您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The image used in this article is generated with an AI tool and does not depict any real-time moment

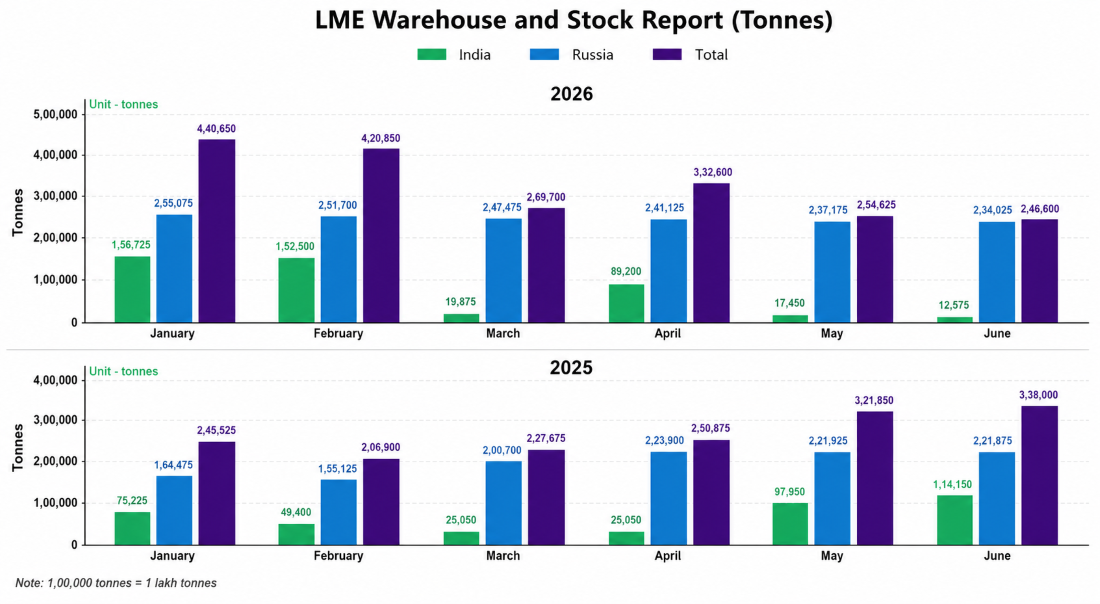

London Metal Exchange (LME) aluminium warehouse inventories have almost halved in 2026. Warehouse stocks fell from 440,650 tonnes in January to 246,600 tonnes by June, a decline of nearly 45 per cent. At first glance, that simply looks like metal leaving exchange warehouses. But look closer and the picture becomes far more intriguing.

{alcircleadd}Russian-origin aluminium now accounts for almost 95 per cent of the metal remaining on LME warrant, while Indian inventories have repeatedly entered and exited the exchange.

So what exactly is happening? The answer lies in two completely different stories unfolding inside the same warehouse system.

One warehouse, two very different inventory trends

The decline in total LME inventories tells only part of the story. A closer look at the data shows that Russia and India followed remarkably different inventory trends despite remaining the exchange's two largest warehouse origins.

Russian-origin aluminium accounted for around 58 per cent of total inventories in January and 60 per cent in February. As stocks from other origins declined more rapidly, Russia's share rose to approximately 92 per cent in March. A temporary recovery in Indian inventories reduced that figure to around 73 per cent in April, before it increased again to approximately 93 per cent in May and nearly 95 per cent in June.

The increase in Russia's share, however, was accompanied by only modest changes in Russian warehouse stocks. Inventories eased from 255,075 tonnes in January to 251,700 tonnes in February, before declining to 247,475 tonnes in March, 241,125 tonnes in April, 237,175 tonnes in May and 234,025 tonnes in June. Explore: The most comprehensive and forward-looking industry-focused report – Global Bauxite & Alumina Market Forecast to 2036: Supply–Demand, Trade Flows & Price Outlook

India's inventory trend looked markedly different.

Warehouse stocks slipped slightly from 156,725 tonnes in January to 152,500 tonnes in February (-2.7 per cent), before falling sharply to 19,875 tonnes in March (-87.0 per cent). They then recovered to 89,200 tonnes in April (+348.8 per cent), before declining again to 17,450 tonnes in May (-80.4 per cent) and 12,575 tonnes in June (-27.9 per cent).

2025 tells a very different warehouse story

The contrast becomes even clearer when compared with the first half of 2025.

Unlike 2026's steady decline, LME aluminium inventories recovered after an early setback. Total on-warrant stocks fell from 245,525 tonnes in January to 206,900 tonnes in February, before rising steadily to 338,000 tonnes by June.

Russia remained the largest warehouse origin throughout that period, but its inventories broadly reflected the recovery in overall exchange stocks. Holdings declined from 164,475 tonnes in January to 155,125 tonnes in February, before rising to 200,700 tonnes in March and 223,900 tonnes in April. Inventories then remained broadly stable at 221,925 tonnes in May and 221,875 tonnes in June.

India also followed the broader recovery, although its inventory movements remained more volatile. Stocks declined from 75,225 tonnes in January to 49,400 tonnes in February, before reaching 25,050 tonnes in both March and April. The trend then reversed sharply, with warehouse inventories climbing to 97,950 tonnes in May and 114,150 tonnes in June, contributing significantly to the overall recovery in LME stocks.

The rebound coincided with Vedanta's BALCO preparing to commission its 435,000-tonne annual aluminium expansion during the second quarter of 2025, bringing additional Indian metal to the market and supporting higher warehouse registrations.

What changed between the two years?

Two developments reshaped aluminium trade during the first half of 2026.

