您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

This image has been sourced from https://news.metal.com/

PV aluminium extrusion: This week, the operating rate of the surveyed industry sample of PV frame enterprises held up well. Leading extrusion manufacturers continued to run at full capacity, supported by ample long-term orders on hand, with the core driver being the advancement of centralised PV projects toward year-end.

{alcircleadd}In H2, the production schedule situation for downstream leading module enterprises is expected to be better than H1, but monthly incremental growth in PV frame demand will be steady M-o-M, limiting the extent of demand improvement. SMM also learned that PV frame processing fees have remained stable recently without notable changes.

On balance, the operating rate of PV frame enterprises will likely maintain a consolidating-to-firm pattern in the near term.

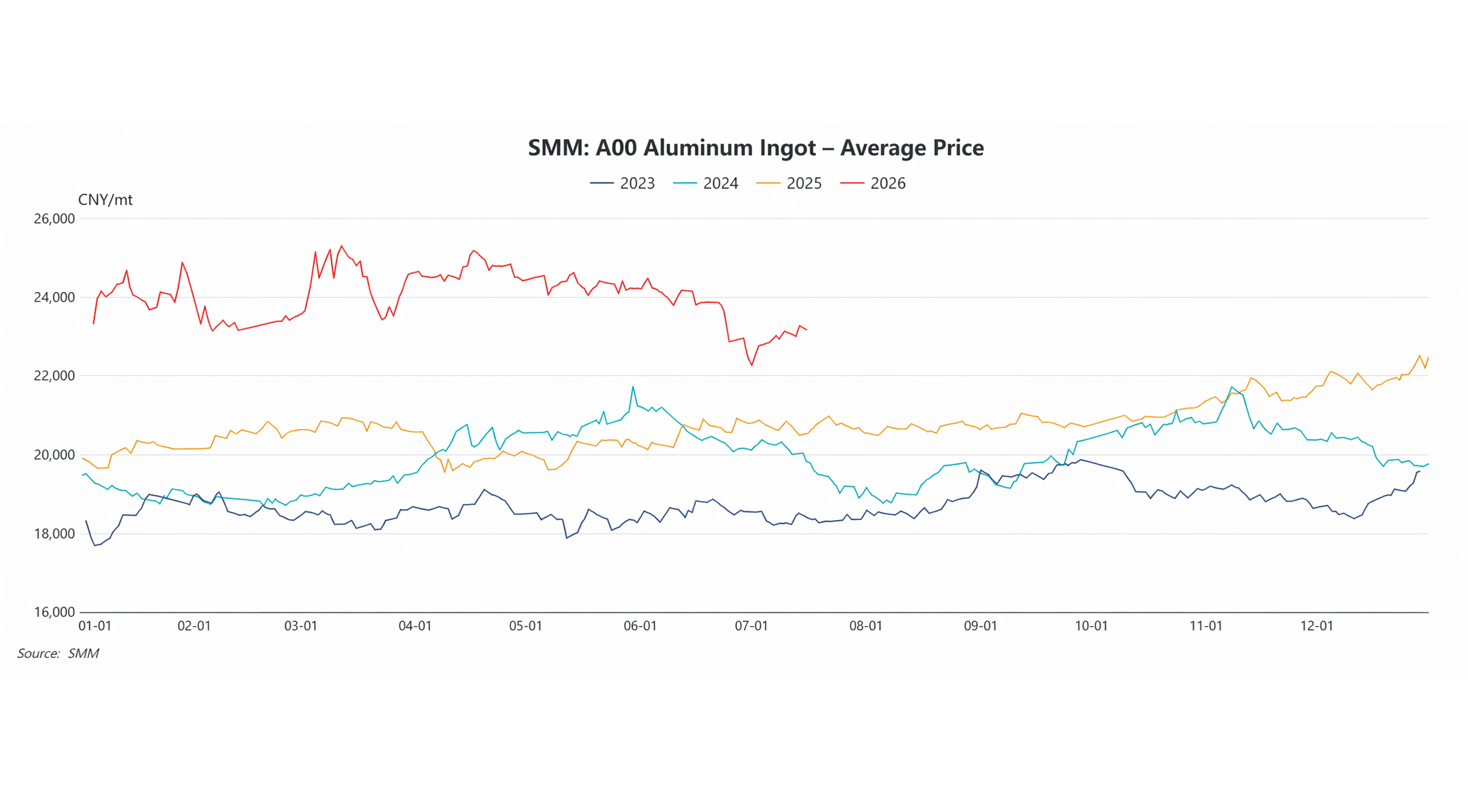

Raw material prices: During the period (July 13-July 16, 2026), the SMM A00 weekly average price was RMB 23,155 per tonne, up 0.9 per cent from the prior week. Overall, recurring Middle East tensions, lingering rate hike concerns, and continued supply recovery clashed with a destocking trend that is hard to reverse in the short term.

Amid this tug-of-war between longs and shorts, aluminium prices are expected to consolidate in the near term. The most-traded SHFE aluminium contract is expected to trade in a range of RMB 22,500-23,500 per tonne next week, while LME aluminium is expected to trade at USD 3,050-3,250 per tonne.

Looking ahead, close attention should be paid to Middle East production resumption progress and geopolitical conflict trajectory, LME aluminium ingot inventory changes, and China’s downstream processing orders and aluminium semis export data.

Note: This article has been issued by SMM and has been published by AL Circle with its original information without any modifications or edits to the core subject/data.

Responses