您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

EXECUTIVE SUMMARY:

{alcircleadd}For half a century, the global aluminium value chain operated on a predictable, linear model. If you needed a cheap die-casting, you bought ADC12. If you needed electrical wiring, you bought 1350. If you needed an aerospace frame, you bought 7075 and mechanically riveted it together.

Today, those traditional metallurgical windows are functionally dead.

The extreme lightweighting demands of EVs, the explosive thermal and electrical loads of AI data centres, and the incoming financial penalties of the CBAM have completely rewritten the rules of alloy selection. If a plant manager attempts to force a legacy alloy into a next-generation application, the result is catastrophic: giga-castings tear in the mould, electrical terminations creep and catch fire, and high-carbon primary metal wipes out the profit margin at the border.

To survive, procurement officers and plant managers need a new map. Here is the definitive AL Circle Master Matrix, detailing exactly how the industry's most critical alloy families are being upgraded, doped, and engineered for the next industrial era.

The global aluminium casting usage is expected to reach 24.2 million tonnes in 2026. To know about the future market trends, prebook our upcoming report “Global Aluminium Casting Market 2026-2032

The master alloy comparison matrix

_0_0.png) The image used in this article is generated with an AI tool and does not depict any real-time moment

The image used in this article is generated with an AI tool and does not depict any real-time moment

The foundry revolution: RidgeAlloy, rheocasting, and active cooling

For decades, ADC12 (Al-Si-Cu) was the undisputed king of high-pressure die casting (HPDC). However, the EV "Giga-casting" revolution, pioneered by single-shot underbodies replacing hundreds of stamped parts, has exposed ADC12's fatal structural flaws. Traditional HPDC alloys require high iron content to prevent the metal from soldering to the steel die, but that iron creates brittle, needle-like intermetallic phases that warp and crack catastrophically during T6 heat treatment. Furthermore, turbulent metal injection at velocities exceeding 50 m/s inevitably folds air and surface oxides into the casting, generating destructive oxide bifilms.

The chemistry upgrade: RidgeAlloy - As foundries shift toward circular economies, they must learn to process post-consumer scrap without relying on expensive primary metal dilution. The breakthrough is ridgealloy, engineered by the U.S. Department of Energy’s Oak Ridge National Laboratory.

Utilising high-throughput computing, metallurgists developed a novel Al-Mg-Si-Fe-Mn composition that can absorb a massive 1.5 wt% iron and 1.5 wt% silicon simultaneously without losing ductility.

The physical upgrade: Semi-solid metal (SSM) rheocasting To eliminate oxide bifilms, advanced foundries are abandoning turbulent liquid injection entirely in favour of SSM Rheocasting.

This process manipulates the aluminium alloy as a semi-solid slurry. By carefully controlling the cooling rate of the melt prior to injection, the aluminium achieves a partially solidified state characterised by a non-dendritic, highly globular microstructure.

Integrated thermal management: The CoolCast imperative Active liquid cooling is essential for next-generation EV drivetrains. Casting lightweight, hollow aluminium tubes directly into a structural HPDC component was historically impossible because extreme injection pressures (up to 1,200 bar) instantly crushed the tubes.

This bottleneck is resolved via ZLeak Tube technology, developed under the CoolCast research project.

The electrification & AI backbone: Zirconium, CCA, and busbars

Driven by the explosive price of copper and the sheer physical limits of modern electrical infrastructure, the world is frantically substituting copper with aluminium. However, standard 1350 electrical-grade aluminium suffers from severe "creep" (permanent deformation under sustained mechanical and thermal stress). This causes mechanical connection joints to loosen over time, forming highly resistive oxide layers (Al₂O₃) that trigger catastrophic electrical fires.

The grid upgrade: Zirconium-doped TAL: To build offshore wind grids and high-voltage transmission lines, the industry is pivoting to Thermal Resistant Aluminium Alloys (TAL). By doping the melt with 0.02 to 0.05 per cent zirconium (Zr) and a trace amount of boron (B), metallurgists permanently alter the alloy's performance boundaries.

