您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

(Continued from Part I)

LME/SME price trends

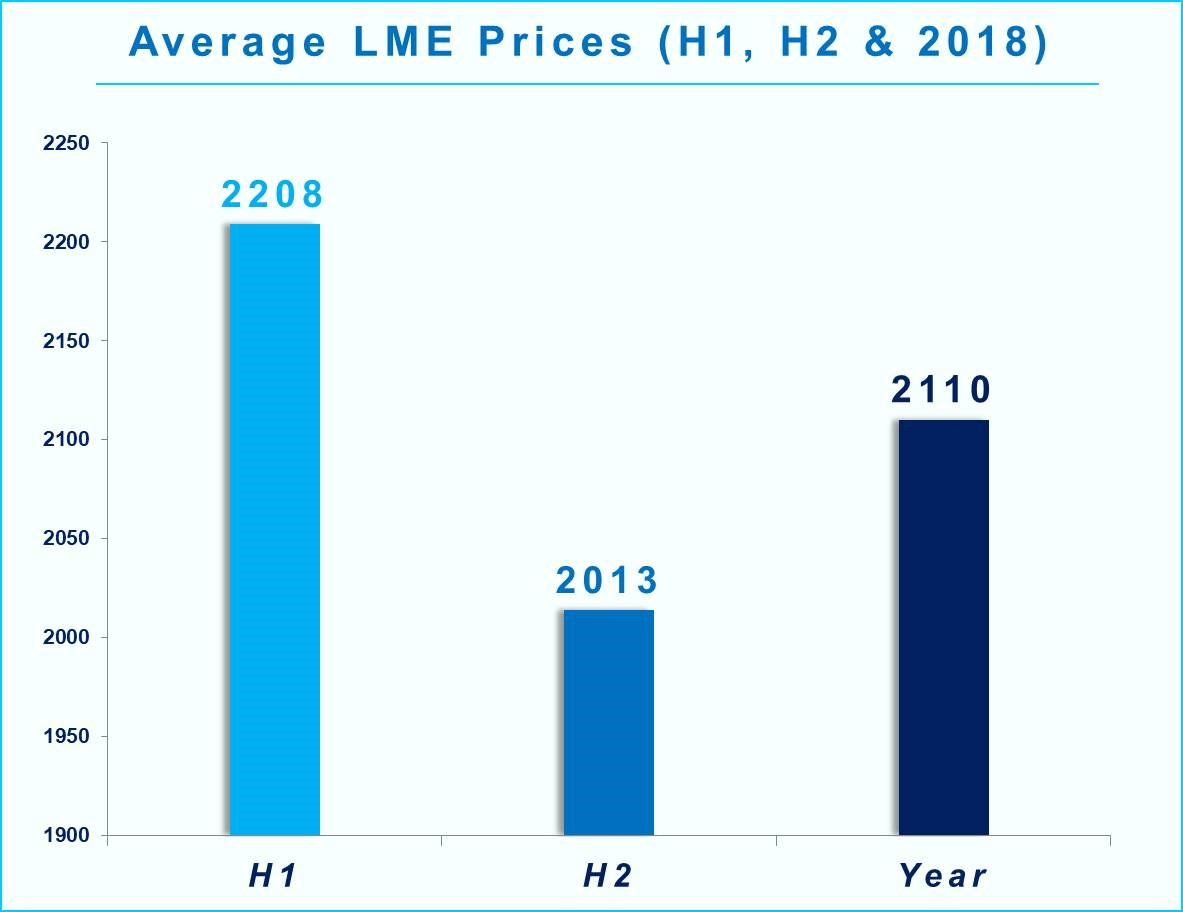

{alcircleadd}An analysis of the LME and SME price trends in H1, H2 and the whole year 2018 will give us an idea about how the prices were impacted by the events in the aluminium supply scenario. As the sanctions hit the market in April and LME prices were pushed higher to about US$2602.5 per tonne, the average LME price for H1 2018 skyrocketed to US$ 2208/tonne. It was further supported by the increasing alumina prices due to sanctions on Aughinish alumina and 50% capacity cut in Alunorte refinery. Prices started correcting when the sanction deadlines were extended and came to settle in June.

LME prices started its downtrend during the second half of 2018. This was mostly driven by the following factors:

The prices touched a sixteen months low when it touched US$ 1869 per tonne at the end of December after the US Treasury had announced it would lift sanctions on Rusal. This brought down average LME price in H2 2018 to US$ 2013/tonne. The average LME price for 2018 stood at US$ 2110/tonne, 7.4% up from 2017 average of US$ 1963/tonne.

