您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

This image has been sourced from https://www.mysteel.net/

From tightness to oversupply in southwest China

{alcircleadd}At the beginning of the year, the commissioning progress of new alumina projects in Guangxi fell short of expectations, compounded by temporary production cuts at several alumina plants in the southwest region, leading to persistently tight spot supply in the area. With this year's new alumina capacity primarily concentrated in Guangxi, the gradual ramp-up and release of these new capacities have recently eased the tight spot conditions in the southwest, resulting in a slight rebound in raw material inventories among downstream aluminium smelters in the region.

According to Mysteel's survey, as of the end of June 2026, total alumina output in the southwest region reached approximately 1.892 million tonnes, with a regional supply-demand gap of 258,000 tonnes. The market currently relies heavily on cross-regional shipments from the north to bridge this supply shortfall. Subsequently, along with the commissioning of new capacities and the resumption of maintenance-halted facilities, the alumina supply-demand landscape in the southwest will likely shift from tightness to a state of oversupply. It is projected that the total surplus of alumina in the region will exceed 2 million tonnes in the third and fourth quarters combined.

The fragility of the northern supply

Staying on the other end along the trend of shipping from south to north are alumina plants in the northern regions (such as Shanxi, Henan, and Shandong), which have been facing severe rigid constraints. This is fundamentally why their production fluctuates significantly and spot supply remains relatively tight.

The biggest constraint comes from the policy end. According to the High-Quality Development Implementation Plan for the Aluminum Industry (2025-2027) and the Action Plan for Continuous Improvement of Air Quality, no new capacity for aluminium or alumina will be added in key air pollution prevention and control areas, such as the Beijing-Tianjin-Hebei region and the Fenwei Plain. Most major alumina-producing areas in northern China fall under these restricted zones, bringing new project construction to a near standstill.

Meanwhile, energy efficiency for new, modified, or expanded projects must meet the advanced values of mandatory energy consumption quota standards, and environmental performance must reach Grade A. Some older capacities in the north face renovation or elimination for failing to meet these standards, and inefficient capacities will be phased out during the industry reshuffle.

Concerning environmental protection side, during the northern heating season, summer peak electricity periods, and major events, environmental inspections are frequent. Alumina plants in Shanxi and Henan often face phased production halts or restrictions under heavy pollution weather warnings, with the calcination process being a key control point. In June 2026, Shanxi launched a special safety inspection for non-coal mines and red mud reservoirs, leading to phased production cuts or halts affecting approximately 2 million tonnes of operating capacity.

Furthermore, standards for red mud storage and tailings management continue to escalate. Environmental protection investments for small and medium-sized alumina enterprises have increased substantially; some small-capacity plants lacking supporting red mud disposal sites maintain low operating rates in the long term, further compressing effective supply.

Explore: The most comprehensive and forward-looking industry-focused report – Global Bauxite & Alumina Market Forecast to 2036: Supply–Demand, Trade Flows & Price Outlook

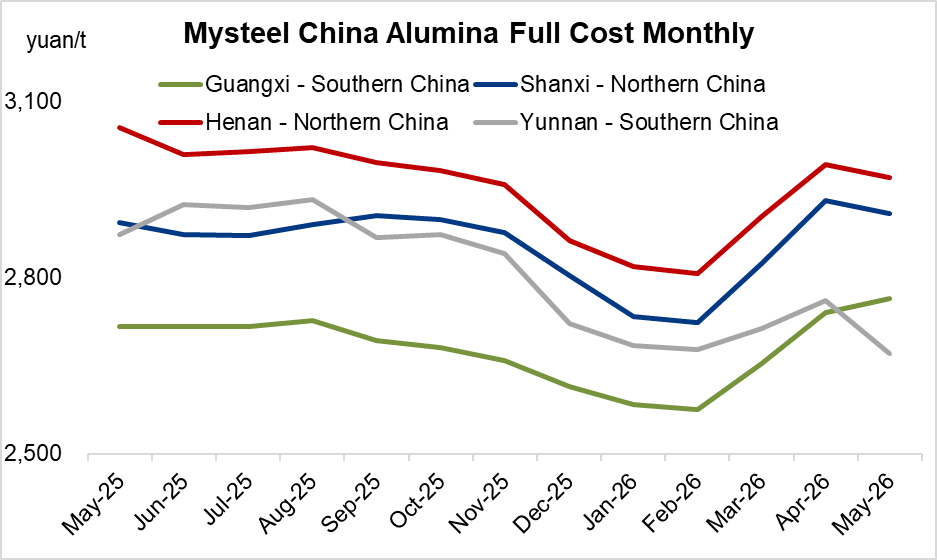

On the cost end, compared to coastal plants in Guangxi that benefit from direct port unloading, inland plants in northern China require long-distance road transport or multiple transshipments for imported ore, resulting in high logistics costs. Currently, the weighted total cost of alumina in Shanxi and Henan is approximately RMB 2,900-3,000 per tonne, higher than both the industry average and low-cost coastal capacities. During price downturn cycles, these plants easily fall into negative cash flow, forcing them to proactively suppress production or conduct maintenance.

The trend of shipping from south to north

Cross-regional transportation is driven not only by regional supply-demand dynamics but also requires a comprehensive analysis of regional price spreads and logistics costs.

According to Mysteel research statistics, freight from Baise to Yunnan is RMB 80-100 per tonne lower than from Beihai. Assuming stable delivered prices at downstream consumption sites, the implied ex-factory price range for Guangxi coastal alumina plants is RMB 2,580-2,600 per tonne.

Freight from Baise to Guizhou is RMB 40-50 per tonne lower than from Beihai, corresponding to an ex-factory price of RMB 2,630-2,640 per tonne for Guangxi coastal enterprises. Freight from Shandong to eastern Inner Mongolia is RMB 20-30 per tonne lower than from Fangchenggang. Aluminium smelters in Inner Mongolia execute procurement prices with reference to the average market prices in Shanxi and Shandong, which translates to an ex-factory price of RMB 2,660-2,670 per tonne for Beihai alumina plants.

Based on a comprehensive comparison of regional price spreads, from the seller's perspective, the profit per tonne for current Guangxi coastal alumina plants selling to the northern market is RMB 30-80 per tonne higher than selling in the southern market.

Looking at the cost curve, coastal alumina plants in Guangxi leverage the low-cost advantage of imported bauxite (Guinean ore) and port logistics convenience, making their total costs lower than those of high-cost inland northern capacities (in Shanxi and Henan).

Therefore, the trend of shipping alumina from south to north has recently taken hold, and the volume of cross-regional transportation is showing an increasing trend.

Explore our e-magazine ALuminium LeaderSpeak 2026 for the latest industry insights and trends

Conclusion

In summary, the alumina supply in the southwest region is gradually trending towards oversupply.

Conversely, due to the impact of policies, environmental regulations, and cost factors, production fluctuations at northern alumina plants are significant, leading to relatively tight overall spot supply in the north. Downstream aluminium smelters in the north have a demand for cross-regional procurement to replenish their inventories.

If the price spread between Guangxi and the northern region exceeds RMB 80 per tonne in the future, southern supplies may continuously flow into the northern market.

Note: This article has been issued by MySteel and has been published by AL Circle with its original information without any modifications or edits to the core subject/data.

Responses