您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The global push for low-carbon or “green” aluminium is intensifying competition for available scrap. According to global market trends research, regional economies are ramping up remelting capacities and prioritising the retention of domestically generated scrap to meet internal demand.

Source: TradeIndia

China remains the world’s largest consumer of recycled aluminium, with usage reaching approximately 12.01 million tonnes in 2023. This figure is projected to rise and cross fourteen million tonnes by 2026 (f). However, it is anticipated to cross nineteen million tonnes by 2030 (f), followed by Western Europe, the rest of Asia (excluding China), and North America.

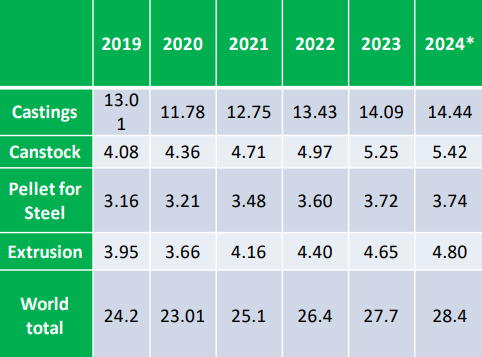

In 2020, amongst the various applications of recycled aluminium, canstock was the only one to witness growth. Demand from most other applications declined in 2020, while the demand from the steel sector for aluminium pellets remained stable during the year.

The automotive industry is a primary demand driver and a focus market for secondary aluminium alloys, particularly grades such as ADC12 and A380. In 2023, there was an overall increase in global recycled aluminium usage. The castings segment witnessed a significant recovery, reaching 14.09 million tonnes, while canstock, pellet for steel, and extrusion also demonstrated growth, with 5.25, 3.72, and 4.65 million tonnes, respectively.

Source: AL Circle Research estimate

World Recycled ALuminium Market Analysis Industry forecast to 2032

In 2024, these trends continued, with the castings segment reaching 14.44 million tonnes, canstock at 5.42 million tonnes, pellet for steel at 3.74 million tonnes, and extrusion at 4.80 million tonnes. The year 2024 signifies an essential point in the data, as it sets the stage for forecasting the future of recycled aluminium usage by end-use segments.

Looking for the latest insights on aluminium dross recycling and recovery technologies? "Aluminium Dross Processing: A Global Review" delivers an unmatched global analysis of aluminium dross (white & black dross/aluminium ash & salt slag) generation, dross processed, and metal recovery rates, cutting-edge technologies, key suppliers, and trade trends across all regions.

In recent years, China’s aluminium industry—including the recycled aluminium sector—has undergone significant reforms. These include restrictions on aluminium scrap imports and the introduction of stricter quality standards for imported material.

Between 2024 and 2026, as per different types of market segmentation studies, planned expansions in secondary aluminium capacity are expected to exceed both current and anticipated scrap supply far. The tightest shortages are forecast for used beverage cans (UBCs) and extrusion scrap. Asia, and particularly China, is becoming a dominant demand hub for both wrought and cast scrap, intensifying competition for feedstock with Europe and North America. While regulatory measures and advances in sorting technologies will help improve scrap recovery and quality, they will not be sufficient to bridge the widening gap between supply and demand.

As per AL Circle Research, the global recycled aluminium usage by end-use segments has shown resilience and growth in the face of economic challenges. This is a promising sign for both the aluminium recycling industry and the broader sustainability goals, as it indicates an increasing reliance on recycled aluminium across various applications, with a positive CAGR outlook for the years ahead.

Responses