您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

House of Lords Lunch 2026

Aluminium is often described as the ultimate circular material, and in many respects that is true. In the UK, we have built a system over decades that is already highly effective. Collection rates are strong, recycling systems are established, and remelting capability exists across the supply chain. This is not a sector starting from scratch, nor is it one in need of fixing at a fundamental level.

{alcircleadd}What is less well understood is that the real challenge facing aluminium in the UK is not about recycling performance. It is about value. More specifically, it is about where that value is captured, and whether the UK is in a position to retain it.

Too often, aluminium is still framed as “scrap” and that language matters. It underplays the reality that secondary aluminium is one of the UK’s most important domestic raw materials, particularly in a country with very limited primary production capacity. As highlighted in ALFED’s recent reports, secondary aluminium delivers up to 95 per cent energy savings compared to primary production and plays a central role in both industrial competitiveness and net zero delivery.

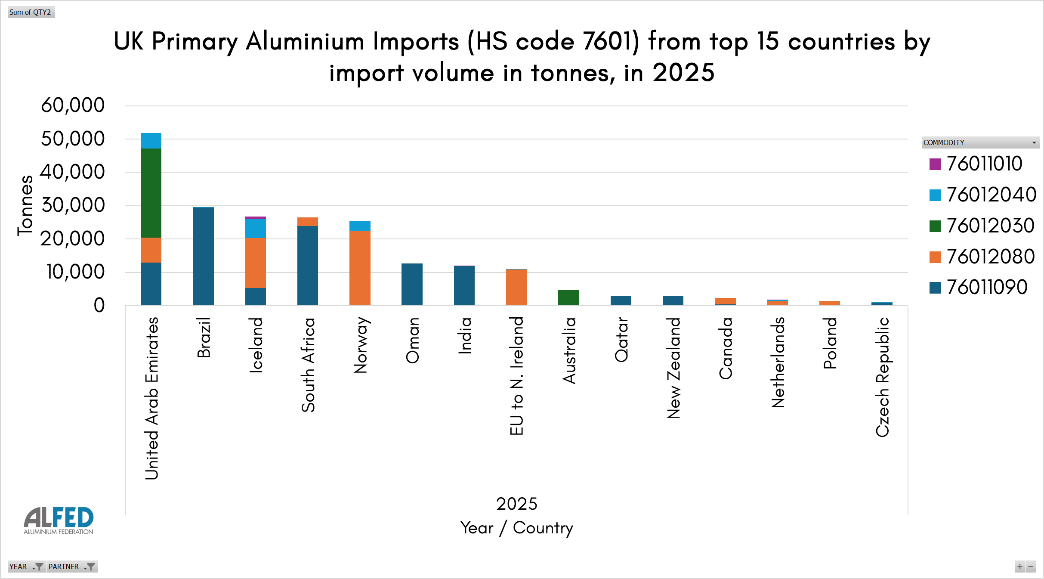

At the same time, the UK remains heavily reliant on imported primary aluminium. In 2025 alone, around 68,000 tonnes were imported from the UAE, Bahrain, Oman, Qatar and Saudi Arabia. That reliance has always carried a degree of exposure, but recent geopolitical instability and disruption to energy-intensive smelting operations in the region have brought that risk into sharper focus. Supply chains that once felt stable are now subject to external pressures that the UK cannot control.

This is where circularity becomes more than an environmental concept. It becomes a question of resilience. If we can make better use of the material already within our system, through improved alloy development, processing capability and closed-loop applications, there is a real opportunity to reduce that dependency over time.

The issue is that while the UK generates significant volumes of aluminium scrap, we are not consistently retaining the value associated with it. Material flows are increasingly shaped by global pricing and demand rather than domestic industrial need.

