您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The year 2018 has seen the highest and lowest in terms of aluminium price growth and production of primary aluminium is estimated to be slightly higher (about 1.3%) in comparison to 2017. The year was marked by supply uncertainty in alumina and aluminium which pushed the prices higher in the first quarter. Tariffs and punitive sanctions created panic in the market disrupting the international trade. However, they also encouraged restarting of closed aluminium operations by Alcoa and Century Aluminum in the U.S. While prices saw some unprecedented gains, towards the end of the year they touched rock bottom as the supply uncertainties eased out but economy continued to move slower in China and the trade war waged by the U.S. reached no solution. We are analysing the various developments in the primary aluminium sector in 2018 in order to connect the dots and see how they shaped the industry over the year while setting the stage for 2019.

Production

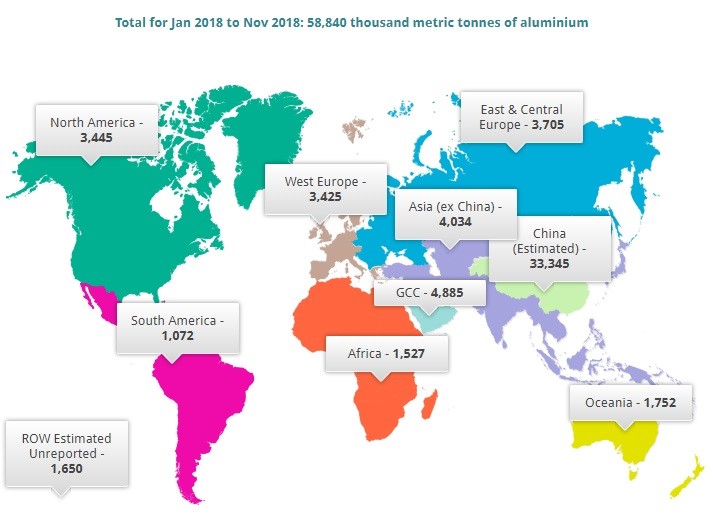

Total primary aluminium production from Jan 2018 to Nov 2018 stood at 58.8 million tonnes, up 1.3 per cent from 58 million tonnes of aluminium produced in the same period of 2017 (International Aluminium Institute). For the year 2017 the total aluminium production stood at 63.4 million tonnes and the total for 2018 is expected to stand at about 64.2 -64.5 million tonnes. IAI also estimated about 33.3 million tonnes of aluminium production in China in the same period, about 56% of the total production. China’ National Bureau of Statistics (NBS) confirmed that China’s total aluminium production in 2018 stood at 35.8 million tonnes up 7.4 per cent from the previous annual record in 2017 and the December volume stood at 3.05 million tonne. The increase in production is driven by the fact that environmental capacity cuts were not strict on alumina and aluminium sector.

Total production in H1 stood at 31.7 million tonnes, while that of H2 stood at 32.5 million tonnes(E). While China production stood at 17.9 million tonnes, the ROW production stood at 13.8 million tonnes in H1 2018. During the second half of 2018, China produced about 18 million tonnes while the ROW produced an estimated 14.5 million tonnes.

