您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

United States tariffs on aluminium imports had a great effect on the country’s domestic aluminium industry, said Andy Home, Senior Metals Columnist at Thomson Reuters, at the London Metal Exchange Week 2019.

As the US import duties came into effect on the national security grounds in early 2018, the US Midwest premium, which overlays the LME cash price, expanded from 10 cents per pound to 22 cents per pound. The premium later eased to 18 cents per pound, though much higher than levels seen before the imposition of the tariffs.

{alcircleadd}This hike in prices was primarily because of the disruption in supply chain, both primary aluminium and semi-finished, as a result of lesser imports due to tariffs.

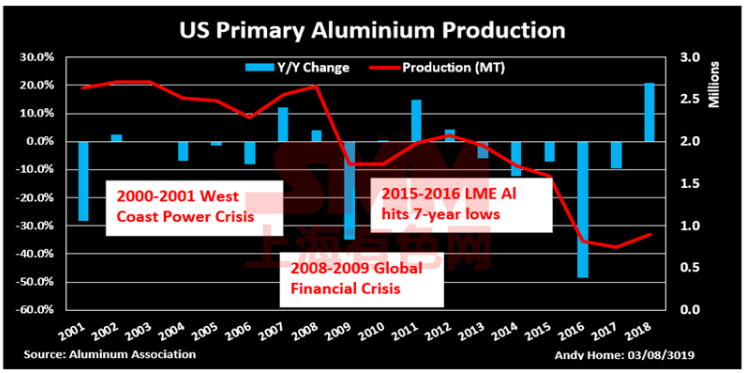

However, the above graph indicates that the steel and aluminium import tariffs in 2018 had no impact on the US aluminium production. After plunging from 2008 to 2017, the US aluminium output grew through 2018 and continuing until now.

The Aluminium Association, in cooperation with the Aluminium Association of Canada, showed the U.S. produced 568,110 tonnes of aluminium in the first half of 2019, up 40 per cent from 404,671 tonnes produced in H1 2018. Also, in the last month, the United States’ aluminium output stood at 90,316 tonnes after increasing 18 per cent from 76,578 tonnes year-on-year.

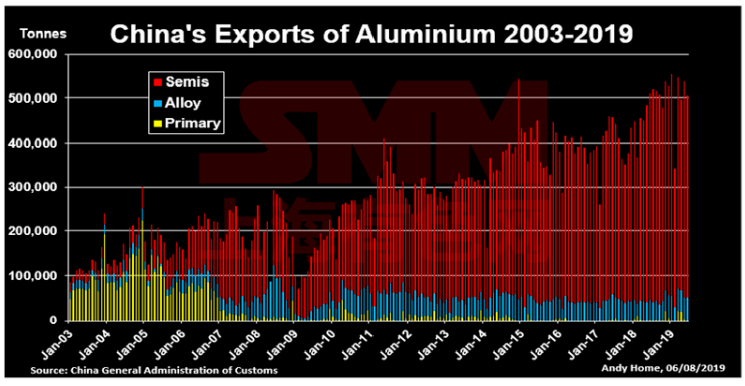

The aluminium industry in China saw a prosperous growth, pointed out Andy Home. China’s aluminium production accounted for 57% of the global total in 2018, up from a rate of 17% in 2002. Also, its aluminium alloy and semi exports remained unaffected, as shown in the graph below.

Meanwhile, Ian Roper, general manager of SMM Singapore, pointed out at the LME Week 2019 that the daily primary aluminium production in China plunged through the second half of 2018 and also the entire 2019. This could be primarily attributed to the idled capacity of the smelters and slower recovery of the closed ones due to high input costs. This, as a whole, lifted the primary aluminium price in return.

Responses