您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The use of downstream aluminium products has been seeing a potential growth over the years, driven by the automotive and packaging industries. Automakers’ focus on making lightweight, fuel-efficient vehicles has been lending a further boost to it, resulting in many new investments and expansions in the industry. But in some parts of the world, the growth in demand remained slow, attributing to the global economic downturn. Let us here take a quick view to the downstream aluminium products demand trend in the past year.

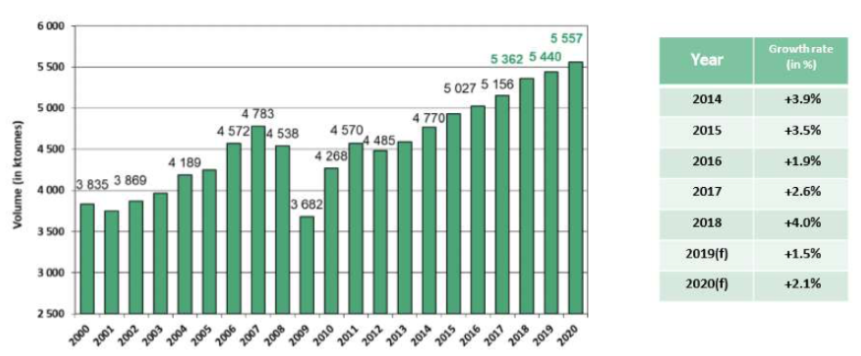

Global downstream aluminium demand

{alcircleadd}Europe in 2019 saw a 1.5 per cent growth in aluminium flat-rolled aluminium products, said Mr Catsaros at International Aluminium 2019 Conference. Demand hovered at 5.4 million tonnes, which is expected to increase to 5.5 million tonnes in 2020, he noted. On the other hand, auto body sheet (ABS) demand is estimated to rise to 1.5 million tonnes by 2023, at a CAGR growth of 5 per cent.

In the September quarter, the demand for European aluminium foil rolls went down by 2.2 per cent to 228,685 tonnes with year to date figures, while the production remained unchanged at 714,251 tonnes, showed the data from the European Aluminium Foil Association (EAFA).

In North America, in the first quarter of 2019, the demand for aluminium downstream products was up by 2.1 per cent. While the US government granted about 80% of exemption requests for Japanese aluminium products, Kobe Steel and UACJ ramped up local production there in light of other factors, such as transportation costs. UACJ expects its U.S. output of automotive aluminium sheet to exceed 1 million tons in 2020, up about 50% from 2017 levels.

China’s flat rolled current production during October 2019 was approximately at around 11 million tonnes per year, while capacity exceeded 20 million tonnes. Some 8 million tonnes used to be consumed locally, while the remainder exported. By 2023, China’s capacity is expected to reach 23 million tonnes per year, said Mr Catsaros at the conference.

India in future is expected to shape up into one of the leading aluminium consumption hubs, as the latter is estimated to inch up to 7.2 million tonne in the next five years. So, the key aluminium players of the country are being suggested to focus on the development of the downstream sector to meet the growing domestic demand and curb increasing imports, as a result of a lax tax structure on downstream imports. The downstream aluminium products invite import duty of 7.5 per cent, against 20-30 per cent in Southeast Asian nations having free trade agreements (FTAs) with India. That apart, China, in a bid to incentivise its secondary manufacturers, provides an export incentive of 16 per cent.

Let us now look at the downstream inventories trend in China through 2019.

Billets Inventories in China

Aluminium billets, cast from aluminium alloys to make automotive and aerospace parts, recorded weak inventories in China throughout the year. As of mid-February 2019, aluminium billets stocks stood at 169,300 tonnes, which by the end of June came down to 71,700 tonnes after registering a decline of 57.64 per cent or 97,600 tonnes. In the second half of the year, the stocks shrank further to 50,600 tonnes, meaning down by 42.62 per cent from the first half of the year. In the entire year, the billet inventories trended down by 70 per cent or 118,700 tonnes.