The EV motor upgrade: The 1370 CCA core: Inside the EV traction motor, heavy copper hairpin windings are being replaced by copper-clad aluminium (CCA). This bimetallic wire utilises a soft 1370 aluminium core co-extruded inside a highly conductive copper cladding.

The AI data centre upgrade: 6xxx Series Busbars Next-generation AI server racks, packed with advanced GPUs, consume up to 100 kW of power. Delivering this immense power via traditional copper cables is impossible; the sheer weight of the copper cables exceeds the structural load-bearing limits of raised data centre floors.

The scrap & extrusion mandate: ShAPE and nanocomposites

Downstream manufacturers face immense pressure from OEMs to transition from high-carbon primary metal to 100 per cent recycled secondary scrap. However, processing post-consumer scrap via traditional extrusion is a metallurgical nightmare: tramp iron impurities cause extruded profiles to snap and automotive sheets to fracture during stamping.

The process upgrade: ShAPE technology Pacific Northwest National Laboratory's Shear Assisted Processing and Extrusion (ShAPE) fundamentally disrupts the extrusion lifecycle.

The material upgrade: Metal matrix nanocomposites (MMNCs) - By uniformly dispersing nano-sized ceramic particles like silicon carbide (SiC) or titanium carbonitride (TiCN) into the secondary aluminium melt, metallurgists are engineering properties beyond the limits of monolithic alloys.

The aerospace apex: The scandium upgrade

The highest-margin sectors in the world, aerospace and defence, have hit a 50-year metallurgical plateau. The 7000 Series (Al-Zn-Mg-Cu) represents the absolute pinnacle of commercial strength, but these alloys suffer from a catastrophic flaw: they are notoriously unweldable. The intense heat of a welding arc destroys the carefully engineered microstructure in the Heat Affected Zone (HAZ), leading to severe hot cracking. This historically forced aerospace OEMs to rely on millions of heavy, expensive rivets.

The next-gen upgrade: Scandium microalloying - Adding trace amounts of Scandium (typically 0.1 to 0.5 wt%) to the melt represents the most powerful microalloying strategy in modern metallurgy.

Expanding the scandium effect across alloy series:

