您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

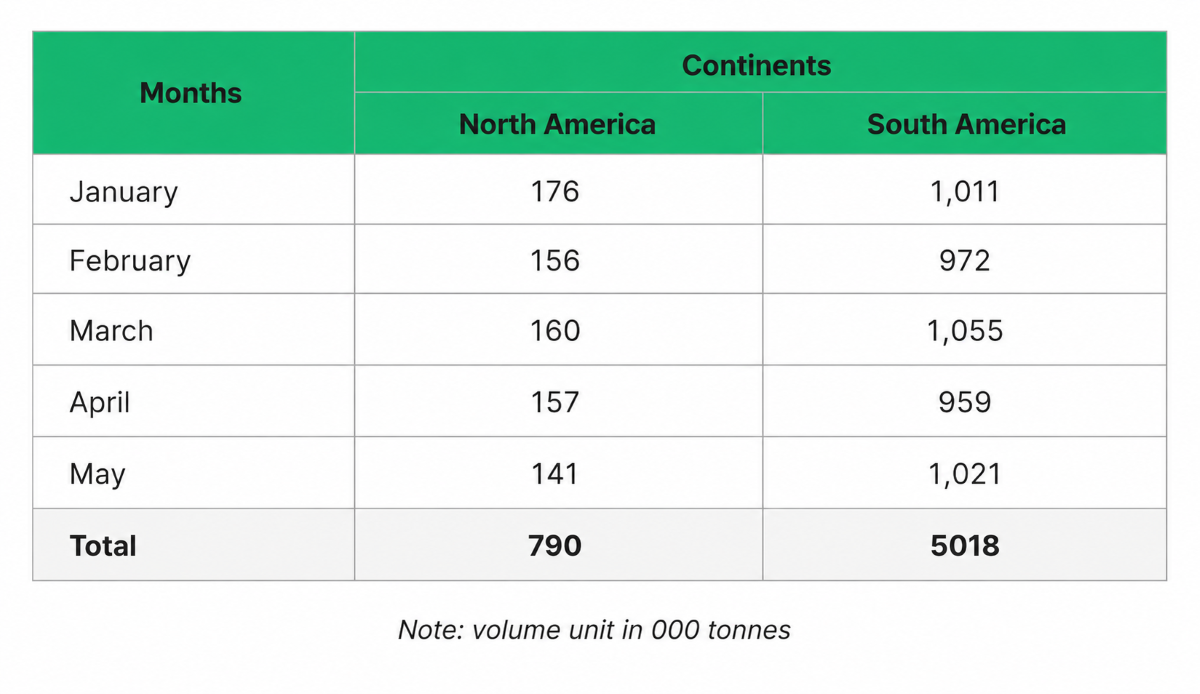

Has the alumina output of the Americas reflected a cooling effect across the global platform in the first half (H1) of 2026? According to industry data, cumulative alumina production in North America and South America from January to May totals 5.81 million tonnes. While the joint output registers a minor year-on-year dip of 0.38 per cent from 5.83 million tonnes in the same period of 2025, has the case been the same for the Americas on a singular basis?

{alcircleadd}As of January-May, alumina produced in North America amounted to 790,000 tonnes, of which chemical-grade accounted for 169,000 tonnes and metallurgical grade for 621,000 tonnes.

In the same period, South America produced 5.02 million tonnes, of which chemical grade totalled 389,000 tonnes and metallurgical grade contributed 4,629,000 tonnes.

Handling 86.4 per cent of the cumulative output, South America, therefore, dominates the Americas’ alumina production.

Explore: The most comprehensive and forward-looking industry-focused report — Global Bauxite & Alumina Market Forecast to 2036: Supply–Demand, Trade Flows & Price Report

Growth rate by months

From January to May, the alumina production trend in the Americas, as reported by the International Aluminium Institute (IAI), has been like this:

Based on the monthly figures, the average production volume for June in North America and South America would stand at around 158,000 tonnes and 1 million tonnes, respectively.

Hence, as the industry awaits the official June production update, the forecast for the first half (H1) of 2026 amounts to

North America has consistently remained considerably behind in the output race, largely due to the long-term decline in domestic alumina and aluminium production in North America over the years. Hence, the decline in demand has resulted in a decline in production growth.

South America, on the other hand, continues to be a prominent producer as well as exporter. Hosting Brazil – the third-largest alumina-producing country with an annual capacity of 10 million tonnes after China and Australia – the continent exports the majority of its alumina output.

According to the data accumulated from the UN Comtrade, as of 2025, major importers of South American alumina were

Alumina production over the years

Comparing the January-May figures of 2026 Y-o-Y, the trend looks like this:

North America’s 2026 output dropped 8.35 per cent Y-o-Y from 862,000 tonnes in 2025. The 2025 figure, too, fell by 7.4 per cent Y-o-Y from the 931,000 tonnes in 2024.

South America’s 2026 output improved by a modest 1 per cent Y-o-Y from 4.97 million tonnes in 2025. Likewise, the 2025 output dropped 1.78 per cent Y-o-Y from 5.06 million tonnes in 2024.

Hence, the yearly comparisons depict mainly a declining trend in alumina production. Although the South American output has improved since 2025, it has not been able to offset the deficit levels of 2024.

North America’s production decline can be attributed to the major operational overhauls at the Gramercy refinery operated by Atalco (Atlantic Alumina). Optimisation measures such as improved bauxite blend efficiency and other operational adjustments have slowed down the production momentum. While it produced 1,000 tonnes more in Q1 than in Q4 2025, picking up the previous momentum to mitigate the deficit might take a longer span of time.

