您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The US dollar dipped broadly on Friday after President Donald Trump ordered US companies to start looking for an alternative to China after Beijing imposed more tariffs on American goods. China announced retaliatory tariffs against about US$75 billion worth of US goods, putting as much as an extra 10% on top of existing rates. The dollar index slipped some 0.6% and finished at 97.65.

LME base metals closed mixed while SHFE metals ended mostly lower. LME aluminium edged higher and SHFE aluminium closed flat.

{alcircleadd}

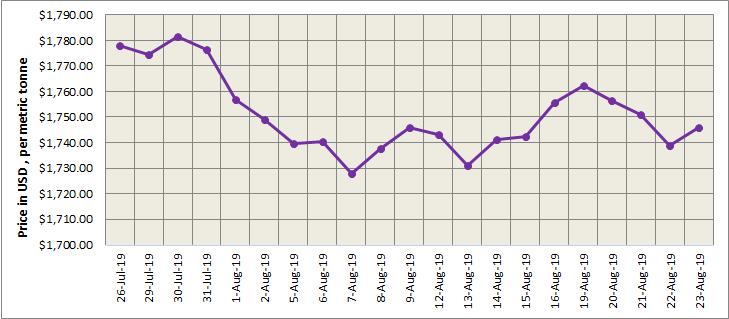

Three-month LME aluminium rebounded swiftly after the announcement of higher Chinese tariffs on American goods depressed base metal prices on Friday. It edged higher on the day and closed at RMB 1,767 per tonne, with the trading range expected at US$1,700-1,780 per tonne today.

As on August 23, Friday, LME aluminium cash (bid) price stood at US$ 1745 per tonne, LME official settlement price stands at US$ 1746 per tonne; 3-months bid price stands at US$ 1769.50 per tonne, 3-months offer price is US$ 1770 per tonne; Dec 20 bid price stands at US$ 1853 per tonne, and Dec 20 offer price stands at US$ 1858 per tonne.

The LME aluminium opening stock dropped to 935200 tonnes. Live Warrants totalled at 656500 tonnes, and Cancelled Warrants were 278700 tonnes.

LME aluminium 3-months Asian Reference Price is hovering at US$ 1788 per tonne.

SME and SHFE Aluminium Price Trend

The benchmark aluminium price on Shanghai Metal Exchange (SME) has dropped to stand at US$ 1991 per tonne today from US$ 2012 per tonne on Friday.

The greater unwinding of long positions knocked the most traded SHFE 1910 contract to a four-day low of RMB 14,240 per tonne, before the contract clawed back some losses to end 0.35% lower at RMB 14,285 per tonne. The SHFE October contract settled flat last Friday night at RMB 14,285 per tonne with support from fundamentals. It is expected to trade at RMB 14,250-14,350 per tonne today with spot premiums up to RMB 40 per tonne.

Investors appeared to have digested the news of less capacity in operation in Shandong and Xinjiang, and moved their positions to the forward contract. While supply holds stable with capacity cuts in Sichuan offset by newly-commissioned capacity in Guangxi, rising social inventories will hurt long confidence. SHFE aluminium is expected to remain firm and rangebound.

Responses