Aluminium Alloys (ADC12) price trend in China

Demand and consumption of aluminium extrusion and semi-finished products remained sluggish in China on slower growth in the country’s automotive industry. As a consequence, the aluminium alloy price (ADC12) recorded slowdown till August 2019. From RMB 14,850 per tonne in the beginning of the year, the price over the first seven months inched down to RMB 14,000 per tonne. But from the mid of August, the price of the aluminium alloys (ADC12) started increasing and by the year end clocked at RMB 14,750 per tonne, meaning although it declined over the year yet remained range-bound.

Tariffs and policy changes

With effect from September 28, 2019, Vietnam imposed an anti-dumping tax ranging between 2.49 per cent and 35.58 per cent on some aluminium products from China, as the Southeast Asian nation looks to rein in an ever-increasing trade deficit with its giant neighbour. As pointed out by the ministry, the aluminium imports from China nearly doubled last year to at least 62,000 tonnes. The figure excluded the amount of aluminium that transited through Vietnam.

The anti-dumping duty by Vietnam was levied on China’s both aluminium and non-alloy aluminium products in forms of bars, rods, extruded, treated and untreated surface, processed and unprocessed.

A few months after, Mexico also declared to impose countervailing duties on imported aluminium foil from China. The duty would be levied on imports that cost below $3.4817 per kilogram, reportedly said Mexico’s economy ministry after an anti-dumping investigation.

For Hangzhou Five Star Aluminium Co, Ltd, the countervailing duty would be $0.17968 per kilo, while for Jiangsu Zhongji Lamination Materials Co, Ltd and for Boxing Ruifeng Aluminium Co, Ltd and other exporters, the duties would be $0.17968 per kilo and $0.6588 per kilo, respectively.

In May, the Mexican government had imposed a provisional anti-dumping duty on aluminium foil coils imports from China. According to a preliminary ruling announced on May 24, duties were set at $0.17968-1.1634 per kg.

China, on the other hand, declared in November to remove import tariffs on unwrought aluminium alloy from Pakistan, with effect from December 1.

Trade Focus

China imported 18,706 tonnes of unwrought aluminium alloy in September, the highest since SMM records began in January 2018. From a month ago, the imports were up by 16.9 per cent, while from a year, they were higher by 140 per cent. In November, the imports increased further to 31,100 tonnes, up 86.9 per cent month-on-month and 242.1 per cent year-on-year

According to the latest data from China Customs, China's exports of aluminium foil fell 10.53 per cent year-on-year to 102,200 tonnes in November. On a month-on-month comparison, foil exports edged 1.87% higher, with products under HS code 76071190 and 76072000 accounting for the increase. In the first eleven months, aluminium foil exports totalled 1.18 million tonnes, an increase of 1 per cent year-on-year.

China Customs data also showed China’s aluminium sheet, plate and strip exports in October declined by 1.9 per cent from a month earlier to come in at 193,500 tonnes. In September, China’s export amount was 197,100 tonnes after declining by 9.7 per cent from August and 20.2 per cent from the same period last year.

To the US, China during January-September exported 102,000 tonnes of aluminium plates, sheets and bars, which was down from 221,000 tonnes during the same period last year, according to the USGS data.

But the United States total imports of aluminium plates, sheets and bars in the nine months of the year stood at 1.15 million tonnes, up from 1.05 million tonnes during the contemporary period in the year last. But its imports of crude, metals and alloys declined during January-September 2019 from 3.23 million tonnes in the last year to 2.03 million tonnes.

Besides China, Canada is another important supplier of aluminium to the US (including semi-finished and crude, metals and alloys). During January-September 2019, the US imported 146,000 tonnes of aluminium semis and 903,000 tonnes from crude, metals and alloys. The former was down by 21.05 per cent year-on-year from 186,000 tonnes and the former by 46 per cent from 1.66 million tonnes.

Conclusion

There has been a potential growth in the demand and use of aluminium downstream products over the years that bolstered the developments and expansions of new projects in the industry in 2019. However, the demand for flat rolled products, in particular, saw a marginal growth in Europe of about 1.5 per cent. In North America, demand for aluminium downstream products was up by 2.1 per cent. These marginal growths in demand could be attributed to the overall global economy slowdown.

In China, demand and consumption of aluminium extrusion and semi-finished products remained sluggish on slow progress of the automotive industry, which in turn led to no major developments of the downstream projects. The inventories slowed down at the highest pace and stood at 71,700 tonnes at the end of the year.

Responses