Demand Supply Scenario

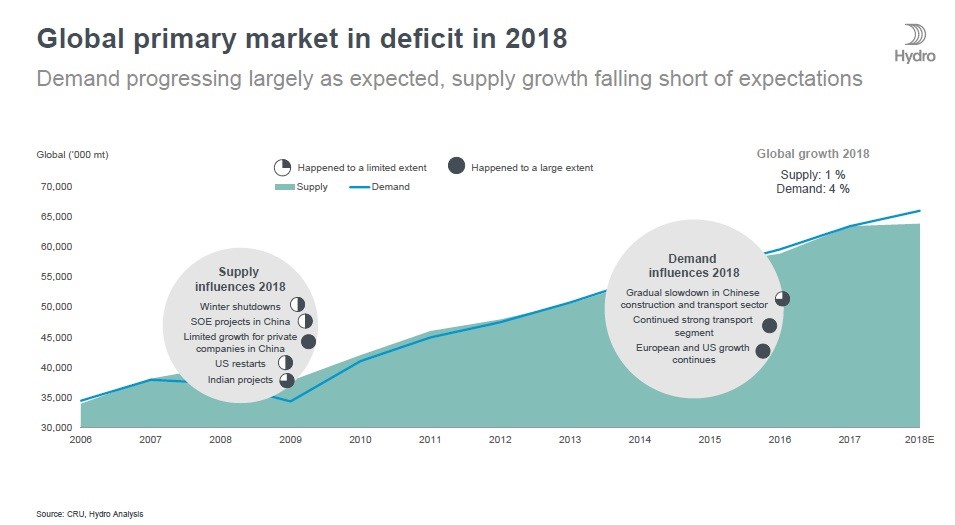

Global primary market was in slight deficit in 2018 as analysed by CRU & Hydro. Demand growth was solid, especially from the transport segment, largely as expected. Supply growth was falling short of expectations as reopening of new capacity was slow in China in the first two quarters. Production in North America, Latin America, Western Europe and Africa fell in the first half of 2018 due to smelter problems.

North American production should have been rising with the restart of potlines by Alcoa at its Warrick smelter and Century Aluminum at its Hawesville smelter. In both cases, however, it’s been a case of two steps forward, one step back. Alcoa could not start the third potline due to a power outage in May. Century lost one line at its Sebree plant, also in Kentucky, for similar reasons. The union lock-out at the Becancour (ABI) smelter in Canada, majorly owned by Rio Tinto reported production drop of 74,000 tonnes in January-June from 218,000 tonnes in the year-earlier period.

However, production slightly improved during the second half. The demand growth stood at about 3-4% while supply growth was about 1%. The total demand was about 65 million tonne while production stood at about 64.2 million tonnes (E).

The market is however moving to a surplus as indicated by growing LME aluminium inventory in December and the falling LME prices. China’s economy is growing slow indicating more stocking of aluminium in 2019.

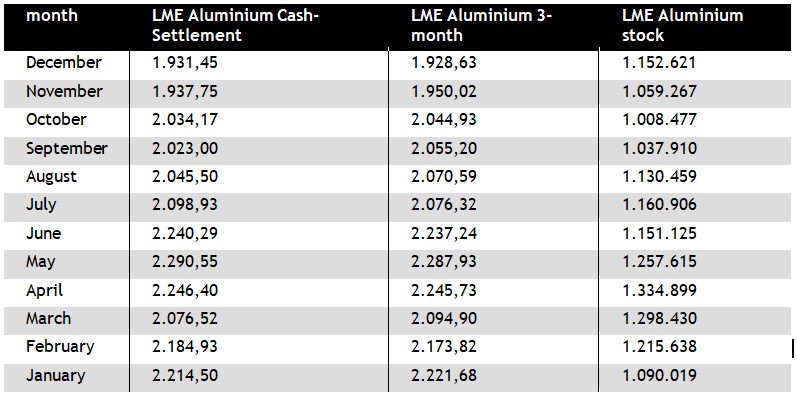

Monthly AVG LME price and aluminium stock

Trump’s 10% tariffs on all aluminium import

The aluminium supply scenario received the first hit when Trump imposed a global tariff of 25 per cent on steel imports and 10 per cent tariff on aluminium imported from all countries in March 2018. Though a few countries got exemptions on the tariff, all its major trading partners including Canada, Mexico, European Union and China were imposed heavy tariffs initiating the beginning of a long trade wars between these countries with the US. This led to retaliatory tariffs imposed by the countries affected by aluminium tariffs

Sanction Against Rusal

However, prices were taken to an unforeseen level when, Trump administration imposed punitive sanctions on Rusal and its owner Oleg Deripaska on April 7 and following it, London Metal Exchange suspended Rusal’s aluminium from April 17. Rusal accounts for about 14 per cent of world aluminium production outside China. The company not only supplies about 6.5 % of global aluminium demand but also supplies about 7 per cent of the world’s alumina.

Benchmark aluminium price on London Metal Exchange shot up to the highest in almost 7 years and closed at US$2602.5 per tonne on Thursday, April 19. This was driven by panic buying as Rusal’s consumers feared they might not be able to buy or trade metal from Rusal. The prices started correcting during the end of April when the Treasury had extended its deadline for U.S. consumers to wind down business with Rusal.

US treasury announced its intention to remove sanctions against Rusal on December 19, 2018. Rusal’s parent company had been negotiating with the US Treasury to free itself from the sanctions. US Treasury announced it would remove sanctions against Oleg Deripaska-owned Rusal after extending the deadlines for the full imposition of sanctions twice.

(To be continued in Part 2)

Responses