您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

This image has been obtained from Mysteel

In the first half of 2026, China's domestic alumina production rose 5.6 per cent Y-o-Y to 45.9 million tonnes, with capacity up 8.2 per cent to 120.95 million tonnes per year. June saw a 258,000 supply deficit in the southwest, covered by northern shipments. In the second half, supply tightness is expected to ease as capacity in Guangxi ramps up and southern-to-northern flows continue. Demand from aluminium smelters is set to stay stable.

{alcircleadd}Therefore, the alumina prices are expected to trend lower in a RMB 2,500-3,000 per tonne range, with seasonal factors like winter heating and environmental checks offering possible intermittent support.

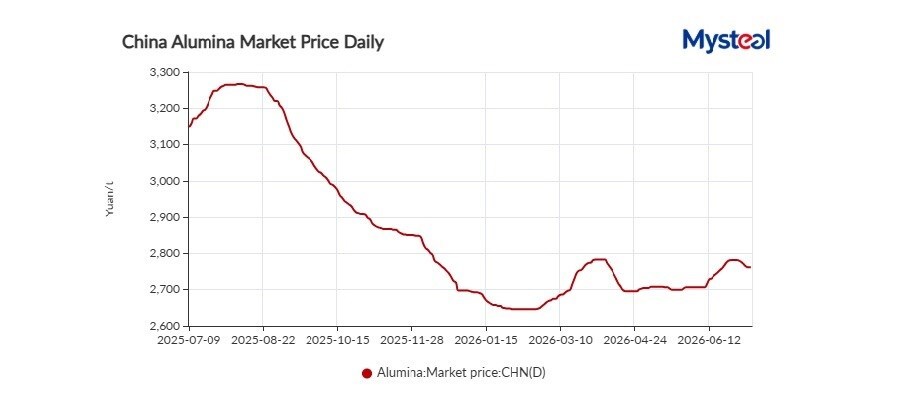

H1 2026 China alumina market overview

Alumina price trends in China

In the first half of 2026, China's domestic alumina prices traded in a narrow range, with the spot prices averaged at RMB 2,697 per tonne, down 21.69 per cent year-on-year. Price movements were shaped by distinct phases.

In early Q1, prices moved lower as some alumina refineries curtailed the production under financial pressure, though most reductions were routine maintenance or flexible production adjustments. As the Chinese New Year approached, downstream aluminium smelters largely completed their stockpiling, and alumina refineries cleared inventories ahead of the holiday.

Spot availability temporarily tightened, but stocks remained high at railway stations, exchange warehouses, and aluminium smelters. After the holiday, the traders became more willing to sell for destocking purpose.

A modest price rebound emerged in late Q1, driven by a sudden production cut at a major alumina refinery in northern China, which created a temporary regional supply tightness and prompted procurement from aluminium smelters in Northeast China. However, the price gains proved short-lived, and the market lacked strong upward momentum once it returned to a more rational footing.

In Q2, earlier production cuts by some alumina refineries in both the north and south China driven by operational or cost pressures shifted the market from apparent surplus to a phase of tight balance. Meanwhile, new capacity in Guangxi accelerated its ramp-up, leveraging coastal logistics advantages.

In early April, alumina futures price led a decline, with some traders selling at low prices to avoid inventory build-ups, dragging spot prices lower. Later in the month, a sudden output cut at a major alumina refinery in southern China tightened supply, helping the prices to stabilise.

In late Q2, market sentiment was lifted by reports that Guinea, the world's largest bauxite producer, was planning to introduce export controls in June 2026 through a quota system. This triggered a sharp rally in alumina futures, and spot prices followed modestly higher after a period of consolidation, with additional support from news of another output cut at a large refinery in Shanxi. High-priced transactions began to emerge, and spot prices diverged into a "steady in south, firm in north" pattern based on local supply-demand dynamics.

Unlock key insights from leading companies and experts across the aluminium ecosystem with our e-Magazine - Mine to Market: ALuminium Producers & Manufacturers 2026

Overseas alumina price trends

Overseas alumina prices remained relatively stable through the first half. By end-June, Australia's FOB prices stood at USD 330 per tonne, down 8.31 per cent year-on-year.

In late Q1, drone strikes targeted production facilities at Emirates Global Aluminium's Al Taweelah smelter and Bahrain's Alba, damaging equipment and adding to operational uncertainty. Both are key Middle Eastern smelters, with annual capacities of 1.6 million tonnes and 1.623 million tonnes, respectively, and their disruptions carry meaningful global supply implications.

At the same time, Qatar Aluminium suspended output due to natural gas shortages, Alba implemented controlled safety shutdowns on three lines, and Mozambique's Mozal smelter entered maintenance. Given the long lead times required to restart aluminium smelters, these production cuts point to weaker overseas alumina demand for at least the next six months.

In Q2, the closure of the Strait of Hormuz continued to disrupt shipping routes, creating delivery difficulties for alumina cargoes headed to the Middle East. Weaker demand from Middle Eastern smelters also led some to re-sell alumina feedstock, with some Australian cargoes originally destined for the Middle East redirected to China and India.

Cost and margin trends in China

Alumina production costs have risen entering 2026, and the industry continues to face sustained losses. As of end-May, the weighted average full cost of alumina production in China stood at RMB 2,849.45 per tonne, down slightly by RMB 2.88 per tonne month-on-month. The average industry margin was negative at RMB -151.45 per tonne, a decline of RMB 21.12 per tonne from the previous month.