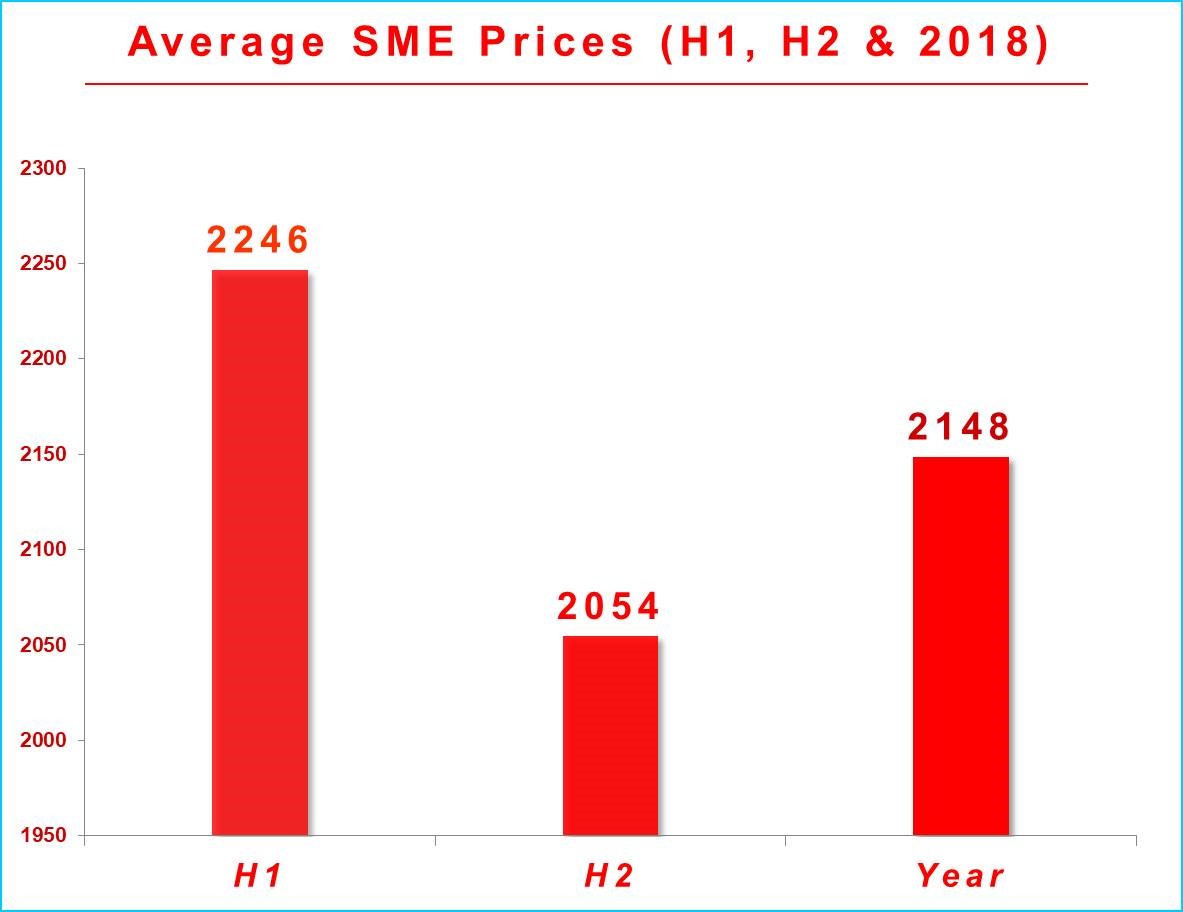

LME prices have influenced the momentum in SME (Shanghai Metals Exchange) aluminium prices. The first half of the year has been bullish for China aluminium prices as it was supported by a tight supply, higher input costs (alumina and coal) and lower international aluminium prices.

However, the changes started showing up towards the end of Q2 when re-commissioning of new capacity increased the inventory and cost support started declining. Chinese aluminium prices fell to their lowest in more than two years in November and clocked a third successive monthly decline, as stalling manufacturing growth compounded plentiful supply amid relatively lenient winter output curbs.

China's official Purchasing Managers' Index (PMI) fell to 50 in November, missing market expectations and down from 50.2 in October. Shanghai aluminium shed 2.8 per cent over November, which saw two-year lows hit several times, leaving smelters in China struggling to turn a profit and leading some to cut output even without being ordered to do so on environmental grounds. However, despite the fluctuations, the average yearly price remained descent at US$ 2148/tonne, higher than the yearly average of US$ 2136/tonne in 2017.