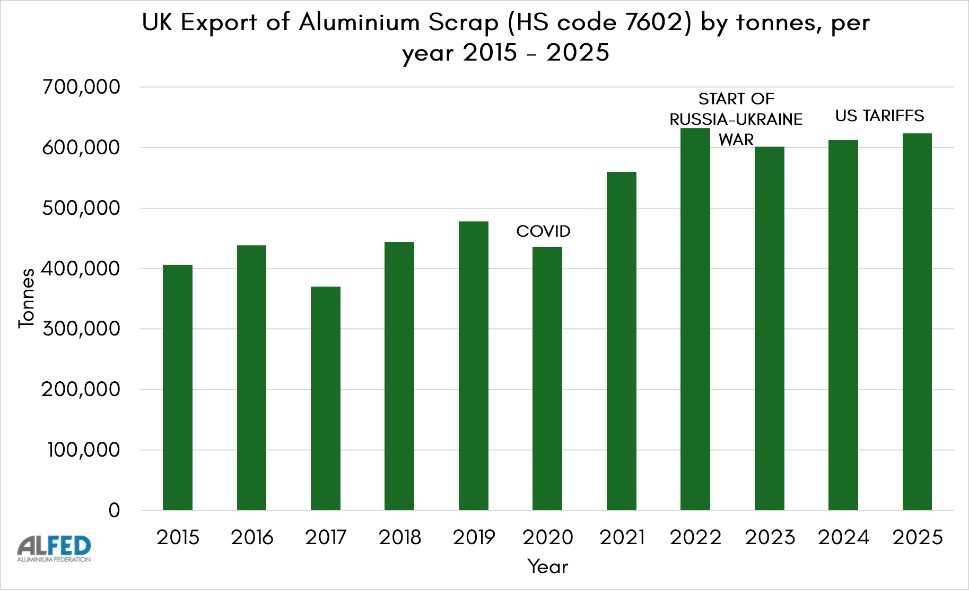

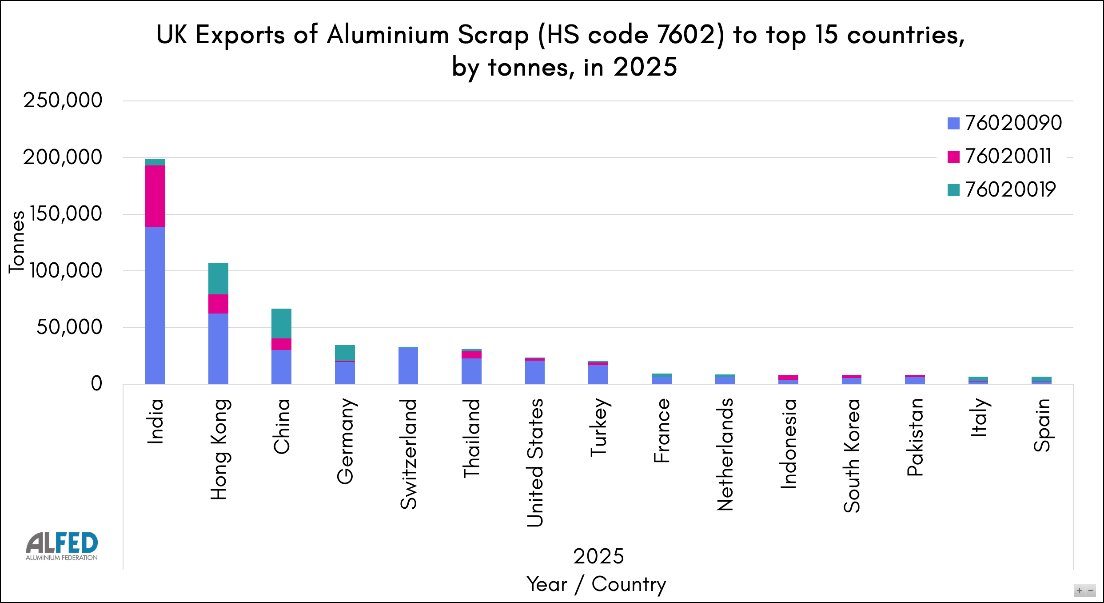

Recent data illustrates this clearly. Exports of aluminium scrap to the United States increased significantly from around 2,000 tonnes in 2024 to over 23,000 tonnes in 2025. Overall exports under the 7602 HS Commodity Code rose from around 612,000 tonnes in 2024 to over 623,000 tonnes in 2025. The increase itself is relatively modest, but the direction of travel is important. It shows that flows are shifting and increasingly responding to global demand signals and geopolitical dynamics.

