您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

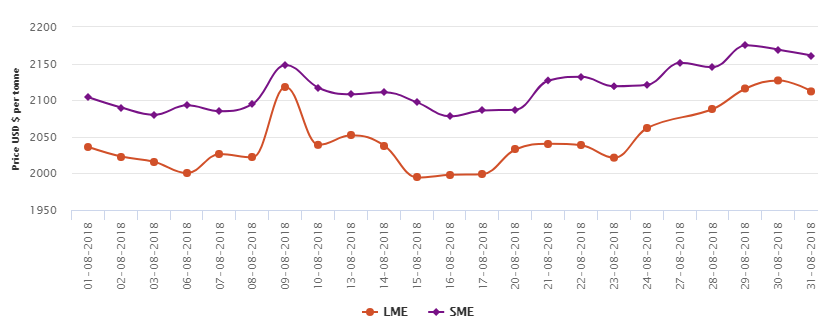

The last week of August was marked by a falling US dollar index and a rising LME aluminium graph. August 27 was a holiday for LME and it started the week with a 1.26 % gain on August 28. The light aluminium contract traded within a range of US$ 2088 to US$ 2112 per tonne over the week. US dollar rebounded for the first time in five trading days on Friday August 31 and pushed the LME slightly lower. LME aluminium and SHFE contracts registered smaller drops compared with other base metals when the US dollar rebounded overnight.

The benchmark aluminium price on Shanghai Metal Exchange started the week at US$ 2151 per tonne on August 27 and after reaching the height of US$ 2175 per tonne mid-week, the week was closed at US$ 2161 per tonne on August 31.

As on August 31, LME aluminium cash (bid) price stands at US$ 2111.50 per tonne, LME official settlement price stands at US$ 2112 per tonne; 3-months bid price stands at US$ 2137 per tonne, 3-months offer price is US$ 2139 per tonne; Dec 19 bid price stands at US$ 2175 per tonne, and Dec 19 offer price stands at US$ 2180 per tonne.

The LME aluminium opening stock dropped to 1070750 tonnes. Live Warrants totalled at 780750 tonnes, and Cancelled Warrants were 290000 tonne.

LME aluminium 3-months Asian Reference Price is hovering at US$ 2139.29 per tonne.

The US dollar index slumped to the lowest in four weeks in the last week of August, as investors lost confidence in the dollar after the US and Mexico reached a preliminary agreement to change parts of the North American Free Trade Agreement (NAFTA). Short supplies of alumina overseas provided support to LME and SHFE aluminium. Alcoa’s and South32’s alumina refineries in Western Australia (WA) have delayed their shipments and workers continued their strike at Alcoa refinery plants and bauxite mines in WA. Meanwhile, maintenance at South32’s Worsley alumina refinery in WA affected output by some 200,000 tonnes. All these factors put pressure on the alumina market. Cost support is likely to continue in the short term, and Shanghai Metals Market expects the contracts to continue its strong and rangebound pattern in the long term.

Shanghai Metals Market research showed that China shut 730,000 tonnes of primary aluminium capacities during June-August because of high costs and relatively low prices of aluminium. A00 aluminium ingot prices in China dipped on gaining inventories due to increasing supplies and weak consumption. The prices are expected to stay rangebound next week.

Responses