您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The images has been sourced from: https://news.metal.com/

Futures market: In May, the most-traded cast aluminium alloy contract swung wildly with its price centre moving lower. It traded in the range of RMB 22,800-23,800 per tonne throughout the month, repeatedly retreated after rapid rises, and bottomed out, failing to form a one-sided trend. Moving averages gradually converged, and the contract remained range-bound overall.

{alcircleadd}Spot market: At the start of the month, dragged by the Labour Day holiday and the off-season, ADC12 prices came under pressure and fell. In the middle and latter parts of the month, persistently tightening policies reinforced expectations for raw material shortages and production cuts, strengthening support at lower levels. Spot prices moved sideways around RMB 23,700 per tonne. The price centre shifted higher in June. As of June 5, SMM ADC12 was quoted at RMB 23,900 per tonne, up RMB 100 per tonne from the beginning of May.

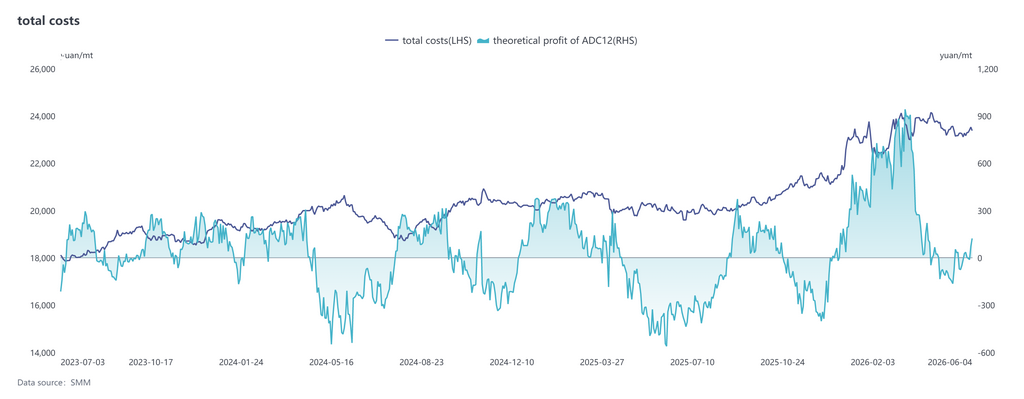

Cost side, according to the latest SMM data, the total theoretical cost of the ADC12 industry from January to May 2026 increased by 14.0 percentage points from 2025 to RMB 23,305 per tonne.

By component, aluminium scrap cost was approximately RMB 21,070 per tonne, accounting for 90.4 per cent; copper cost was RMB 836 per tonne, 3.6 per cent; and silicon cost was RMB 475 per tonne, 2.1 per cent. The cost shares of aluminium scrap and copper continued to rise, while the cost of silicon continued its pullback.

Since May, the raw material side overall has remained tight, serving as the core factor supporting the market. Although aluminium scrap prices fluctuated with aluminium prices, the actual decline was limited by suppliers holding back from selling. Ex-China aluminium scrap prices stayed high, keeping the import window shut for an extended period and significantly weakening its supplementary role to the Chinese market.

At the same time, regulation of the 'invoice-based economy' continued to tighten, making it increasingly difficult to obtain input invoices. Enterprises' tax burdens and compliance costs were passively pushed up, causing the industry's theoretical profit to invert. The tight supply of invoices and stricter compliance oversight are unlikely to ease in the short term. Procurement costs for aluminium scrap and tax burdens are expected to remain high in June.

Demand side, in May, the market continued to exhibit off-season characteristics. Orders from downstream die-casting enterprises remained sluggish, procurement was mainly based on rigid demand and small batches, and the willingness to rush to buy amid rising prices was insufficient, keeping market trading activity low throughout. End-use consumption saw little substantial improvement, with the demand side continuously suppressing the upside room for prices.

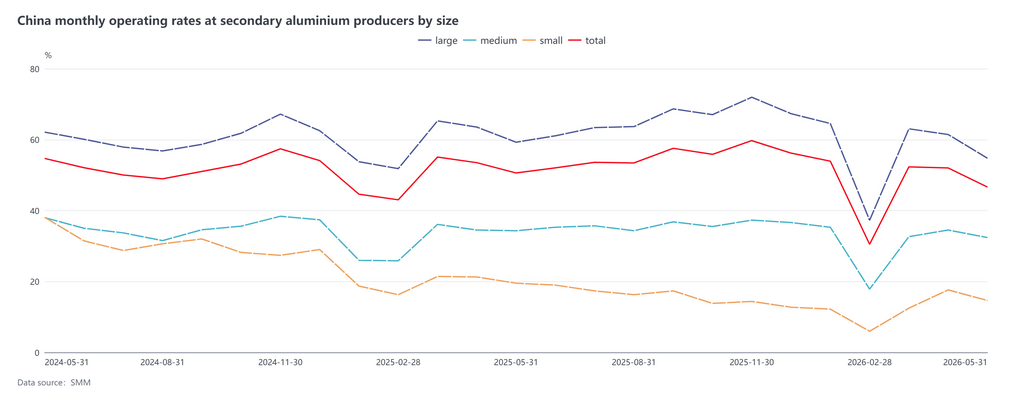

Supply side, in May, the operating rate of the secondary aluminium alloy industry was 46.6 per cent, down 5.4 percentage points M-o-M and down 4.0 percentage points YoY. Enterprise production generally shrank, mainly due to two bearish factors. First, the Labour Day holiday combined with weakening end-use demand led to shrinking orders. Second, tighter regulations on "reverse invoicing" raised the compliance cost of aluminium scrap recycling, making supplies with invoices tight, and enterprises faced the dilemma of "invoice shortages" and losses. The operating rate in June is expected to continue its downtrend, mainly constrained by weakening demand in the off-season and elevated policy compliance costs.

Entering June, secondary aluminium alloy prices will remain generally stable with a slight rise. On the cost side, tight invoice supply and stricter compliance supervision are unlikely to ease significantly in the short term, and enterprise tax burden costs are expected to stay high.

On the supply side, if the shortage of invoices and tight raw material supply continue to intensify, the scope of production cuts in the industry will further expand. Coupled with the continued closure of the import window, the tight spot supply pattern is expected to persist, providing strong support for prices. On the demand side, the off-season pattern continues, with downstream dominated by just-in-time procurement, leaving insufficient upward momentum.

However, supply tightening offsets the off-season pressure, limiting the downside room for prices. Overall, the price centre of ADC12 in June is expected to rise compared with May, showing a generally stable trend with a slight rise and a range-bound trend.

Going forward, close attention should be paid to changes in compliant raw material supply, the implementation of production cuts in the industry, and the pace of end-use demand recovery.

Note: This article has been issued by SMM and has been published by AL Circle with its original information without any modifications or edits to the core subject/data.

Responses