您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

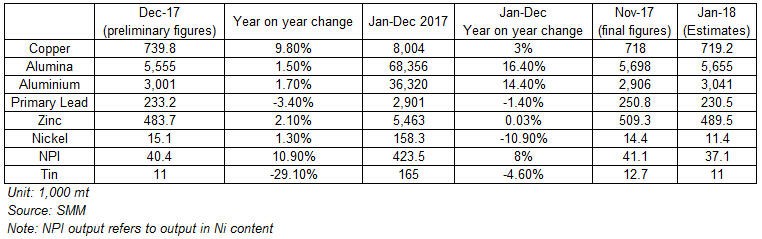

SMM has published the latest output data from the major Chinese producers in the base metals market. The following table shows the latest output for alumina and aluminium in December and a forecast for January.

The report shows a drop in alumina production month on month, as December output drops from that in November. SMM sees three reasons for the alumina output drop in December:

Winter production cut in Nov-Dec is one of the major factors that affected production numbers of companies including Henan East Hope Sanmenxia, Kaiman, Shanxi Zhaofeng, Fushen, Shandong Weiqiao and China Aluminium Shandong Branch.

East Hope Sanmenxia and Henan Zhongmei were ran operations at only 50% of their capacities during the 30-day special green policy in Henan province. Shandong branch of the Aluminium Corp of China (Chalco) was also under pressure because of that.

Shortage of natural gas supply affected output in China Power Investment Corporation and Kaiman and affected alumina producers that depend on natural gas power. While Huiyuan has resumed its operations, Inner Mongolia Xinwang is expected to resume by the end of January. Maintenance work affected one production line of Guangxi Xinfa in December bringing down the total output.

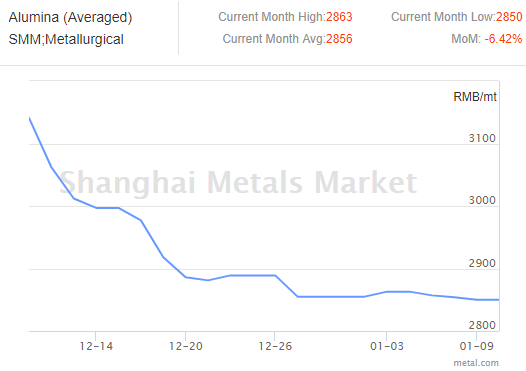

As reported by SMM, Average spot alumina price in China remains unchanged at RMB 2850/t today. Chalco and imported alumina prices also remain unchanged. Primary ingot prices register a slight gain in all major markets. Prebaked anode price in Northwest China market registers a drop and settles at RMB 4800/t today.

SMM forecast China’s alumina output to grow in January due to the closure of Henan’s special green policy and the newly-increased capacity of Liulin Senze and Huaqing Aluminium.

Responses