您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The US dollar rebounded against a basket of currencies on the first day of the week and then fell on Tuesday ahead of an expected US interest rate cut from the Federal Reserve. Though it registered a gain mid-week, the greenback ended the week lower.

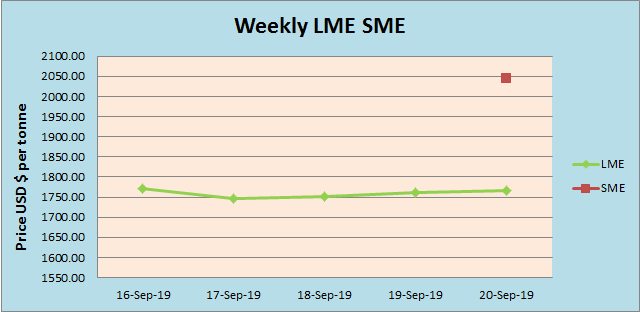

LME base metals started the week slightly higher but dropped on Tuesday, on growing concerns about demand in China after the release of bleak economic data and strong dollar. The prices did not see any drastic movement rest of the week and continued on a steady upward curve. LME aluminium started the week with US$ 1770.5 per tonne and after a drop to USD1746.5 per tonne it continued higher and closed the week at US$ 1766 per tonne on Friday September 20. Three-month LME aluminium also rebounded to a three-day high and ended the week at US$ 1792 per tonne after Friday’s closing.

{alcircleadd}

As on September 20, Friday, LME aluminium cash (bid) price stood at US$ 1765.50 per tonne, LME official settlement price stands at US$ 1766 per tonne; 3-months bid price stands at US$ 1790 per tonne, 3-months offer price is US$ 1792 per tonne; Dec 20 bid price stands at US$ 1863 per tonne, and Dec 20 offer price stands at US$ 1868 per tonne.

The LME aluminium opening stock dropped to 897900 tonnes. Live Warrants totalled at 700025 tonnes, and Cancelled Warrants were 197875 tonnes.

LME aluminium 3-months Asian Reference Price is hovering at US$ 1798 per tonne.

SHFE Aluminium Price Trend

China market reopened on September 16 after the festive holiday. SMM data showed that social inventories of primary aluminium in China have fallen for five weeks. Improving consumption in a high season in September-October and expectations of greater supply pressure in November widened the backwardation on SHFE aluminium. SHFE aluminium continued trading higher over the week. This will continue to support price in the short term.

The most-active SHFE November contract came off from highs in the beginning of the week on Tuesday, falling below support from the 20-day moving average and closing down 1.04% at RMB 14,280 per tonne. The November contract ended its four straight sessions of decline on Friday as shorts rallied the contract from a low of RMB14,650 per tonne, to an intraday high of RMB 14,240 per tonne, before it ended up 0.46% at RMB 14,225 per tonne.

Resumption of primary aluminium smelters grew worries about nearby higher supply, and this resulted in the previous pullback in aluminium prices. The contract is expected to trade rangebound next week with the market awaiting environmental policies after the National Day holiday.

Responses