Inventory Situation

Global LME aluminium inventory stood at 1.09 million tonnes at the beginning of the year and increased on the back of US sanctions on Rusal to about 1.3 million tonnes in April. However, after the easing of sanctions, inventories dropped and hovered around 1 million tonnes in H2 2018. The inventory showed signs of increasing at the end of the year when it stood at 1.1 million tonnes. LME warehouses in the US did not experience a major increase in stocks on the back of strong demand, and Asia saw an increase due to more supply and slow demand in China and Europe is expected to remain flat.

China Aluminium Inventory

On December 27, 2018, as per SMM statistics of domestic aluminium inventories (SHFE warrants included), total primary ingot inventory stood at 1.29 million tonnes. The inventory level is hovering at this level for some time for the seven major cities of Shanghai, Wuxi, Hangzhou, Gongyi, Nanhai, Tianjin and Chongqing. According to Shanghai Metals Market statistics, China’s social inventory of primary aluminium including SHFE warrants stood at 1.78 million tonnes as of January 2, 2018.

Foreign Trade Scenario

Trade tariffs on aluminium and counter tariffs and sanction on Rusal had an impact on international trade of aluminium. UC Rusal continues to struggle to export any of its aluminium production out of Russia despite an easing of the US sanctions on April 23, when the US Treasury eased restrictions on Rusal till October. Shipments were only trickling out of the country and mostly towards Asia due to financing and banking issues. The company resumed shipments to some customers with pre-existing contracts in May. Rusal exported 197 thousand metric tons in May, tripling its output from the previous month. According to a Reuter’s report, Rusal raised its aluminium exports by 4 per cent in October 2018, about 272,000 tonnes after the easing of sanctions.

Indian aluminium makers, including Hindalco Industries and Vedanta Ltd, boosted sales to Japan as US sanctions against Russia’s Rusal and import tariffs shake up traditional supply routes. However, imports of aluminium ingot from India doubled in the first eight months of 2018 from a year ago, Japanese trade data shows, while imports of alloy - which include higher-value products - surged 11-fold off a tiny base. Japan took 59,545 tonnes of aluminium ingot in the eight months to March, double a year ago, while material from Russia fell 21 per cent to 175,694 tonnes, Japanese trade data showed. Imports of aluminium alloy from India jumped to 3,008 tonnes over the same period, while Russian imports fell 10 per cent to 185,685 tonnes.

China's aluminium exports rose to a record in the first quarter of 2018, and analysts said the country's producers were benefitted further due to higher prices and Rusal’s temporary exit from the trading scene.

Canada’s aluminium and aluminium alloy export to the U.S. stood at 1.8 million tonnes in the period from January to October, a slight drop from about 2 million tonnes in 2018, which indicated the biggest supplier of aluminium to the U.S. has not been severely affected by the import tariffs imposed by Trump.

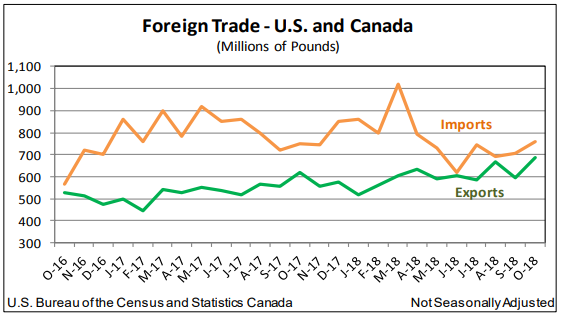

According to the data from Aluminum Association, after the implementation of tariffs, aluminium imports by the U.S. reported a decline. Below graph shows the monthwise trend in last 3 years:

Total aluminium exports (ingot and semi-finished products) from the U.S. and Canada (excluding cross-border trade) totalled 1.3 million tonnes through October 2018, up 16.3 per cent from the same period of 2017. Total aluminium imports were off 5.6 per cent to 3.6 million tonnes.

A short term outlook

The LME aluminium prices are expected to hover at a level of US$ 1845/tonne to US$ 1880/tonne in the first quarter of 2019. The inventory level in LME and SME will not decrease significantly as the demand remains sluggish. Cost support will be minimum as restarting of operations in Alunorte and sanction lifting on Aughinish alumina indicates enough supply availability in the first quarter. Harbour projects a surplus market for aluminium in 2019. Hydro and CRU projected Global primary market expected to be in deficit also in 2019. We do not see a surplus market in ex-China in 2019 as aluminium demand continues to be strong. In China it would be a surplus market and the global market is likely to remain balanced or on a slight deficit.

Responses