您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The US dollar index hit a three-week low to around 93.9 and closed at 94 last Friday night. This was 0.52% lower from a week ago, marking the biggest loss in four weeks. LME base metals felt downward pressure on escalated tension between China and the US.

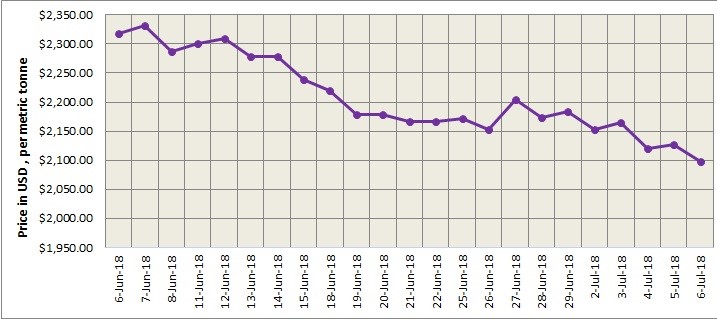

LME aluminium dipped slightly and closed at US$ 2098.50 per tonne on Friday July 6 from US$ 2127 per tonne on previous closing. It dipped further at a slower pace last Friday night as it rebounded from a low of US$2,071 per tonne on weakened US dollar. With pressure at the five-day moving average, it closed at US$2,086.5 per tonne after night trading and is expected to trade at a range of US$2,075-2,095 per tonne today.

{alcircleadd}

As on July 6, LME aluminium cash (bid) price stands at US$ 2098 per tonne, LME official settlement price stands at US$ 2098.50 per tonne; 3-months bid price stands at US$ 2071 per tonne, 3-months offer price is US$ 2072 per tonne; Dec 19 bid price stands at US$ 2110 per tonne, and Dec 19 offer price stands at US$ 2115 per tonne.

The LME aluminium opening stock dropped to 1105975 tonnes. Live Warrants totalled at 920425 tonnes, and Cancelled Warrants were 185550 tonne.

LME aluminium 3-months Asian Reference Price is hovering at US$ 2078.35 per tonne.

SME and SHFE Aluminium Price Trend

The benchmark aluminium price on Shanghai Metal Exchange increased to US$ 2116 per tonne on July 9 from US$ 2091 per tonne on July 6.

With support from alumina production cuts in Shanxi and Henan provinces, the SHFE 1809 contract traded rangebound during Friday. The SHFE 1809 contract rose to a high of RMB 14,130 per tonne today morning as longs added their positions after digesting the US-China trade tariffs. It closed at RMB 14,120 per tonne with resistance at the 10-day moving average. The contract is expected to trade at RMB 14,050-14,200 per tonne today, with spot discount at RMB 40-0 per tonne.

SMM expects the contract to hold steady or to see a smaller decline this week, with the alumina production cuts and bauxite shortages n Shanxi and Henan. There is limited potential for a rebound as the US-China trade war continued to weigh on market sentiment. The contract is likely to struggle around the five- and 10-day moving averages this week.

Key factors to watch today include China's economic data in June and the Eurozone Sentix investor confidence index in July.

Responses