您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

According to the Shanghai Metals Market, primary aluminium inventories in China witnessed a steep downfall of 29,000 tonnes week-on-week across eight major consumption areas, including SHFE warrants. Therefore, on Thursday, July 21, the inventories totalled 668,000 tonnes, which in comparison with the month’s second Monday, July 11, shrunk by a substantial 55,000 tonnes. As of now, the inventories in July have shrunk by 161,000 tonnes in comparison with the same period last year.

The ingot social inventory has suddenly begun declining in July. Delayed arrivals and shipments added with transportation stagnancy due to the pandemic are gradually cutting down the ingot volume in Wuxi. While in Gongyi, the main issue seems to be the intake by local consumers which is heightening regional inventory stress. The aluminium ingot social inventory is estimated to maintain low volume owing to the recent density of arrivals and shipments.

Last week, on July 14, primary aluminium inventories fell by 26,000 tonnes from the week before across eight major consumption areas to come in at 697,000 tonnes.

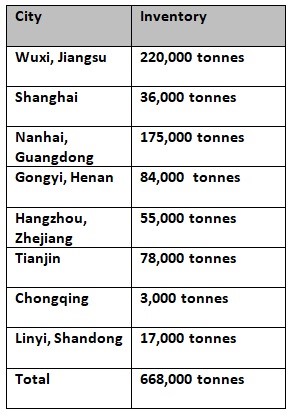

The chart below indicates the current status of primary aluminium inventories across China in more detail:

On July 21, the aluminium ingot inventories plunged the highest in Wuxi by 15,000 tonnes over a week to 220,000 tonnes from 235,000 tonnes, as recorded on July 14. Meanwhile, primary aluminium inventories in Gongyi shed 6,000 tonnes to rest at 84,000 tonnes. In Nanhai, inventories decreased by 5,000 tonnes to stand at 175,000 tonnes. Hangzhou saw a dip of 4,000 tonnes week-on-week to come in at 55,000 tonnes, while only the inventory in Chongqing augmented by 1,000 tonnes to rest at 3,000 tonnes.

The inventories in Tianjin, Shanghai and Linyi refrained from showing any change being fixed at 78,000 tonnes, 36,000 tonnes and 17,000 tonnes, as recorded on July 21.

Responses