您想继续阅读英文文章还

是切换到中文?

是切换到中文?

THINK ALUMINIUM THINK AL CIRCLE

The social inventories of primary aluminium in China usher the year 2020 with a growth of 18,000 tonnes over the week, indicating a potential end to the continued inventory downtrend since March 2019.

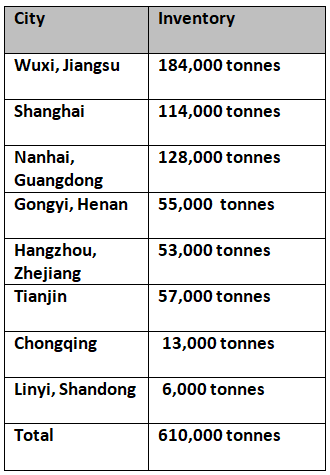

Thus, the stocks across eight major consumption areas, including SHFE warrants, as of today, January 2, have come in at 610,000 tonnes, in compare to 592,000 tonnes on last Thursday, December 26, after declining by 12,000 tonnes week-on-week.

{alcircleadd}

As can be seen in the above chart that except in the two major cities, the inventories have increased in the rest of the cities, such as Shanghai, Nanhai, Gongyi, Hangzhou, and Linyi, where the inventories have climbed up by 2,000 tonnes, 19,000 tonnes, and 1,000 tonnes, respectively, to stand at 114,000 tonnes, 128,000 tonnes, 55,000 tonnes, 53,000 tonnes, and 6,000 tonnes. In Wuxi and Chongqing, the inventories have dropped by 7,000 tonnes and 1,000 tonnes to 184,000 tonnes and 13,000 tonnes, respectively.

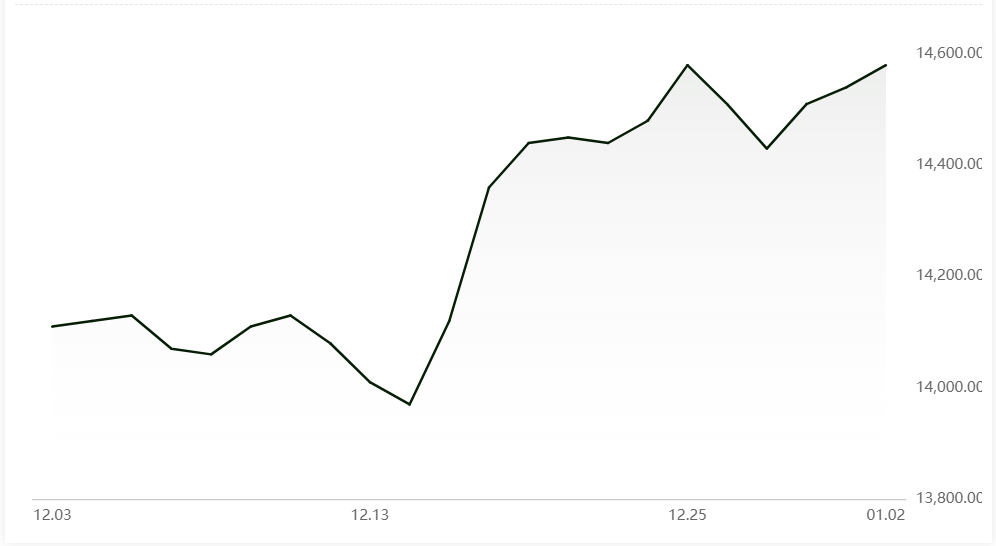

As of today, January 2, the price of A00 aluminium ingot has also increased, along with the growth in primary aluminium inventories. The ingot price, recording a rise of RMB 40 per tonne, has clocked at RMB 14,580 per tonne. The average prices are expected to range between RMB 14,560 per tonne and RMB 14,600 per tonne, with spot contract to be traded at a premium price of RMB 140-180 per tonne.

Except in Tianjin, Wuxi, Gongyi, and Shenyang, the ingot price in other major cities has increased by RMB 40 per tonne. In Tianjin and Wuxi, the price has inched up by 50 per tonne, while in Gongyi and Shenyang by RMB 45 per tonne and RMB 5 per tonne, respectively.

Responses