您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The year 2018 was marked by supply and trade disruptions and price volatility in the aluminium sector. Alumina supply was disrupted and price shot up. The U.S. imposed 10% duty on all imported aluminium. Rusal aluminium was sanctioned by the U.S. and banned by LME and the US-China trade war disrupted the market balance. There was a supply concern in the primary sector. However, the beginning of 2019 has indicated a solution to supply issues and prices have started consolidating.

The start of 2019 has already witnessed the lifting of sanctions on Rusal by the US Government and trade negotiations between the U.S. and China are taking shape in a positive manner. Concerns over raw material insecurity is also slowing down with Alunorte refinery likely to start full production by the second quarter of 2019 and Alcoa’s worker issues getting solved. Going forward, the outlook for aluminium industry in 2019 is expected to be moderately optimistic. World aluminium usage stood at 86 million tonnes in 2018 and is expected to reach 90 million tonnes in 2019.

{alcircleadd}

Aluminium cannot be seen as an independent commodity as the market is driven by forces that have impact on the entire value chain. We are starting our outlook analysing how the policy changes and developments of 2018 are building a foundation for 2019. We also look at how the industry has fared in the first two months of 2019 and aim to analyse the way aluminium value chain is poised to grow in 2019 vertical wise.

Why should you buy AlCircle’s “Preview of Global Aluminium Industry Outlook 2019”?

For the detailed Table of Contents, click here.

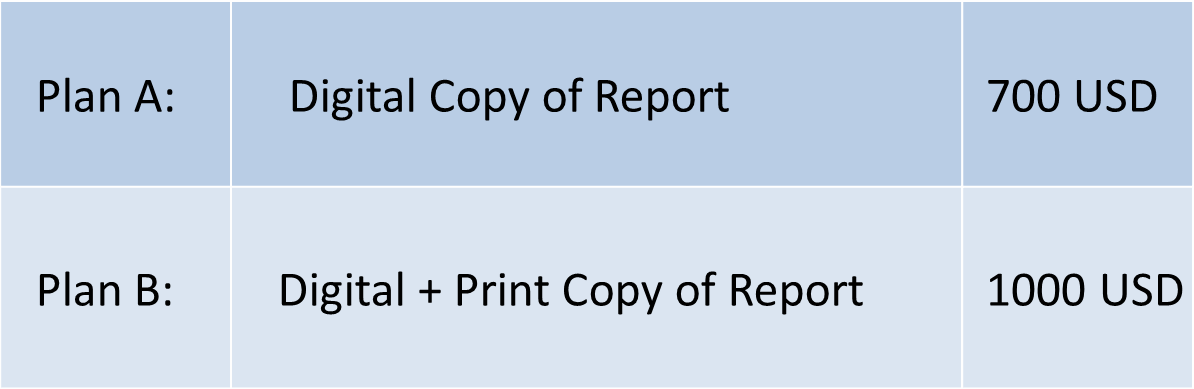

The Outlook 2019 Report is now available in both Digital as well as Print format. Both the available options along with their pricing details are as follows:

So, wait no more! You can now buy your copy of A Preview of Global Aluminium Industry Outlook 2019 by clicking here and for any further query, reach out to us at booking@alcircle.com.

Responses