您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

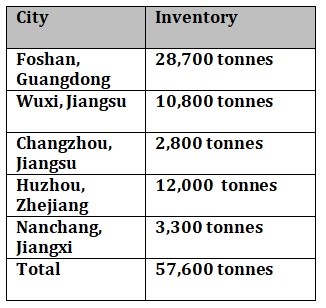

As of Thursday, December 22, SMM's social inventory of aluminium billets was 57,600 tonnes, a decrease of 3,800 tonnes from a week prior, primarily due to Foshan. According to SMM research, several aluminium billet factories in Inner Mongolia, Ningxia, and Gansu reduced or suspended production in the middle of December, 10–20 days earlier than in previous years, as a result of sharply declining orders, the COVID-19 pandemic's worsening effects after control measures were loosened, and the depressing real estate market.

The figure below provides further information on the current state of aluminium billet inventories in China:

The inventory in Wuxi hiked by 4,300 tonnes to stand at 10,800 tonnes from 6,500 tonnes recorded last week. On the same day, in Changzhou and Huzhou, the inventories increased by 1,000 tonnes to record 2,800 tonnes and 12,000 tonnes.

On the other hand, inventories in Foshan and Nanchang dropped by 9,900 tonnes and 200 tonnes to close at 28,700 tonnes and 3,300 tonnes. Additionally, most north Chinese billet producers sent their consignments with better conversion margins than Foshan. The inventory in Foshan decreased considerably as a whole.

_0_0.gif)

East China's stockpiles continued to grow slightly, and considering the weak downstream demand, the cargo movement among dealers was also orderly. The supply and demand for aluminium billets were weak in December. Because some suppliers have been shipping products straight to participants farther down the supply chain, the social inventory is anticipated to increase dramatically.

Responses