您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

Sluggish trading ahead of the Chinese New Year holiday next week is keeping the Chinese market passive and there is no such significant movement in the prices of commodities and the raw materials.

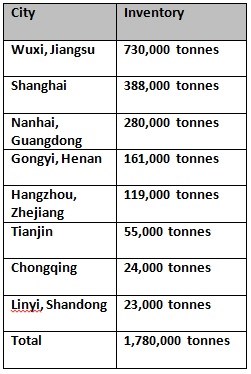

According to Shanghai Metals Market, China’s social inventory of refined aluminium including SHFE warrants stood at 1.78 million tonnes SMM on Thursday February 8, up 17,000 tonnes from a week ago due to buyers’ unwillingness to invest.

{alcircleadd}The inventory status in the major Chinese cities is as follows:

SHFE aluminium is expected to get stronger with the approaching of Chinese New Year holiday. The contract outperformed its nonferrous peers yesterday, registering a 0.28% increase. SMM believes this is mostly due to investors pricing in the weak fundamentals of aluminium much earlier on.

Some smelters in Henan province have said they planned to delay the restarts after the winter heating season ends on March 15 due to the losses for low aluminium prices. SMM expects SHFE aluminium to stay rather firm before the Chinese New Year holiday next week as investors continued to square their positions.

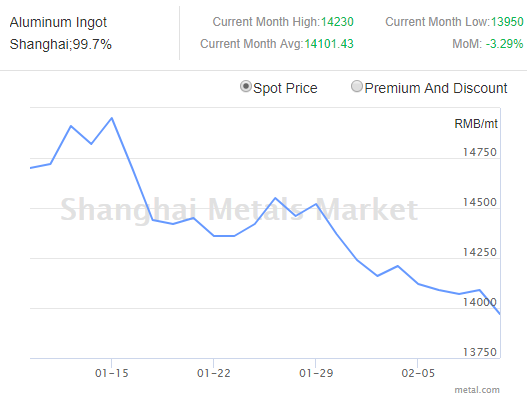

After Yesterday’s slight gain average Aluminum Ingot prices dropped RMB 120 per tonne today to stand at RMB 13,970 per tonne. The prices are expected to move within a range of RMB 13,950-13,990. Spot discount will range within RMB 140-100 per tonne today. Average A00 ingot prices saw the biggest drop in the East China market at RMB 170 per tonne.

Post holidays, however, prices would still fall as aluminium supply would ramp up, even if at a slower pace. However downward movement is expected to prevail in the short term as the domestic aluminium demand is set to be increased fast after the winter heating season, when industrial activities restart with a boom.

On the cost front, SMM expects alumina prices and prebaked anode prices to go down due to lower electricity prices.

Responses