您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

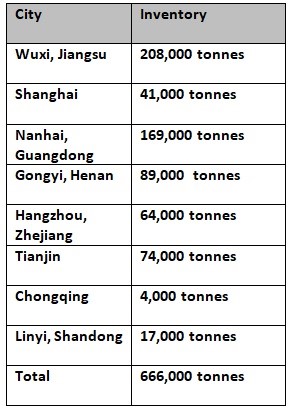

According to the Shanghai Metals Market, primary aluminium inventories in China witnessed a decrease of 9,000 tonnes week-on-week across eight major consumption areas, including SHFE warrants. Therefore, on Thursday, September 22, the inventories totalled 666,000 tonnes, which in comparison with the month’s third Monday, September 19, shrunk by 19,000 tonnes. As of now, the inventories in September dropped by 122,000 tonnes as recorded in the same period last year and by 11,000 tonnes than in August.

Mainly, the inventory decreased in Wuxi, Nanhai and Hangzhou with arrivals from Wuxi and Gongyi being affected by prevailing pandemic restrictions and curtailed railway transportation in Xinjian. In fact the shipments of aluminium billet from Xinjian were also limited. The Nanhai inventory primarily fell due to the production cuts in Yunnan province. Anyhow, the open import window will suffice the domestic market demand to some level but the bonded zone inventory is just 30,000 tonnes if the direct imports and the logistical stocks are calculated together.

Last week, on September 15, primary aluminium inventories fell by 21,000 tonnes from the week before on Monday across eight major consumption areas to come in at 675,000 tonnes.

The chart below indicates the current status of primary aluminium inventories across China in more detail:

The aluminium ingot inventories plunged the highest in Wuxi by 5,000 tonnes, followed by a 3,000 tonnes drop in Nanhai and another 1,000 tonnes decline in Hangzhou.

In the other Chinese provinces, the price of aluminium ingot remained stoic at what they were last Monday. Chongqing remained halted at 4,000 tonnes, Linyi at 17,000 tonnes, Shanghai at 41,000 tonnes, Tianjin at 74,000 tonnes and Gongyi at 89,000 tonnes.

Journeying into the next week, China might witness an increased downstream restocking demand just before the National Day holiday, but the aluminium ingot social inventory will lay lower than usual with traits on going further down.

Responses