您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The year 2019 can be called an aftermath of trade wars, restrictive tariffs, sanctions, capacity cuts and price volatility that impacted the aluminium value chain the year earlier. 2019 has experienced a steady drop in alumina and aluminium prices worsened by weak market fundamentals and falling demand for the metal, globally and in China. Slowdown in global economy resulted in a downturn in the global automotive sector and saturated growth in the construction and aerospace segment further putting pressure on the demand. Industry players and market participants have already lowered demand projection for the full year 2019 and for 2020. Here is a quick look at how the primary aluminium industry moved in 2019 and what is expected in near future.

Production & Consumption

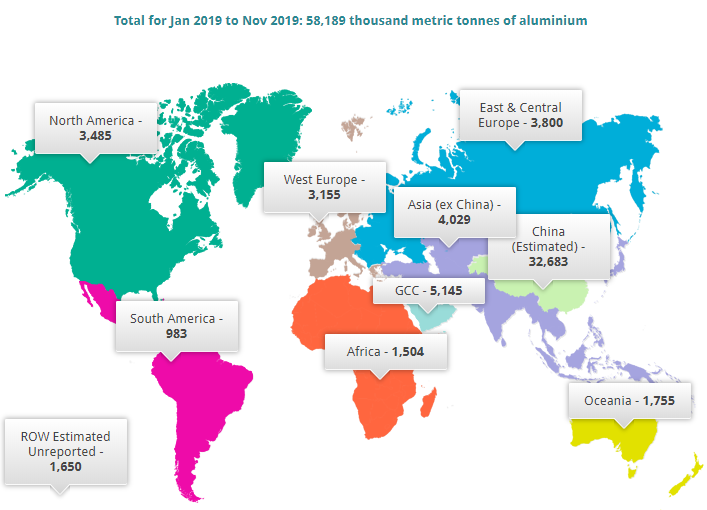

{alcircleadd}Global primary aluminium production totalled 5.2 million tonnes in November, with a year-on-year drop of 2.4%, according to the latest data showed by the International Aluminium Institute (IAI). On a month-on-month comparison, aluminium production dropped by 2.8% from 5.34 million tonnes in October. Primary aluminium production amounted to 58.1million tonnes in the period from January to November 2019 as compared to 58.8 million tonnes in the same period of 2018. This records a slip of 1.1% year-on-year indicating a production drop.

Australia’s Department of Industry has also lowered its forecast for global primary aluminium consumption in 2019 by 3% to 64.48 million tonne indicating a deficit of about 1 million tonne.

China, which contributed more than 56% of total global primary aluminium output in October, produced 2.94 million tonnes of aluminium in November, down 0.81% year on year. According to the National Bureau of Statistics, output in January-November stood at 32.13 million tonne, with a year-on-year decline of 0.6%.

With 1.99 million tonnes coming online in the first 10 months of the year, 40.69 million tonnes of yearly primary aluminium capacity was built in China as of the end of October, and 35.1 million tonnes in operation. Operating capacity of aluminium is likely to increase further in December with new capacity coming online.

SMM expects China’s primary aluminium production to stand at 3.05 million tonne in December, up 1.94% year on year. At this rate the yearly production for full year 2019 is likely to be about 35.44 million, 1.8% less, compared to 36.5 million tonnes in 2018. Primary aluminium consumption in will amount to 36.07 million tonne, down 1.53% year on year. Inventories across social warehouses will continue to shrink in December at a slower pace.

Inventory Situation

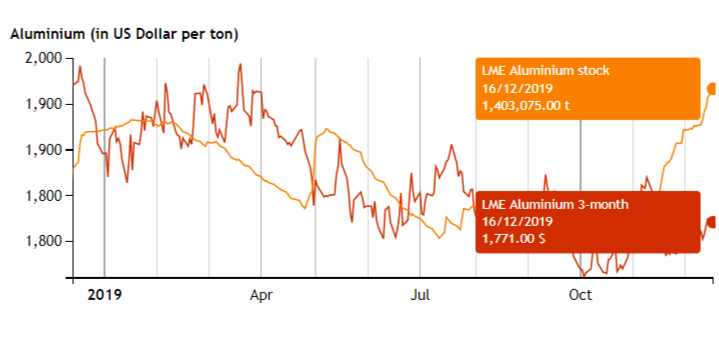

LME aluminium stocks started the year with 1 million tonne. While the stocks continued to fall throughout the year, it has started rising from mid-November. Currently, LME aluminium stock stands at 1.4 million tonne.