Domestic supply-side fluctuations remained limited in May 2026. However, the recovery of a large alumina refinery in Guangxi fell short of expectations, keeping spot prices relatively firm. That said, with traders' inventories continuing to build and new capacity gradually ramping up, there was limited room for a significant price rally.

Alumina capacity and production

China's alumina capacity continued to expand in the first half of 2026. By end-June, total installed capacity stood at 120.95 million tonnes per year, up 8.23 per cent year-on-year, with operating capacity at 92.60 million tonnes per year, up 2.89 per cent.

January-June 2026 production totalled 45.916 million tonnes, up 5.58 per cent year-on-year. June output read 7.616 million tonnes, down 2.13 per cent month-on-month but up 3.89 per cent year-on-year.

Imports and exports

In May, China imported 438,500 tonnes of alumina, down 28.11 per cent month-on-month but up 549.63 per cent year-on-year. Exports totalled 283,300 tonnes, down 45.19 per cent month-on-month but up 36.33 per cent year-on-year, resulting in net imports of 155,200 tonnes (+66.70 per cent month-on-month, -210.62 per cent year-on-year). January-May cumulative imports reached 1.8282 million tonnes (+994.74 per cent Y-o-Y), exports 1.3437 million tonnes (+14.62 per cent Y-o-Y), and net imports 484,600 tonnes (+148.20 per cent Y-o-Y).

May imports fell sharply. Major sources included Australia, Indonesia, and India, with Australian volumes halving month-on-month to 278,300 tonnes. Exports continued to flow to Russia, Oman, and the UAE.

New Capacity

As of end-June, new alumina capacity in China reached 5.4 million tonnes per year, with a further 2.0 million tonnes expected in the second half. Guangxi has been the main driver of domestic capacity growth, with three new projects reaching full production in the first half.

Inventories

By July 2, 2026, traders' alumina inventories stood at 6.306 million tonnes, up 46,000 tonnes week-on-week. Faster commissioning and restarts in Guangxi, together with regional price spreads, opened the arbitrage window for shipping from southern China to the northern regions, increasing port and in-transit inventories.

Meanwhile, futures prices corrected, and spot offers edged down recently. Despite generally thin trading activity, some downstream aluminium smelters showed increased interest in inquiries and procurement, leading to a modest build in raw material inventories at aluminium smelters.

Supply-Demand Balance

June's domestic alumina market remained in a tight balance. According to Mysteel's survey, alumina output in Southwest China reported 1.892 million tonnes in June, leaving a regional supply shortage of 258,000 tonnes. The market relied on cross-regional shipments from the north to fill this deficit. But more recently, as new capacity comes online and maintenance restarts accelerate, the supply-demand balance in the southwest is expected to shift from tight to surplus.

In northern regions, production remained volatile due to policy, environmental, and cost factors, keeping spot supply relatively tight and prompting downstream aluminium smelters to source from outside the region. If the price spread between Guangxi and northern markets continues to exceed RMB 80 per tonne, southern cargoes will likely keep flowing north.

H2 2026 China Alumina Market Outlook

Alumina Supply

At end-June, China's operating alumina capacity reported around 94.20 million tonnes per year. An alumina refinery Shanxi halted the feed input due to red mud disposal issues, leaving only small amounts of inventory to supply captive downstream plants, involving a capacity of around 2.0 million tonnes per year. Market speculation points to a possible partial restart, but this remains unconfirmed. A refinery in Henan started a 10-day calciner maintenance, taking out around 1.1 million tonnes per year capacity.

A large refinery in Guangxi, previously offline for line commissioning, has brought one boiler back online and may reach 3.0 million tonnes per year, with another line expected by end-July. Two new refineries in Guangxi have produced first product from their second lines, with ramp-up expected by mid-July, with a combined capacity of 2.2 million tonnes per year. A refinery in Guizhou is running at around 700,000 tonnes per year post-restart and is expected to stay at that level for now.

Demand

Domestic aluminium smelting capacity is stable at around 45.26 million tonnes per year. Smelters are operating steadily with limited month-on-month changes, with some maintaining routine procurement.

Conclusion

Over the past two months, sudden production cuts in both northern and southern regions, combined with large inventory builds at exchange warehouses and traders' storage, have tightened spot alumina availability. The market remains in a tight balance, with downstream smelters stepping up inquiries, reinforcing sellers' reluctance to sell and supporting spot prices. However, alumina prices recently kicked off the downward track amidst macro headwinds and Guinea failing to introduce export control as market had expected. Therefore, with new and restarted capacity in Guangxi gradually ramping up and regional price spreads widening to encourage southern-to-northern flows, alumina prices are expected to trend lower in the second half. That said, seasonal factors such as winter heating demand, mine inspections, environmental protection inspections, and widening industry losses could create phased upside. Alumina prices are expected to trade in a range of RMB 2,500-3,000 per tonne.

Explore- Most comprehensive and forward-looking industry-focused report — Global Bauxite & Alumina Market Forecast to 2036: Supply–Demand, Trade Flows & Price Outlook

Note: This news is published under a content and exchange agreement with Mysteel

Responses