您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

According to the Shanghai Metals Market, China's primary aluminium inventories increased by 18,000 tonnes week-on-week across eight major consumption areas, including SHFE warrants. Therefore, on Thursday, December 29, the inventories totalled 493,000 tonnes, which in comparison with the month's last Monday, November 26, escalated by 9,000 tonnes. As of now, the inventories in December dropped by 23,000 tonnes from the end of November and recorded 306,000 tonnes plunge from the same period last year.

The aluminium ingot output surges amalgamated with low downstream intake in the off-season are reasons affecting the social inventory so that they remain periodically stored in warehouses. Anyhow, the production cuts in Yunnan and Guizhou are also primary concerns that should be addressed formally before correcting the speed of cargo imports, in turn checking the inventory accumulation.

Last week, on November 22, primary aluminium inventories stood at 475,000 tonnes, which soared across eight major consumption areas to come in at 493,000 tonnes on December 29, Thursday, with a week-on-week augmentation.

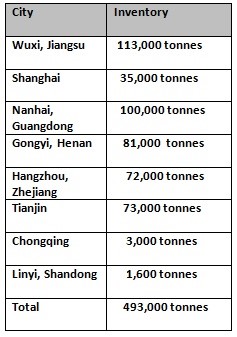

The chart below indicates the current status of primary aluminium inventories across China in more detail:

The provinces in China recorded altering aluminium inventories, with capacity rising the highest in Wuxi to 113,000 tonnes after earning 24,000 tonnes. Next in line was Gongyi, which saw 6,000 tonnes, in addition, to close at 81,000 tonnes. Other than that, inventories in Tianjin, Chongqing and Linyi remained stagnant at 73,000 tonnes, 3,000 tonnes and 1,600 tonnes.

The aluminium social inventory in Nanhai lost 8,000 tonnes, closing at 100,000 tonnes, followed by a 3,000 tonnes slump in Shanghai, pegging at 35,000 tonnes. In Hangzhou, the aluminium inventory shed 1,000 tonnes, settling at 72,000 tonnes.

Responses