您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

Spot alumina price saw some unprecedented highs in 2018 first half and doubled to over $700 per tonne as the market showed panic reaction to U.S. sanctions on Oleg Deripaska and Rusal entities in April. The supply scenario was disrupted by two major happenings. First, the fifty per cent capacity closure in Hydro’s Alunorte refinery in Brazil in March on the issue of bauxite residue pond leakage, followed by US sanctions on Rusal.

The sanctions put the future of Rusal’s Aughinish alumina plant in doubt, which is Europe's largest alumina refinery in Ireland and a major alumina asset of RUSAL contributing about 30 per cent of alumina produced in the EU. Aughinish won a reprieve as the U.S. Administration extended the sanctions deadline till October and currently negotiations are on for a complete lifting of sanctions.

Following the sanction announcement by the US, Rio Tinto announced on 13 April 2018 that it had reviewed arrangements it had with impacted entities and was in the process of declaring force majeure on certain contracts. However, with the extension of the wind-down period until 23 October 2018, no force majeure declaration was made to date. However, alumina prices have not gone back to the pre-sanction level on uncertainities surrounding supply.

Australia Alumina FOB price

Norsk Hydro CEO Svein Richard Brandtzaeg recently said that despite the ongoing talks between the company and Brazilian regulators on Alunorte alumina refinery situation, no timeline has been set yet on the final ramp-up. Hydro Alunorte is the world's largest alumina refinery with 5.8 million tonnes of annual capacity and it exports 86 % of its total production. Hydro’s EBIT for H1 2018 also drops to NOK 1,104 million from NOK 1418 million in H1 2017 due to 50% production cut at both Alunorte and Paragominas.

Shares in Alumina Limited have traded at 10-year highs after a 30 per cent rise in alumina prices and a sliding Australian dollar delivered the best margins in the company's history. While Alumina's joint venture partner Alcoa downgraded its profit forecasts on tariff woes, Alumina Limited is on a high due to supply disruptions. It is benefiting from significant supply disruptions in the global alumina market, particularly in Brazil where the world's biggest alumina refinery is out of action. The supply shortage allowed the refineries that Alcoa and Alumina jointly own to generate healthy margins in June quarter.

On the other hand Chinese alumina refineries have started cutting production. Liaoning province in China was about to start an alumina refinery with a capacity of 10 million tonnes of alumina every year. But unfortunately, the project plan got cancelled by the city of Chaoyang after public consultation. The refinery was scrapped because of differing opinions from city residents on its environmental impact assessment.

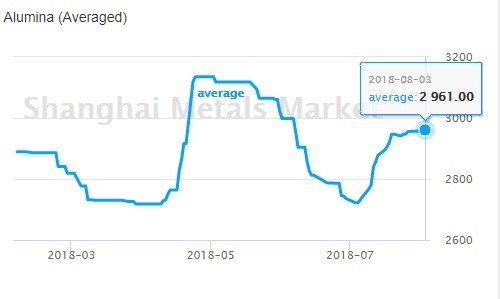

China spot alumina price

According to the latest update by Shanghai Metals Market, alumina production in Lvliang of Shanxi province is likely to be affected as the area was highlighted in China’s three-year initiative to “make skies blue again”. From Beijing-Tianjin-Hebei region, the key focus areas of this initiative will further expand to include some of the surrounding cities like Jinzhong, Yuncheng, Linfen, and Lvliang in Shanxi province, Luoyang and Sanmenxia in Henan province, and Xi'an and Tongchuan in Shaanxi province. Though China exports very less of alumina, the country’s alumina export has seen a solid growth since April.

These developments may be a sign of things to come, promising further turbulence ahead in the alumina market. During Q2 2018 results, Alcoa projected a full-year 2018 global deficit for both aluminium and alumina. For alumina, the company projected a slightly lower global deficit between 200 thousand and 1 million metric tons. Alumina prices will continue to be under pressure and the market will remain tight in partial absence of two major producers in operations.

Responses