forecast to 2032

Stronger foreign demand offers German scrap another outlet

Overseas buyers continued to compete for European scrap, particularly as Asia’s recycled aluminium demand expanded. EU aluminium scrap exports reached a record 1.27 million tonnes in 2025, nearly 50 per cent above 2019 levels, with India and China among the main destinations.

Uneven tariffs and trade measures also widened differences between regional markets, directing material towards destinations offering better returns. The scale of these outward flows prompted the EU to begin preparing measures to curb scrap leakage amid concerns over material availability within Europe.

For Germany, this creates a difficult balance. As many as 85 per cent of companies report a shortage of aluminium scrap, even as overseas markets compete for the same raw material. The situation adds pressure to a recycling chain that depends on sufficient feedstock for resource-efficient and competitive production.

That tension becomes more significant when the latest increase is viewed against Germany’s longer trade history.

Read all the latest developments in Europe’s aluminium recycling industry

The Q1 rise follows an uneven export cycle

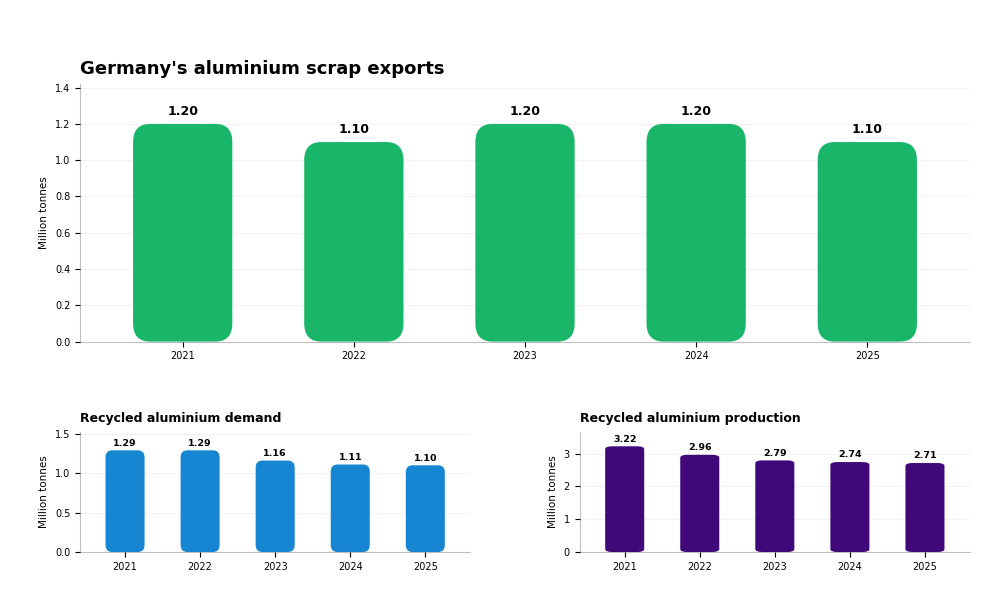

Germany’s aluminium scrap exports have moved through repeated phases of decline and recovery. After falling 8.2 per cent in 2022, shipments recovered in 2023 and 2024 before declining 4.3 per cent to 1,162,477 tonnes in 2025. The direction shifted again in Q1 2026, when exports rose on both a year-on-year and quarter-on-quarter basis.

Changes among major destinations show a similarly uneven pattern.

Italy remained the largest market in 2025, importing 189,523 tonnes, up 2.5 per cent after declines of 8 per cent in 2024, 1.4 per cent in 2023 and 3.8 per cent in 2022.

Austria imported 144,333 tonnes in 2025, down 7.5 per cent after a 6 per cent increase in 2024. That recovery had followed declines of 8.7 per cent in 2023 and 7.3 per cent in 2022.

The Netherlands recorded an 11.8 per cent fall to 118,317 tonnes in 2025, reversing a 4.1 per cent increase in 2024. Imports had previously risen 6.7 per cent in 2023 after falling 13.2 per cent in 2022.

Poland’s imports declined 6.4 per cent to 110,980 tonnes in 2025 after gains of 5.1 per cent in 2024 and 25.5 per cent in 2023, which followed a 14 per cent decline in 2022.

India followed a different trajectory. Imports of German aluminium scrap rose 8.3 per cent to 68,387 tonnes in 2025, extending increases of 19.8 per cent in 2024 and 10.4 per cent in 2023 after an 18.9 per cent decline in 2022.

These movements show how changes in demand across individual destinations have repeatedly reshaped Germany’s export market. But the trade story also needs to be considered alongside the role scrap plays within the recycling chain.

Why scrap availability matters to Germany’s recycling chain

Aluminium scrap is not directly used as a finished material. It is the primary feedstock for recycled aluminium production and must pass through several stages before returning to manufacturing.

Scrap generated during production or recovered from end-of-life products such as cans, vehicles, cables and building materials is first collected and sorted by type, alloy and quality. Contaminants including coatings, plastics and other metals are then removed.

The prepared material is remelted and refined, with its chemical composition adjusted where necessary. It can then be cast into ingots, billets or other usable forms for manufacturing new aluminium products.

This process makes access to suitable feedstock central to the recycling economy. Its importance becomes clearer when viewed against Germany’s longer production trend.

Explore the position of aluminium at the intersection of sustainability and strategy in Sustainability & Recycling: Aluminium's Dual Commitment

Recycled aluminium production loses momentum

The Q1 2026 decline was not an isolated development. Germany’s recycled aluminium production has been losing ground for several years.

Annual output stood at 3.22 million tonnes in 2021 before falling 8.1 per cent to 2.96 million tonnes in 2022. Production declined another 5.7 per cent to 2.79 million tonnes in 2023, then eased to 2.74 million tonnes in 2024 and 2.71 million tonnes in 2025.

Overall, Germany’s recycled aluminium output fell by approximately 15.8 per cent between 2021 and 2025. Based on the production data, around 2.8–3.56 million tonnes of scarp is processed during 2021–2025.

Demand followed a similar downward direction.

Falling demand adds another layer to the export story

Germany’s recycled aluminium demand remained stable at 1.29 million tonnes in both 2021 and 2022 before falling sharply by 10.1 per cent to 1.16 million tonnes in 2023.

The decline continued to 1.11 million tonnes in 2024, while 2025 demand is estimated at 1.10 million tonnes. Overall, demand fell by approximately 14.7 per cent between 2021 and 2025, equivalent to a reduction of 0.19 million tonnes.

The longer-term demand contraction adds important context to Germany’s Q1 2026 export rise. While the domestic recycling market has been losing momentum, external buyers have continued to seek European material.

Germany is therefore facing a difficult balance. A subdued home market can encourage scrap to move towards more attractive destinations, while the recycling industry still requires sufficient suitable feedstock to remain competitive. The Q1 2026 increase brings that underlying tension more clearly into view.

Responses