China’s aluminium stocks are in all time low currently, driven by higher consumption and lower arrival of stocks. According to SMM data, aluminium stocks in eight consumption areas in China, including SHFE warrants, dropped to 611,000 tonnes, as of Monday, December 16. Aluminium stocks dropped about 250,000 tonnes in last 45 days.

According to Morgan Stanley “Global reported inventories (LME plus other warehouse systems) total 2.78 million tonne, but we estimate a further 9 million tonne of unreported stock remains.”

It is this unreported stock which worries the major primary aluminium producers. If the proposed new LME warehousing rules designed to increase the competitiveness of LME warehouses take effect in Feb 2020, it would bring more inventory to light next year weighing on the price.

Demand Supply Analysis

According to a CRU analyst, Paul Williams, Head of Aluminium, aluminium market is moving into surplus by the beginning of 2020 as demand continues to weaken around the world. About 461,000 tonne of stocks have been added to LME warehouses in the last one month. The increase in stock is driven by backwardation and weak demand in the market.

Wood Mackenzie forecasts a deficit of about one million tonnes in 2019, which will be because of the drop in China. China closed about 3 million tonnes of production in H2 2019 and added more to it this year including the closure from Xinfa Group and China Hongqiao Group.

Global aluminium stocks are expected by Wood Mackenzie to end the year at 12 million tonnes. Wood Mackenzie expects global demand to grow 1.1% in 2019 from 3.6% in 2018 and Chinese demand to rise 2.9% from 6.1% in 2018.

Alcoa continued to project a global aluminium deficit ranging between 800 thousand and 1.2 million tonnes in 2019. The company significantly lowered its global aluminium demand growth projection for 2019 to a range of -0.6 per cent to 0.4 per cent.

“The change is driven by weakening macroeconomic conditions, trade tensions between the US and China, and contracting manufacturing activity, especially in the global automotive sector,” Alcoa said.

RUSAL expects that global primary aluminium demand will be unchanged year-on-year in 2019 to 66 million tonnes, and the overall balance to be in deficit of around 1 million tonnes.

Falling primary aluminium demand and rising semi-finished demands are the two contradictory issues affecting the sector. Falling automotive sector, global trade tensions, and increased use of scrap is depressing global primary aluminium demand in 2019.

Aluminium can sheet utilizes recycled aluminium in the product mix and does not consume much of primary aluminium. It is expected that the slowing in the manufacturing and automotive sectors could start to flow through to construction markets in several regions. All these factors are indicating a market surplus in Q4 2019 both in China and the rest of the world. However, the fall in demand is likely to be offset by plunging aluminium inventory in China.

We expect about 1 million tonne of primary aluminium deficit in 2019.

