您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

According to the latest update by Shanghai Metals Market, demand in the aluminium plate/sheet and strip industry weakened in China, which as a result boosted the inventories of finished products across all major Chinese consumption areas. Plants grappled with tight cash flows amid growing competition due to increasing recommencement of productions and also because of the narrow export market, as a consequence of the United States higher anti-dumping and anti-subsidy measures on China.

The aluminium foil industry also showed a dent in its performance in the month of July, buoyed by a plunge in demand for beer foil, household foil, and air-conditioner foil, observed SMM. New orders for air-conditioner foil fell sharply as most air-conditioner manufacturers began a seasonal break.

The low season extended in the construction aluminium extrusion industry as well in July, as high temperatures affected the demand. Demand in the industrial aluminium extrusion industry also continued to tumble owing to poor demand from the railway, automobiles, and photovoltaic sectors.

The aluminium wire and cable industry showed no better performance either as the overall production fell in the first half of the year despite the onset of a few new orders. Large producers began shifting to their industries that also contributed to the decline in the industry.

In the primary aluminium alloy industry, capacity that underwent maintenance in June returned online in July. Several manufacturers of wheel hubs closed on high temperatures in the summer, affecting new orders at some producers. Declines in new orders, however, eased some of the backlogged orders.

In another update by SMM, some 30,000 tonnes of primary aluminium consumption would likely be affected be affected in Gongyi city of Henan, as local downstream processors required to stagger suspensions during July and August. Moreover, lower demand in downstream sector could necessarily weigh on primary aluminium consumption.

Except the 30 top enterprises, all gas-emission related industrial plants in the city were instructed to suspend their smelting furnaces for a month because of the anti-pollution measures. SMM data showed 67 cast coil production lines in Gongyi were ordered to suspend. Most local producers chose to cut output by 50% each in July and August.

Shifted in interests from aluminium ingots to cast coil billets were also seen because of smelting capacity cut across cast coil producers. This may also contribute to the decline in primary aluminium consumption further.

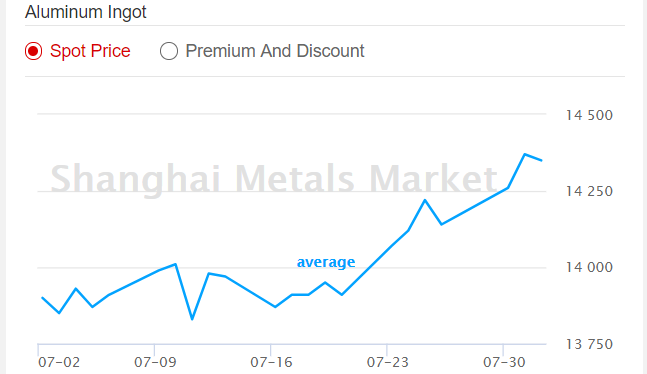

Slower consumption depressed local aluminium prices and the price spread between spot aluminium ingot in Gongyi and Shanghai widened to RMB 100 per tonne as of Tuesday July 31, from RMB 50 per tonne two months ago.

SMM assessed A00 aluminium ingot in Gongyi at RMB 14,260 per tonne to RMB 14,280 per tonne on July 31, while the average ingot price in China stood at RMB 14,370 per tonne. On August 1, the price dwindled a bit to RMB 14,350 per tonne, with expected spot discounts to settle at RMB 90 to RMB 50 per tonne.

The average price of aluminium alloy (ADC12) showed no change over the month, standing at RMB 15,550 per tonne.

Responses