您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

This image has been sourced from BigMint official website

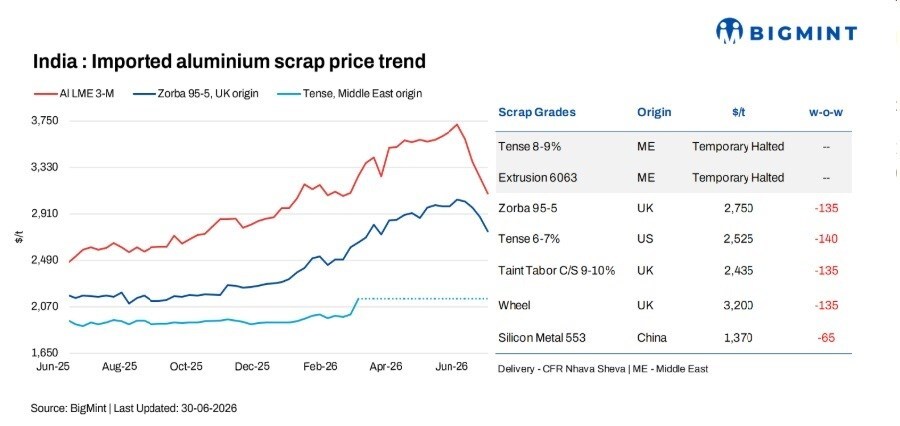

India's imported aluminium scrap prices fell sharply w-o-w, pressured by weaker LME aluminium prices and sluggish demand from domestic buyers.

{alcircleadd}According to BigMint's latest assessment for CFR Nhava Sheva deliveries, UK-origin zorba 95-5 scrap prices declined by USD 135 per tonne W-o-W to USD 2,750 per tonne, while US-origin tense 6-7 per cent scrap prices dropped by USD 140 per tonne W-o-W to USD 2,525 per tonne, as subdued buying interest and bearish global market sentiment continued to weigh on import prices.

LME aluminium tumbles W-o-W

…and so much more!

SIGN UP / LOGINResponses