Price Analysis

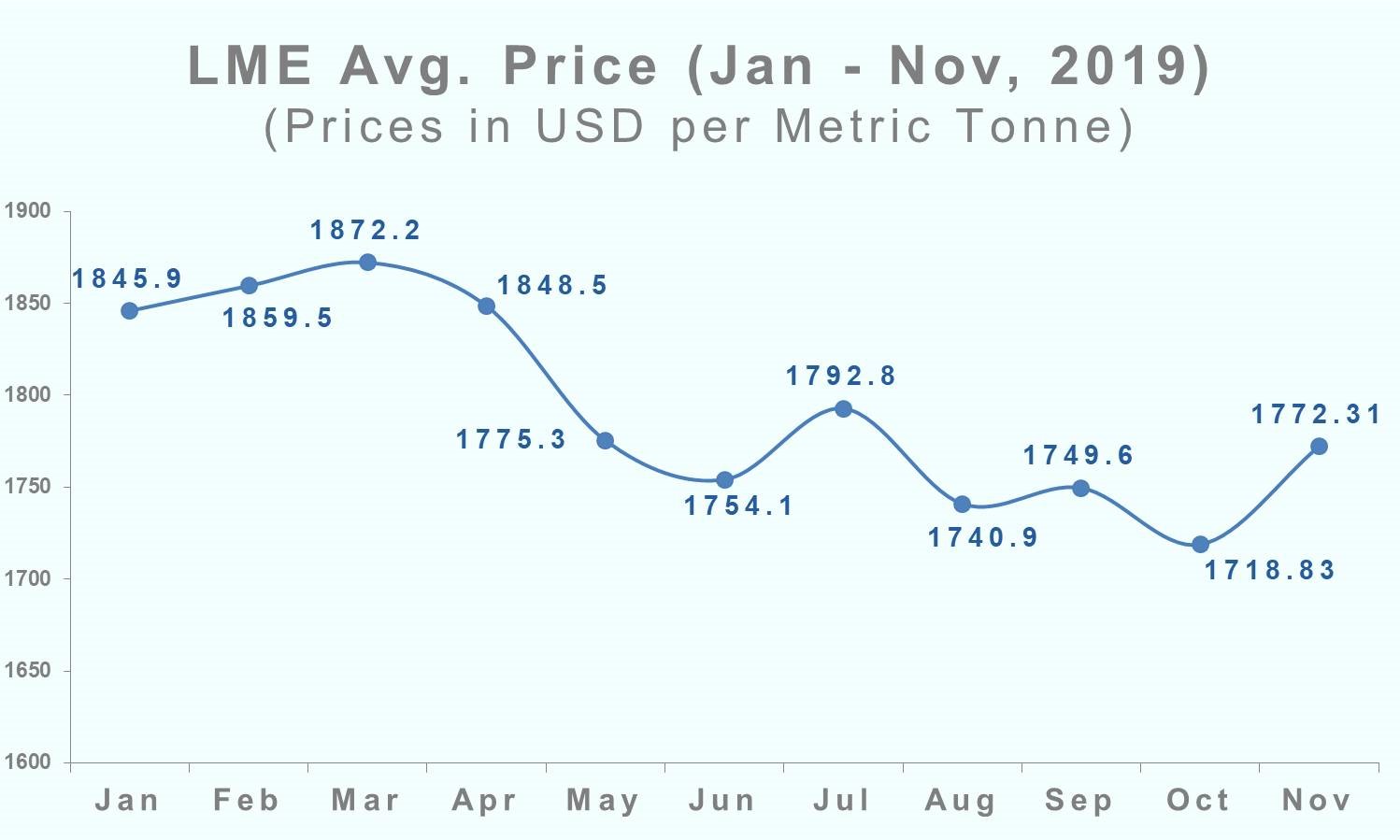

Slow industrial growth and demand in China, and concerns over a global economic slowdown following the US-China trade war led to falling demand and plunging aluminium prices in 2019. The fall in prices was further driven by expectations of excess supply, and rising semi-finished aluminium exports from China due to lower domestic demand. It has impacted primary aluminium demand and prices in ex-China world. We can see below the avaerage LME aluminium cash price movement over 2019.

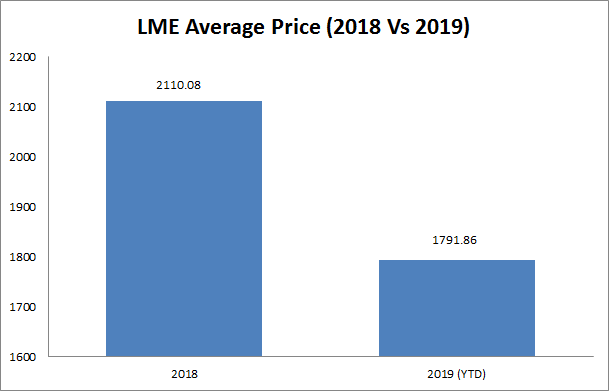

The three month aluminium price stood at US$1,970 per tonne in the beginning of 2019. After remaining elevated, in the range of US$1,850 per ton to US$1,950 per tonne, aluminium prices started dropping faster in the second half of 2019, to reach close to US$1,700 in the beginning of October 2019. Currently, three months aluminium price stands at US$ 1,771 per tonne. The average LME price in 2019 has come down to US$1792/t from US$2110/t in 2018.

