您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

Rio Tinto has released H1 2019 results with 9% higher consolidated sales revenue of US$20.7 billion in comparison with H1 2018. Higher iron ore prices offset the impact of lower volumes and lower aluminium prices. The aluminium business suffered from price declines, in particular in aluminium price despite strong volumes.

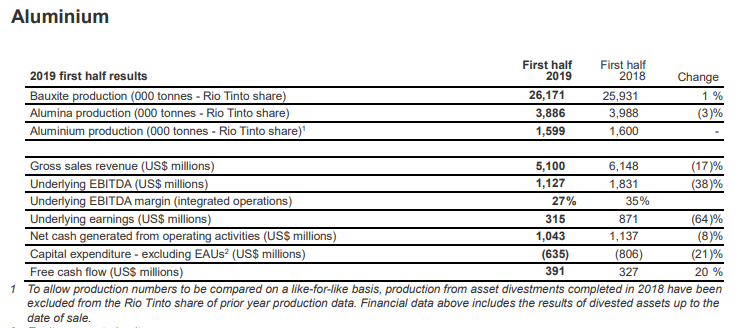

Underlying EBITDA for aluminium business stood at US$1,127 million in H1 2019, down 38% from US$1,831 million in H1 2018 attributed to lower aluminium price. Underlying earnings stood at US$ 315 million, down 64% from US$ 871 million in H1 2018. Gross revenue stood at US$ 5,100 million, down from US$6,148 million in H1 2018. Lower price for primary metal remained the principal driver for the declines.

Gross revenue for Primary Metal stood at US$2,490 million, down from US$ 3,328 million in H1 2018. Underlying EBITDA stood at US$ 306 million, down from US$ 917 million in H1 2018.

Average price for aluminium was down 17% compared with 2018 first half. The mid-west premium for aluminium in the US averaged $420 per tonne - 6% higher than in 2018 first half. The company achieved an average realised aluminium price of US$2,174 per tonne compared to US$2,547 per tonne in 2018 first half. VAP represented 54% of the primary metal sold in H1 2019.

The company continued to realise value from cost improvement and value-added product initiatives.

Aluminium production of 1.6 million tonnes was in line with 2018 first half. Excluding the non-managed Becancour smelter in Canada, where a lock-out constrained operations, aluminium production in H1 was 1% higher YoY, reflecting continued productivity improvement.

On 2 July 2019, management and unions at the Becancour smelter agreed to a new labour arrangement which resulted in the restart of operations at the end of July, with full ramp-up expected in the first half of 2020.

Rio expects its aluminium production in 2019 to be between 3.2 to 3.4 million tonnes of aluminium.

Responses

_0_0.jpg/500/0)