您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

Stock image for referential purposes only

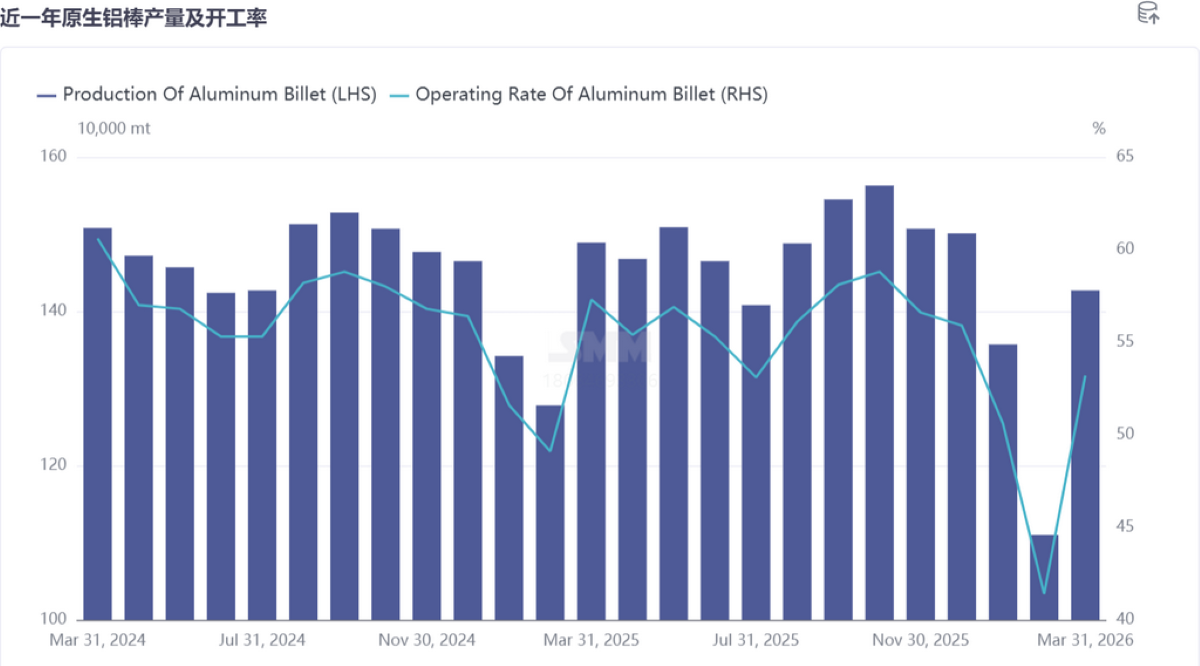

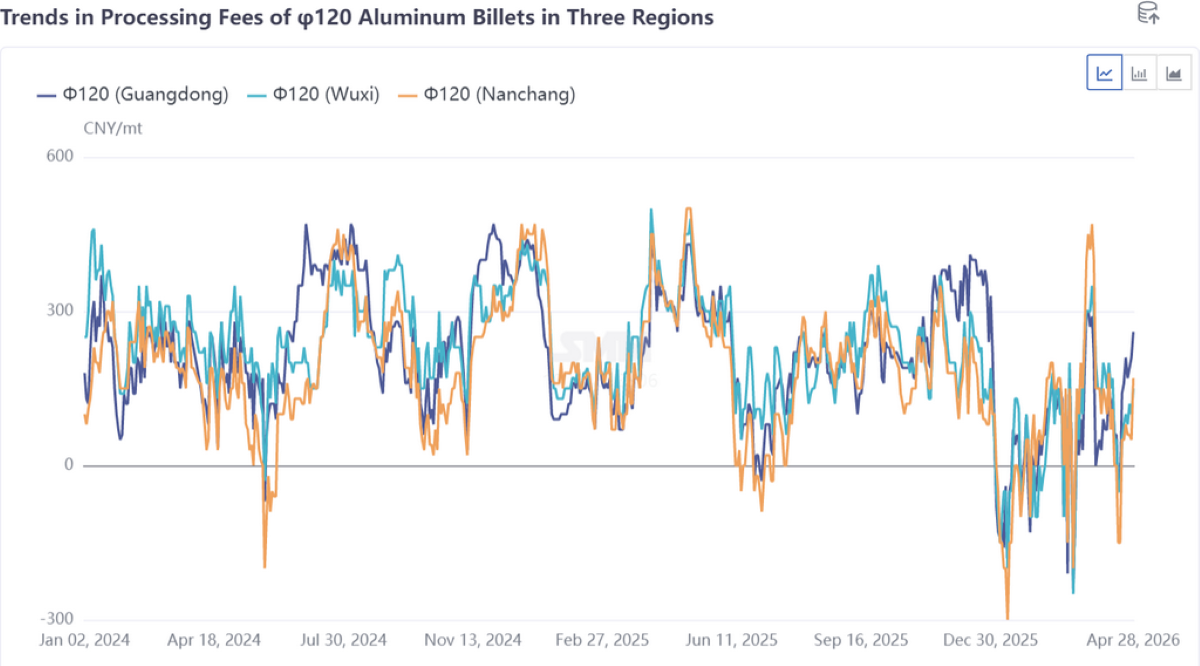

SMM Aluminium Billet Market: In March, the aluminium billet operating rate rebounded significantly by 11.8 percentage points M-o-M to 53.2 per cent, but still declined 4.1 percentage points Y-o-Y. Downstream profile enterprises basically completed resumption of work after the Lantern Festival, with improved raw material purchase willingness and intensity. The aluminium billet market transactions were in an accelerated recovery phase, and both social inventory and in-factory inventory of aluminium billets showed clear destocking trends. As the PV and battery sectors entered the export order rush period, industrial billet orders recovered, providing certain support to the domestic aluminium billet supply side in March. However, as the sluggish trend in the architectural profile sector remained unchanged, end-use demand was still difficult to see substantial improvement. The processing fees for 6063-grade construction billets, which dominated the market at low levels, could hardly be called satisfactory. Although the centre slowly rose from previous lows, it continued to remain below the cost line since Q1. Meanwhile, high aluminium price fluctuations were unfavourable for the stability of processing enterprise orders while driving production costs to surge sharply. Actual transactions still relied on volume discounts, and aluminium billet enterprises hovering on the edge of losses still faced severe capital pressure. Downstream enterprise restocking sentiment was clearly under pressure, industry profits declined, and competition intensified continuously, causing the overall recovery performance of the aluminium billet supply side during the March peak season to fall short of prior expectations.

{alcircleadd}

Image source: https://news.metal.com/

As April draws to a close, demand-side recovery is the core driver for alleviating inventory pressure. Pre-Chinese New Year stockpiling by downstream industries was relatively limited this year. After the holiday, as enterprise operating rates steadily rebounded, terminal rigid demand orders were continuously released, providing strong support for spot warehouse withdrawals. Combined with the traditional "Golden March, Silver April" peak consumption season deepening gradually, downstream processing enterprises' purchase willingness recovered, and spot market transactions were generally active, effectively offsetting the incremental pressure from the upstream