Refinery operations across the region remained under strain from elevated labour and energy costs, weighing on production economics. Meanwhile, restructuring amid challenging market conditions in 2024 and 2025 led to lower operating rates. Production was further affected by maintenance-related interruptions and shipment delays, including those reported by producers such as Alcoa.

South America’s production is largely backed by Hydro’s Alunorte refinery in Brazil, the largest alumina refinery in the world with an annual capacity of 6.3 million tonnes.

The infrastructure ramp-ups made in 2024, including the bauxite slurry pipeline systems, enabled the Y-o-Y gain of 1 per cent. However, the drop in alumina pricing across the London Metal Exchange (LME) graph may have hindered a faster production surge. While alumina prices in the same period last year hovered around USD 365 per tonne, the average benchmark in 2026 has been around USD 305.38 per tonne.

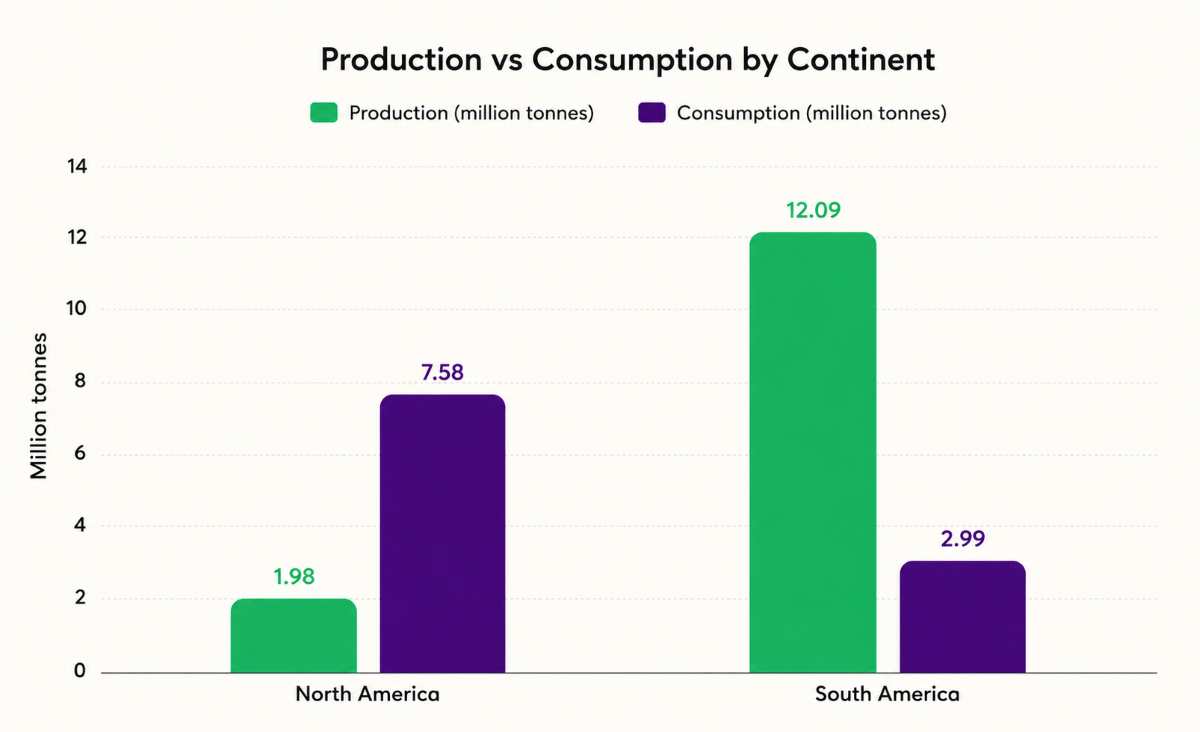

Production vs consumption

As of 2025, the alumina production and consumption trend of the two continents is as follows:

While North America produces only 26.12 per cent of the alumina that it consumes, South America consumes only 27.73 per cent of its total alumina output.

Hence, the trends give two clear understandings of the two continents, i.e., North America’s alumina production is mainly used as domestic feedstock, with the lion’s share imported from overseas.

Meanwhile, the majority of the South American-produced alumina is exported overseas, including to North American nations, with less than one-fourth stocked for domestic consumption.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

Case scenario: The demand-production dynamics

The North American alumina industry’s future is hanging on various factors that might drive its contraction or expansion.

Scenario A: If the primary aluminium price continues to rise but demand continues to fall, the North American alumina sector might not see any boost in production.

However, recent improvements, such as the joint venture of Century Aluminum and Emirates Global Aluminium (EGA) to build a 750,000-tonne aluminium plant in Oklahoma and the announcement by Magnitude 7 Metals of restarting its 75,000-tonne primary aluminium smelter in Missouri, are likely to drive the demand for alumina.

Scenario B: With the easing of the geopolitical tensions in the Middle East, coupled with the factor of increased aluminium scrap supply, as projected by InCred Research Services, the aluminium price will start to fall. However, the demand would continue to rise. In that case, aluminium production would see a boost, and concurrently, alumina demand would either remain firm or increase.

While South America continues with robust output and stable exports, North America's structural weaknesses may persist. If aluminium demand strengthens despite softer prices, alumina consumption is likely to stay firm.

However, North America's recovery will depend less on market conditions and more on the successful commissioning of new smelting capacity and operational improvements, while South America remains best positioned to capture any rise in global demand.

Responses