您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

Orazio Zoccolan is presently serving Assomet, the Italian non-ferrous metals industries association, as a General Manager. He was born in Milan in 1960, and graduated in Political Science at the University of Milan. He started his career working for the Italian recycling aluminium association in 1989. He joined Assomet as an environmental manager in 1997 became a General Manager in 2020, after being a Secretary General of Centroal (aluminium group within Assomet) in 2012.

Besides, he is a member of the Board of Directors of IGQ – certification body, Qualital Servizi – aluminium surface treatment certification body, and Gas Intensive Consortium.

We are delighted to have him with us and know his views and opinions on the current European aluminium industry. To know in details, please continue to read the article.

One fact is certain: in this difficult context, the aluminium industry has been able to adapt and immediately identify viable solutions as well as prepare for the upcoming challenges in the short and medium term.

We have been fighting Covid and its devastating effects off and on for the last two and half years, facing an absolutely unprecedented situation and its diverse implications.

Subsequently, already at the beginning of 2021, when there were clear signs of recovery for our sector as well as for downstream manufacturing, we had to face yet further problems related to the increase in the costs of energy and raw materials. And to all this we should add that in a European Union, which among the main macro-areas, was the most affected, as indicated by the depreciation of the euro and the heavy losses of the stock exchanges that occurred at the beginning of the Ukraine conflict.

The rise in the prices of raw materials, brought about by a plurality of factors resulting from the pandemic, drops in production, reduction in stocks, difficulties in the logistics sector and the monetary and fiscal policy choises of some countries - as well as a new surge of the demand, should be poised to "stabilize" to values lower than the highs recently achieved. And we would still be on higher levels than a year ago. Stabilization and reduction of volatility clearly appear key to allowing us to act on more predictable scenarios, such as the adoption of adequate industrial planning.

With regard to energy, however, it is now essential to carefully manage the diversification of supply sources, in order to free ourselves from any reliance on Moscow, as also shown by the REPowerEU strategy recently presented at EU level.

Moving on to the field of commercial policy, it is necessary to emphasize the results obtained in the context of anti-dumping duties on semi-finished aluminium products. The duty "protection" on extrusions has been in effect for a year now, while as regards flat rolled products, the suspension of similar measures will soon expire and this will allow EU producers a better use of their capacity. Another aspect that has engaged the association is the so-called CBAM (Carbon Border Adjustment Mechanism). This is the carbon adjustment mechanism at the borders, through which it is intended to reduce the risk of leakage of emissions by applying a cost on imports that reflects the carbon content of imported products. As initially conceived, it involves some serious shortcomings which risk harming rather than helping the European industry.

Another topic of particular importance we are facing is the revision of the WSR (Waste Shipment Regulation), whose objective is to set adequate limits on the export of metal scrap from the EU to countries that, from an environmental and emissions perspective, do not offer the guarantees of the same treatment as the of European competitors.

The Italian Aluminium industry

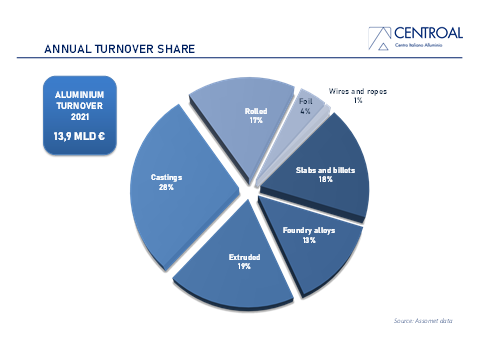

The aluminium industry in Italy is an important player in the production value chain. About 500 factories process aluminium supplying materials for the automotive, packaging and construction industries. It employs more than 15,000 people and had a turnover of 13.9 billion euros in 2021.

The Italian Alu data

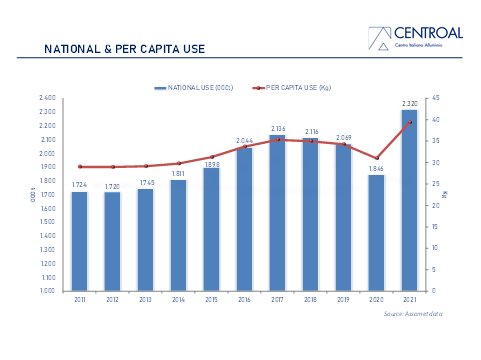

The turnover of 2021 recorded a strong increase of 51% to 14 billion euros; this growth is due both to the increase in production recorded in all sectors, and to the increase in metal price. As for last year, castings reached the highest turnover share (28%), followed by extrusions (19%), slabs and billets (18%) and rolled products (17%). This is followed by the foundry alloys products (13%), foils (4%) and drawn products (1%) sectors. The national use of aluminium, in 2021, stood at 2.3 million tonnes.