supply side. However, the core contradiction of aluminium billet actual transactions relying on volume discounts showed no significant improvement, and downstream restocking actions became increasingly cautious and rational. Considering the domestic proportion of liquid aluminium, production expectations of aluminium billet sample enterprises, and the performance of post-holiday aluminium billet social inventory, in-factory inventory, and processing fees, SMM expects the domestic aluminium billet supply side to maintain stable operations in April, with the operating rate expected to edge up slightly to around 53.3 per cent. However, this remains low compared to peak season levels in the same period in previous years, and the intensifying cut-throat competition remains severe.

Notably, as the transition from peak to off-season approaches, May-July enters the high-incidence period for phased production cuts at aluminium billet enterprises, and signs of this are already emerging in south-west China. Although aluminium billet processing fees in three regions have shown signs of bottoming out since late April, the performance since Q1 has left aluminium billet enterprise profitability in a worrying state. Production efficiency at billet plants in some regions has weakened, with enterprises resorting to production line maintenance, equipment servicing, product switching, and raw material reduction to achieve marginal production cuts. The domestic aluminium billet operating rate is expected to show no improvement in May.

Considering the current industry situation, the aluminium billet market is unlikely to see a strong reversal in the short term. The supply-demand structural imbalance continues to be prominent, industry shipment resistance remains elevated, and aluminium billet processing fee competition is becoming increasingly fierce, with cut-throat competition intensifying continuously. At this stage, the market generally adopts a low-price-for-volume business model, and the procurement side generally follows market trends and purchases based on prevailing prices, which has become the industry norm.

Image source: https://news.metal.com/

Looking ahead, primary aluminium price fluctuation trends, the recovery pace of profile end-use orders, and industry-related regulatory policies will be the core key factors determining aluminium billet market trends and driving market recovery.

Note: This article has been issued by SMM and has been published by AL Circle with its original information without any modifications or edits to the core subject/data.

Responses

_0_0.jpg/500/0)