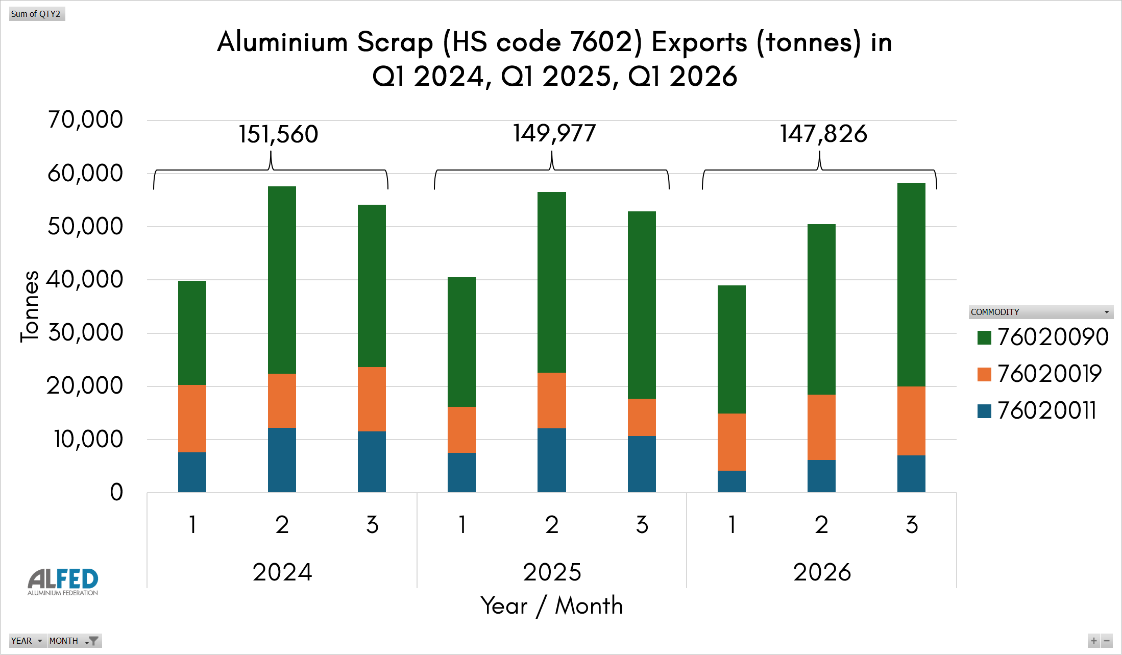

At the same time, the UK imported around 90,000 tonnes of aluminium scrap under HS code 7602 in 2025. This is not a question of shortage. It is a question of how material moves, where value is captured, and whether the UK is competitive enough to retain and process more of that material domestically.

The underlying constraint is structural. The UK has strong collection systems and established demand, but there is a clear gap in the midstream. This includes advanced sorting, alloy-specific processing and recycling-to-product infrastructure. Without sufficient capacity in these areas, exporting material often becomes the most viable option, even when greater long-term value could be achieved through domestic processing.

House of Lords Lunch 2026

This is where aluminium differs from other metals and why it requires its own policy lens. Aluminium is highly sensitive to alloy composition and relies on precise, often closed-loop systems. The economics of processing are different, and the investment required sits at a different point in the value chain. A one-size-fits-all approach risks missing that nuance.

There is also a broader international dimension that cannot be ignored. The UK aluminium sector is deeply interconnected with Europe through ownership structures, processing routes and supply chains. At the same time, we are seeing increasing policy movement within the EU around scrap retention and circularity. If those policies develop further, and the UK does not respond in a coordinated way, there is a real risk that the UK becomes a net supplier of scrap into a more protected system.

This is why ALFED’s position has been clear and consistent. We are not advocating for export bans. Aluminium operates within a global market and trade is an essential part of that system. The focus instead must be on improving the underlying market conditions that influence where material flows.

At present, it is often simply not competitive to process scrap within the UK. That is the core issue. Rather than restricting exports, the priority should be to create the conditions that make domestic processing the most attractive option.

This means addressing industrial competitiveness, particularly energy costs. It means strengthening domestic demand signals so that UK-produced and recycled aluminium is actively pulled through the system. It also means improving classification and data transparency so that the true value of different material streams can be understood and optimised.

This work is already underway. Through the UK Aluminium Alliance, ALFED is working with industry and government to map capability, identify gaps and build the evidence base for investment. The Alliance provides a framework that connects supply, processing, demand and policy into a single system view, recognising that none of these elements can be addressed in isolation.

What we are hearing consistently from industry is that the appetite to invest exists. The barrier is not willingness, it is confidence. Investors need clear, stable signals and a competitive environment that supports long-term decision making. Without that, the UK risks continuing to export not just material, but the opportunity to create value from it.

There is a clear opportunity here. The UK already has the foundations of a strong circular aluminium system. We have the material, we have the demand, and we have the technical capability. The question is whether we can align policy, market conditions and investment in a way that allows that system to deliver its full value.

Recognising aluminium scrap as a strategic secondary raw material is an important step. From there, the focus must be on building the conditions that allow it to be processed, utilised and valued within the UK.

This is not about restricting trade. It is about strengthening resilience, improving competitiveness and ensuring that circularity translates into real economic benefit. With the right policy framework in place, aluminium can play a central role in the UK’s industrial future, not just as a recycled material, but as a cornerstone of a modern, resilient and competitive manufacturing base.

Read all the latest developments in Europe’s aluminium recycling industry

Disclaimer: This article reflects the personal perspective, expertise, or opinion of an individual guest writer. All the information and claims presented here are those of the author alone.

Responses