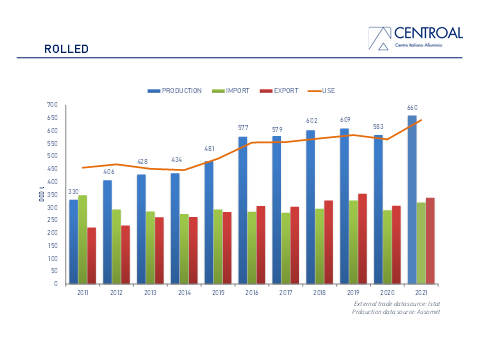

The national production of rolled products showed a growth of 13.2% compared to 2020, with approximately 660 thousand tonnes produced. Imports increased by 10.4% (319 thousand tonnes) and exports by 10.2% (337 thousand tonnes), bringing consumption to an increase of 13.4%. The data on the indexes of domestic orders show a stable trend for the first two months of 2022 as opposed to the foreign ones which decreased compared to January and February 2020 and 2021.

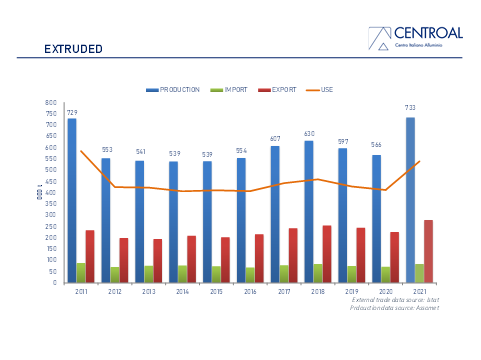

The production of extrusions, on the other hand, had a spike as regards production (+ 29.4%) with 733 thousand tonnes produced. Imports and exports also recorded an increase, respectively + 18.3% (84 thousand tonnes) and + 23.5% (278 thousand tonnes); the national consumption therefore stands at + 30.8%. With regard to orders in the first two months of 2022, both domestic and foreign orders have increased compared to the previous two years.

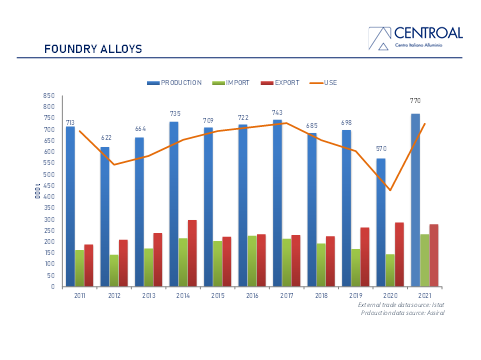

Finally, the sector of foundry alloys also recorded a very strong increase in national production (+ 34.9%) with 770 thousand tonnes produced. Imports also recorded a rise of + 60.9% compared to 2020 (233 thousand tonnes), while exports suffered a slight drop of -2.9%; by combining the data, a consumption of 725 thousand tonnes is obtained, or + 69.9% compared to last year.

On the other hand, as regards Istat/Eurostat data, in Italy, imports increased in all sectors, especially in that of slabs and billets (+ 30%) and raw aluminium alloys (+ 45%); also at a European level there was a clear increase in slabs and billets (+ 32.5%) and in bars and profiles (+ 23%) while imports of ingots of not alloyed aluminium (-4.8%) and foil (- 9.8%).

The current situation is definitely marked by the conflict unleashed by the Russian invasion of Ukraine. Orders have contracted, but despite this and despite the worrying levels reached by the cost of energy, the general situation is still, overall, positive. The global order book is still at sustained levels and downstream users, with the sole exception of the automotive sector which still suffers from a shortage in the supply of components, continue to work at a good pace.

..............................

Assomet represents the Italian producers of non-ferrous metals and semi-finished products of aluminium, lead, copper, zinc and precious metals. Overall, the industrial sector is represented by a thousand companies that employ 26 thousand people with an annual turnover of approximately 28 billion euros.

There are about a hundred directly associated companies.

Founded in 1946, it is a member of Confindustria, the confederation of Italian industries.

Responses