您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

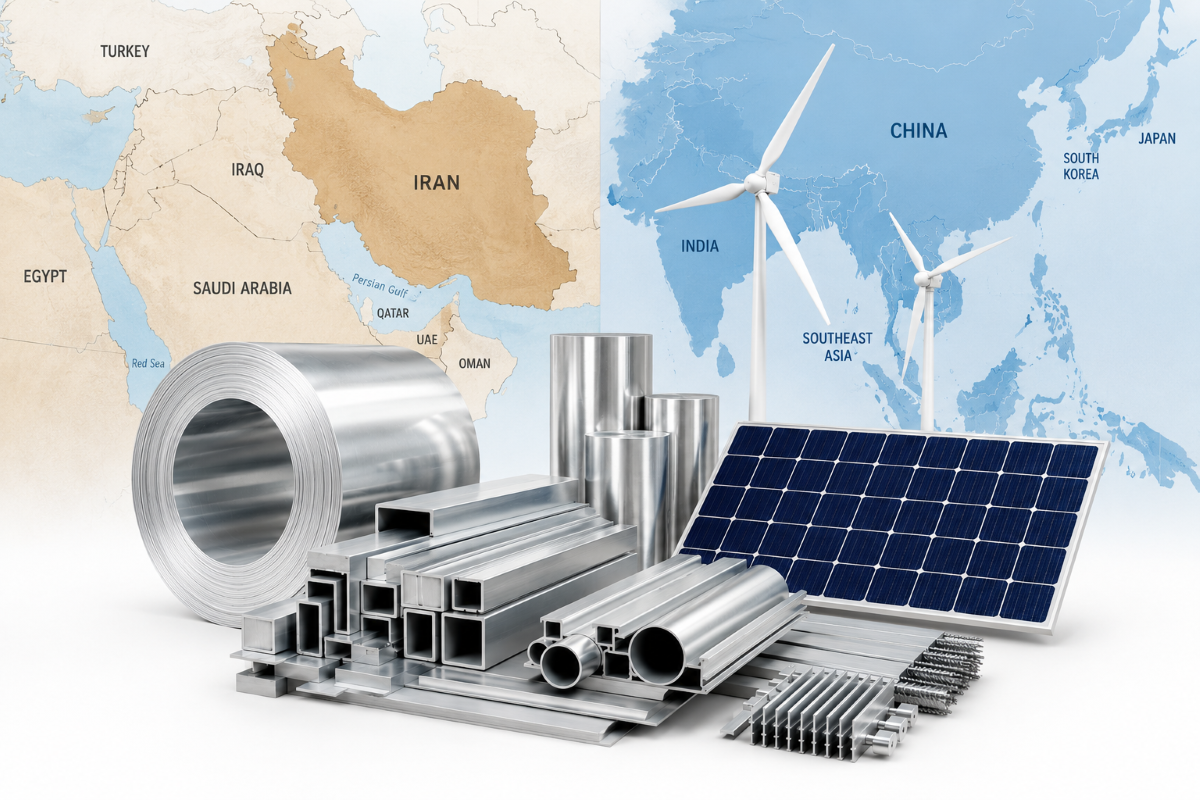

As the ongoing Middle East conflict disrupts aluminium and nickel supply chains, a question mark looms over Asia’s renewable energy ambitions, threatening to raise costs for solar panels, wind turbines and grid infrastructure across the region.

{alcircleadd}Countries including Indonesia, Vietnam and the Philippines have accelerated rooftop solar and renewable energy deployment in recent years, largely in response to persistently high fossil fuel prices. But the growing instability around the Strait of Hormuz is now casting a shadow of uncertainty over the supply of critical industrial metals required for the energy transition.

Discover: The Gulf aluminium market risks, China impact, alumina supply, carbon costs, and logistics disruptions shaping pricing and trade in Gulf Disruption Roadmap

The Iranian missile attacks on the Emirates Global Aluminium (EGA) and Aluminium Bahrain (Alba) facilities have crippled up to an estimated 3 to 3.2 million tonnes of combined annual capacity. Combined with the 40 per cent production shutdown (estimated 259,200 tonnes) at the integrated aluminium complex Qatalum, 3 to 4 per cent of the global supply has been cut short.