The first was the Iran-US conflict, which disrupted aluminium production in the Gulf and tightened physical supply across the region. As buyers searched for alternative sources of metal, Indian producers found stronger opportunities outside the LME warehouse system.

The second was the continuing impact of US and UK sanctions on Russian aluminium. While Russian warehouse inventories declined only gradually, stocks from other origins fell much faster, leaving Russian-origin aluminium to account for an increasingly larger share of the metal remaining on LME warrant.

Together, these developments explain why India and Russia followed two very different inventory trends despite operating within the same warehouse system.

India's disappearing inventories tell a different story

Unlike Russia, India's warehouse movements were driven primarily by changing opportunities in the physical aluminium market rather than sanctions.

Producers such as Hindalco Industries and Vedanta's BALCO have never been structural suppliers to the LME warehouse system. Their primary focus remains domestic customers and long-term bilateral export markets, with aluminium registered on LME warrant only when exchange delivery offers the most attractive commercial return.

That flexibility became particularly evident during the first half of 2026.

The Iran-US conflict began on February 28, 2026, before escalating on March 28, when missile strikes hit two major Gulf aluminium producers—EGA's Al Taweelah smelter in the United Arab Emirates and Alba in Bahrain. The attacks temporarily removed roughly half of the Gulf's aluminium production capacity, tightening regional supply and creating an immediate search for alternative sources of primary aluminium.

The disruption created an immediate scramble for alternative supplies of non-Gulf, non-Russian aluminium. Buyers were prepared to pay significant premiums, creating stronger incentives for Indian producers to sell directly into physical markets instead of leaving aluminium registered on LME warrant.

The shift was quickly reflected in LME warehouse inventories. After declining marginally from 156,725 tonnes in January to 152,500 tonnes in February, Indian stocks plunged to 19,875 tonnes in March. Inventories recovered to 89,200 tonnes in April, but the rebound proved short-lived, falling again to 17,450 tonnes in May and 12,575 tonnes in June.

The sharp fluctuations underline how differently Indian producers use the LME warehouse system. Rather than treating exchange warehouses as a permanent storage destination, they move metal in and out depending on where commercial opportunities are strongest. When physical premiums rise above the returns available through LME delivery, warehouse registrations become less attractive and metal is redirected to customers willing to pay more.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

Where India’s aluminium went?

Hindalco Industries said exports to Japan, South Korea and Taiwan increased after the company helped bridge supply gaps created by the West Asia crisis. Around 70 per cent of Hindalco's aluminium production is absorbed by the domestic market, while exports account for approximately 25–30 per cent.

Official trade data supports that shift. India's aluminium exports to South Korea increased from 27,061 tonnes in the fourth quarter of 2025 to 64,010 tonnes in the first quarter of 2026. Shipments to Japan rose from 34,623 tonnes to 40,330 tonnes, while exports to China more than doubled from 11,567 tonnes to 25,321 tonnes over the same period.

Russia's growing warehouse share reflects the lasting impact of sanctions

Russia's increasing share of LME warehouse inventories was not driven by rising warehouse inflows but by the way sanctions continued to reshape trading patterns for Russian aluminium.

Since April 2024, the United States and the United Kingdom have prohibited Russian aluminium produced after that date from being delivered into LME warehouses, while metal produced before the cut-off date remains eligible for exchange delivery.

Although pre-sanctions metal can still be traded legally, buying patterns have shifted. Banks financing commodity transactions, industrial consumers with environmental, social and governance (ESG) commitments, and companies seeking to reduce reputational risk have increasingly avoided Russian-origin aluminium. Verifying when individual batches were produced has also made procurement more complicated.

As a result, Russian warehouse stocks declined only modestly during the first half of 2026, while inventories from other origins were withdrawn much faster. As competing stocks disappeared, Russian-origin aluminium accounted for a larger share of the metal remaining on warrant.

A similar pattern emerged in the LME copper market. Chinese-origin copper represented around 53 per cent of LME copper inventories before rising to approximately 59 per cent in June, even though Chinese warehouse stocks also declined, because inventories from other origins fell more rapidly.

The warehouse data therefore reflects a relative shift rather than an increase in Russian warehouse registrations.

That, however, raises another question: if many Western buyers were avoiding Russian aluminium, why did Russian warehouse stocks continue to decline?

Who was buying Russian aluminium?

The answer lies largely outside the LME warehouse system.

China has increasingly sourced primary aluminium directly from Russian producers rather than through exchange warehouses. Chinese imports of Russian primary aluminium rose from around 291,000 tonnes in 2021 to 1.13 million tonnes in 2024, before increasing another 48 per cent year on year during the first four months of 2025.

Trade data reinforces this shift. Russia's aluminium exports to China increased from 477,678 tonnes in the fourth quarter of 2025 to 589,133 tonnes in the first quarter of 2026.

China was not the only destination. A smaller group of buyers, particularly price-sensitive consumers across Asia, continued purchasing eligible Russian aluminium from LME warehouses whenever discounts made it commercially attractive, especially as tighter regional supply supported premiums following disruptions in the Gulf.

Taken together, the diverging paths of Indian and Russian aluminium show that LME warehouse data is no longer simply a measure of inventory levels-it has become a reflection of shifting trade flows, sanctions, geopolitical disruption and changing buying behaviour across the global aluminium market.

Responses

A proud

ASI member

AL Circle Private Limited | CIN: U72200WB2017PTC221175

Registered Office: Ecospace Business Park, Block 3A, Unit 401A, New Town, Rajarhat, Kolkata, WB 700160

Corporate Office: Ecospace Business Park, Block 3A, Unit 401A, New Town, Rajarhat, Kolkata, WB 700160

© 2026 AL Circle. All rights reserved. AL Circle is not responsible for content from external sources.

_(1)_0_0.png)