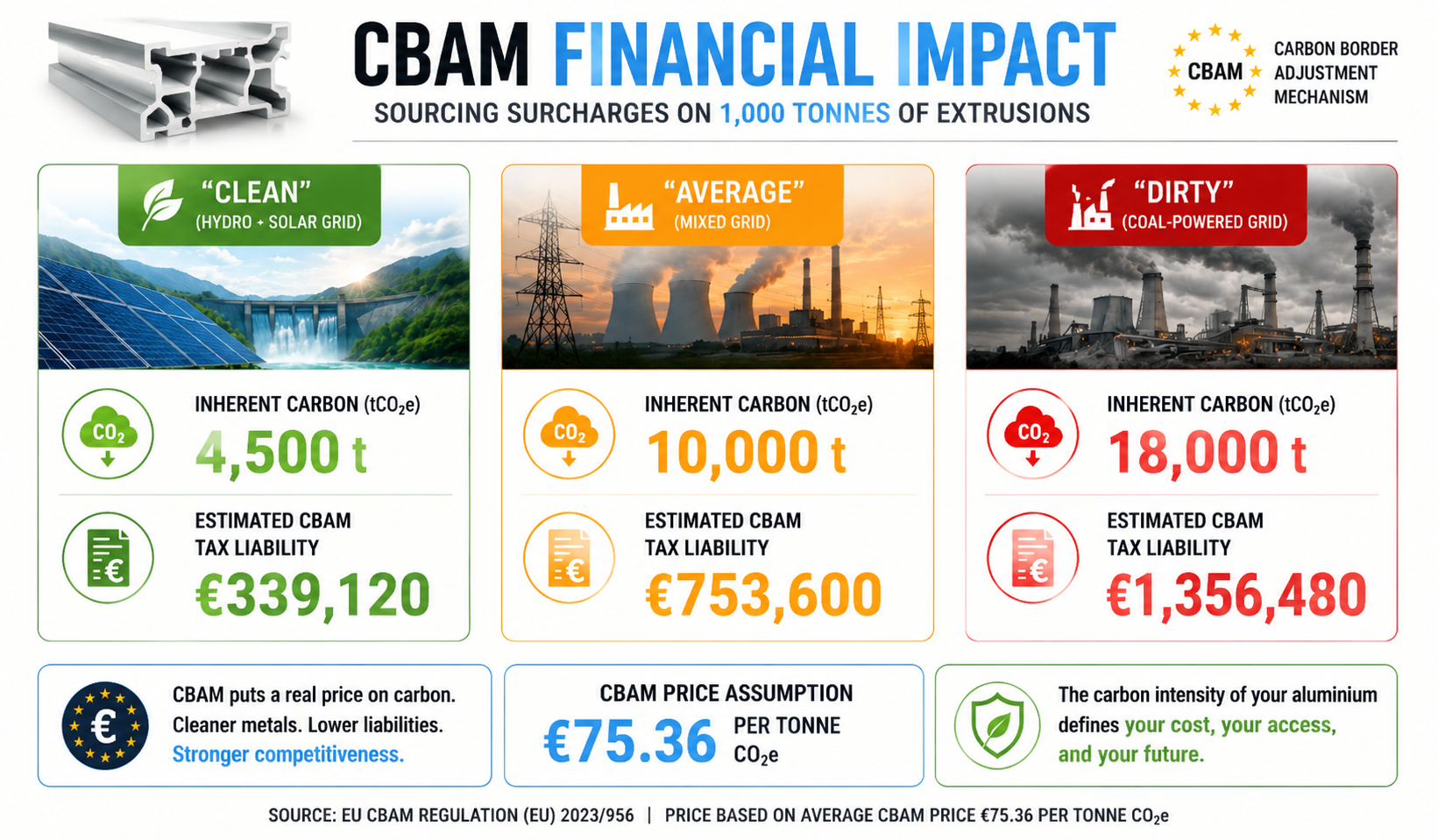

The fifth dimension: Carbon as a physical property (CBAM)

The era of purchasing aluminium based solely on the London Metal Exchange (LME) cash price and standard regional premiums is over. Value and margin are now dictated by the carbon premium.

Under the CBAM, the carbon footprint of imported metal is legally treated as a physical property. High-carbon primary aluminium faces crippling border taxes. Conversely, secondary aluminium derived from post-consumer scrap carries a zero upstream carbon burden.

The carbon algebra: Equations 57 and 58 - To enforce this carbon tariff, the European Commission has codified a strict mathematical framework.

The financial impact scenario - By incorporating localised grid emission factors into the default calculation, carbon-intensive regions are heavily penalised. For example, the national grid factor applied to Chinese industrial production is rated at a massive `1 tCO2e/MWh-approximately 2.7 times higher than the European Union grid average. When combined with the confirmed initial CBAM certificate price of €75.36 per tonne, the financial impact on a 1,000-tonne shipment of extrusions is stark, potentially leading to massive additional costs for exporters.

The image used in this article is generated with an AI tool and does not depict any real-time moment

The image used in this article is generated with an AI tool and does not depict any real-time moment

The numbers are inescapable. As pricing agencies like Fastmarkets embed CBAM costs directly into billet premiums, sourcing cheap, coal-fired primary metal triggers a carbon tax bill exceeding EUR 1.35 million (USD 1.54 million) on a minor shipment, completely wiping out processing margins.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

The strategic conclusion

The aluminium industry has transitioned into a highly complex, deep-tech area. The operators who continue to view aluminium as a simple commodity will be crushed by energy volatility, carbon tariffs, and technological obsolescence.

The future belongs to the operators who master the kinetics of zirconium, the precipitation of scandium, the impurity tolerance of RidgeAlloy, and the zero-carbon footprint of secondary scrap. By connecting the upstream chemistry directly to the downstream manufacturing process, advanced casters, extruders, and procurement officers can secure the highest-margin contracts of the next decade and insulate themselves from the commodity death spiral.

Note: This is exclusive coverage by AL Circle and may not be reproduced, republished or shared without prior permission.

Disclaimer: The opinions, information, claims, references, and images presented here are those of the author alone and AL Circle holds no responsibility.

Responses