The Middle East remains one of the most exposed regions in the aluminium trade, accounting for about 9 per cent of global aluminium production and almost 20 per cent of supply outside China.

While Chinese producers are attempting to increase output, the country’s 45 million tonne production cap continues to restrict any large-scale expansion.

The London Metal Exchange (LME) aluminium prices have climbed over 13 per cent since the inception of the conflict on February 28 and are up about 19 per cent year-to-date (YTD), according to Reuters. The three-month benchmark aluminium price stood at USD 3,602 per tonne on the close of the Tuesday session.

ANZ Bank highlighted that 75 per cent of the Middle East’s aluminium smelting capacity depends on imported alumina and bauxite moving through the Strait of Hormuz. Any prolonged restriction in shipping routes could intensify production curtailments across Gulf smelters.

The implications are significant for renewable energy supply chains. Aluminium plays a critical role in solar photovoltaic modules, wind turbines, transmission systems and power infrastructure because of its conductivity, lightweight properties and recyclability.

According to Will Symons, Head of Deloitte Asia-Pacific’s sustainability practice, existing renewable power assets are largely unaffected, so the extent of disruption is uncertain. However, he warned that tightening aluminium availability would inevitably raise costs for new renewable projects.

“Disruptions to Gulf aluminium exports and smelting operations are tightening global supply and increasing manufacturing costs across clean energy technologies,” Symons said.

To look for buying or selling leads of aluminium solar extrusion products, visit our B2B marketplace.

Nickel at a critical juncture

Markets of nickel, a crucial lithium-ion battery component, are also beginning to feel the heat. Disruptions to sulphur supplies moving through the Strait of Hormuz are affecting nickel production, with the Middle East accounting for nearly a quarter of global sulphur output used in nickel extraction.

Nickel prices rose to USD 18,933 per tonne on Tuesday, compared with USD 17,238 per tonne when the conflict began in late February.

“While the direct impact of the Middle East conflict on nickel is less immediate than on aluminium, the structural risks to the broader clean energy transition are deeply interconnected,” said Harjeet Singh, Founding Director of Satat Sampada Climate Foundation.

Singh stressed that long-term clean energy goals must increasingly focus on supply chain diversification, localised processing and stronger recycling infrastructure for metals such as aluminium and nickel.

Projecting a grim future for aluminium

Wood Mackenzie has projected that the conflict may wipe out between 3 million and 3.5 million tonnes of global aluminium output in 2026 from a market that produced just under 74 million tonnes in 2025.

ANZ forecasts that aluminium supply losses may widen the market deficit to 2.7 million tonnes this year and more than 1.1 million tonnes in 2027.

“If the Strait of Hormuz reopens, prices may briefly dip, but renewed restocking by manufacturers should limit any significant downside. We expect the aluminium price to remain skewed to the upside, trading above USD 3,400 per tonne this year,” ANZ stated.

Symons observed, “These cost increases may become structural if manufacturers permanently shift sourcing to higher cost suppliers in China, Australia or Canada.” He added that sustained price increases and prolonged supply constraints could slow renewable energy deployment and complicate grid modernisation plans.

Symons also noted that rising aluminium prices are expected to affect solar mounting structures, rooftop installations, battery storage systems, transmission infrastructure and wind energy equipment.

In a May 11 report, Oxford Economics Lead Economist Stephen Hare described the Iran conflict as a “systemic, multichannel supply shock to global metals markets.”

The report identified aluminium as the metal facing the most severe impact because of the global market’s heavy reliance on Gulf production. Around half of the region’s smelting capacity is currently offline, equivalent to roughly 4-5 per cent of global supply.

“Given long restart timelines and power constraints, this points to a structural shock,” Hare noted.

Singh, along similar lines, commented, “What the crisis in the Middle East starkly highlights is the extreme vulnerability of our highly centralised mineral supply chain. We cannot achieve a resilient, just energy transition if our clean technology foundations remain tied to volatile geopolitical choke points.”

Explore the position of aluminium at the intersection of sustainability and strategy in Sustainability & Recycling: Aluminium's Dual Commitment

Responses