Aluminium premiums have also been put pressure by a persistent backwardation in LME spreads.Fastmarkets’ aluminium P1020A, in-whs dup Rotterdam, premium was US$80-90/t on Monday December 16, significantly lower than September when it was at a high of $105-115 per tonne. The first quarterly aluminium premium contract (Jan-March 2020) for Japan for the shipment of 1,000 tonne per month was settled at US$83/t, plus LME cash settlement average of the shipment month on December 4.

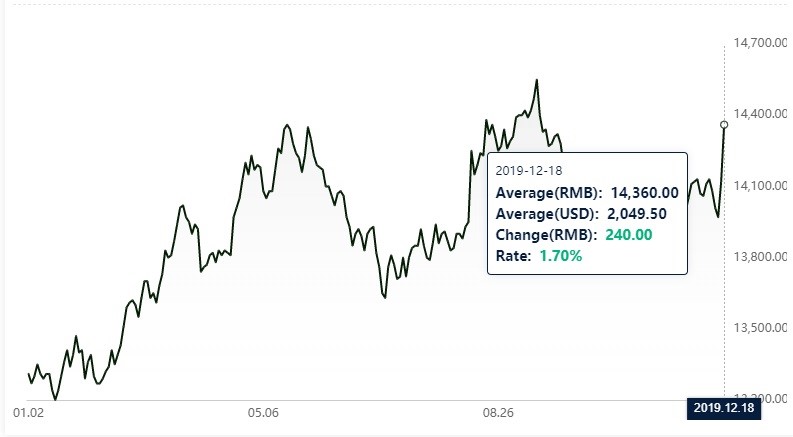

China Aluminium Spot Price

On the other hand China aluminium price has seen an upward growth in 2019. A tight aluminium market in China because of domestic supplies fall has boosted prices in Shanghai, which have been outperforming those on the London Metal Exchange where weaker demand in the rest of world is reflected. Spot aluminium prices on the Shanghai Futures Exchange (ShFE) rose more than 9% to RMB 14,550 ($2,053.75) per tonne from January to September and are currently around RMB 14,360 (US$2,049.5) per tonne.

Short Term Outlook

Aluminum is expected to again be in substantial surplus in 2020, with demand slowing down and new primary aluminium capacity coming up in China and Middle East. Bahrain-based Alba has inaugurated its Line 6 Expansion Project on 24 November 2019, which will increase Alba’s annual production by 540,000 tonnes bringing the total production capacity to 1.54 million tpy. The company aims to have a strong finish in 2019 as its production will top 1.35 million tonne.

Australia’s Department of Industry has cut 2020 consumption forecast by 8% to 63.53 million tonnes and 2021, by 13% to 62.42 million tonnes respectively.

SMM senior aluminium analyst Liang Xuan at 2019 China Nonferrous Metals Industry Annual Meeting said that output of primary aluminium in China is expected to increase 2.5 per cent to 36.44 million tonnes in 2020, after shrinking 1.51 per cent this year. He also told delegates that consumption is likely to grow, but a slower pace of 0.3 per cent to 36.19 million tonnes from a decline of 1.48 per cent in 2019. Aluminium production might grow much faster than consumption in 2020, said Liang Xuan. Xuan also pointed that this could put pressure on aluminium prices in turn in the coming year.

Concerns over global growth and a slowing demand condition is expected to keep aluminium prices subdued over 2019 and also in 2020. Price is expected to pick up only if US-China trade clash reaches a solution and global economic growth picks up.

As the alumina costs have fallen drastically and there have been no further capacity cuts, there is no indication for a supply side support. If there is no further supply cut in China or rest of the world, aluminium prices may drop to a level of US$1,657/t in the first quarter of 2020.

Responses